Wells Fargo 2008 Annual Report Download - page 49

Download and view the complete annual report

Please find page 49 of the 2008 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

|

|

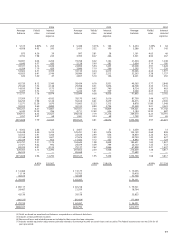

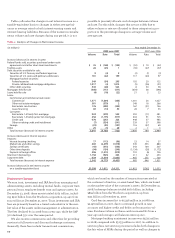

Earnings Performance

Net Interest Income

Net interest income is the interest earned on debt securities,

loans (including yield-related loan fees) and other interest-

earning assets minus the interest paid for deposits and long-

term and short-term debt. The net interest margin is the aver-

age yield on earning assets minus the average interest rate

paid for deposits and our other sources of funding. Net inter-

est income and the net interest margin are presented on a

taxable-equivalent basis to consistently reflect income from

taxable and tax-exempt loans and securities based on a 35%

federal statutory tax rate.

Net interest income on a taxable-equivalent basis was

$25.4 billion in 2008, up 20% from $21.1 billion in 2007. Our

net interest margin increased to 4.83% for 2008 from 4.74%

for 2007. Both the increase in net interest income and the

increase in the net interest margin were largely driven by

disciplined deposit pricing and lower market funding costs.

Average earning assets increased $77.6 billion to

$523.5 billion in 2008 from $445.9 billion in 2007. Average

loans increased to $398.5 billion in 2008 from $344.8 billion

in 2007. Average mortgages held for sale decreased to

$25.7 billion in 2008 from $33.1 billion in 2007. Average debt

securities available for sale increased to $86.3 billion in 2008

from $57.0 billion in 2007.

The purchase accounting adjustments that we recorded on

Wachovia's interest-earning assets and interest-bearing lia-

bilities to reflect market rates of interest for each instrument

or pool of instruments will affect net interest income begin-

ning in first quarter 2009. The more significant of these

adjustments include an $8.2 billion net increase to loans

where amortization will decrease net interest income, a $4.4

billion net increase to deposits, specifically certificates of

deposit, and a $190 million increase to long-term debt, where

amortization for both will increase net interest income.

Core deposits are an important contributor to growth in

net interest income and the net interest margin, and are a

low-cost source of funding. Core deposits are noninterest-

bearing deposits, interest-bearing checking, savings certifi-

cates, market rate and other savings, and certain foreign

deposits (Eurodollar sweep balances). We have one of the

largest bases of core deposits among large U.S. banks.

Average core deposits grew 7% to $325.2 billion in 2008 from

$303.1 billion in 2007 and funded 82% and 88% of average

total loans in 2008 and 2007, respectively. Total average

retail core deposits, which exclude Wholesale Banking core

deposits and retail mortgage escrow deposits, for 2008 grew

$13.1 billion (6%) from 2007. Average mortgage escrow

deposits decreased to $21.0 billion in 2008 from $21.5 billion

in 2007. Average savings certificates of deposit decreased to

$39.5 billion in 2008 from $40.5 billion in 2007 and average

noninterest-bearing checking accounts and other core

deposit categories (interest-bearing checking and market

rate and other savings) increased to $260.2 billion in 2008

from $241.9 billion in 2007. Total average interest-bearing

deposits increased to $266.1 billion in 2008 from $239.2 bil-

lion in 2007, predominantly due to growth in market rate and

other savings, along with growth in foreign deposits, offset by

a decline in other time deposits.

Table 3 presents the individual components of net interest

income and the net interest margin.

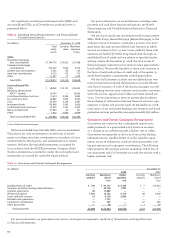

ment taxing authorities, both domestic and foreign. Our

interpretations may be subjected to review during examina-

tion by taxing authorities and disputes may arise over the

respective tax positions. We attempt to resolve these dis-

putes during the tax examination and audit process and ulti-

mately through the court systems when applicable.

We monitor relevant tax authorities and revise our esti-

mate of accrued income taxes due to changes in income tax

laws and their interpretation by the courts and regulatory

authorities on a quarterly basis. Revisions of our estimate of

accrued income taxes also may result from our own income

tax planning and from the resolution of income tax contro-

versies. Such revisions in our estimates may be material to

our operating results for any given quarter.

See Note 21 (Income Taxes) to Financial Statements for a

further description of our provision for income taxes and

related income tax assets and liabilities.