Wells Fargo 2008 Annual Report Download - page 76

Download and view the complete annual report

Please find page 76 of the 2008 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

|

|

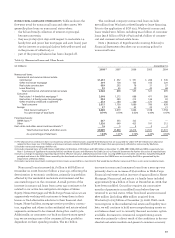

Comparison of 2007 with 2006

Our financial results included the following:

Net income in 2007 was $8.06 billion ($2.38 per share),

compared with $8.42 billion ($2.47 per share) in 2006. Results

for 2007 included the impact of a $1.4 billion (pre tax) credit

reserve build ($0.27 per share) and $203 million of Visa litiga-

tion expenses ($0.04 per share), and for 2006 included $95

million ($0.02 per share) of Visa litigation expenses. Despite

the challenging environment in 2007, we had a solid year and

achieved both double-digit top line revenue growth and posi-

tive operating leverage (revenue growth of 10.4% exceeding

expense growth of 9.5%).

The financial services industry faced unprecedented chal-

lenges in 2007. Home values declined abruptly and sharply,

adversely impacting the consumer lending business of many

financial service providers; credit spreads widened as the capital

markets repriced in many asset classes; price volatility increased

and market liquidity decreased in several sectors of the capital

markets; and, late in the year, economic growth declined sharply.

We were not immune to these unprecedented external

factors. Our provision for credit losses was $2.7 billion higher

in 2007 than in 2006, reflecting $1.3 billion in additional

provisions for actual charge-offs that occurred in 2007 and a

$1.4 billion provision to further build reserves for loan losses.

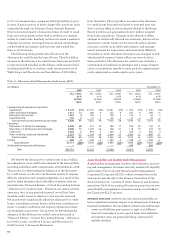

Historically, our policy has been to repurchase shares

under the “safe harbor” conditions of Rule 10b-18 of the

Securities Exchange Act of 1934 including a limitation on the

daily volume of repurchases. Rule 10b-18 imposes an addi-

tional daily volume limitation on share repurchases during a

pending merger or acquisition in which shares of our stock

will constitute some or all of the consideration. Our manage-

ment may determine that during a pending stock merger or

acquisition when the safe harbor would otherwise be avail-

able, it is in our best interest to repurchase shares in excess

of this additional daily volume limitation. In such cases, we

intend to repurchase shares in compliance with the other

conditions of the safe harbor, including the standing daily

volume limitation that applies whether or not there is a pend-

ing stock merger or acquisition.

Our potential sources of capital include retained earnings

and issuances of common and preferred stock. In 2008,

retained earnings decreased $2.4 billion, predominantly as a

result of net income of $2.7 billion less common and preferred

dividends and accretion of $4.6 billion. In 2008, we issued

468.5 million shares in a common stock offering to the public

valued at $12.3 billion. We also issued approximately 86 mil-

lion shares of common stock valued at $2.3 billion under vari-

ous employee benefit and director plans (including shares

issued for our ESOP plan) and under our dividend reinvest-

ment and direct stock purchase programs, and we issued

approximately 429 million shares of common stock valued

at $14.6 billion for acquisitions, including $14.4 billion (as of

the announcement date of the acquisition) for the Wachovia

acquisition. Wachovia shareholders received 0.1991 shares

of Wells Fargo common stock in exchange for each share

of Wachovia common stock they owned, for a total of

422.7 million shares of Wells Fargo common stock. Shares of

each outstanding series of Wachovia preferred stock were

converted into shares (or fractional shares) of a correspond-

ing series Wells Fargo preferred stock having substantially

the same rights and preferences.

On October 28, 2008, at the request of the United States

Department of the Treasury (Treasury Department) and pur-

suant to a Letter Agreement and related Securities Purchase

Agreement dated October 26, 2008 (the Securities Purchase

Agreements), we issued 25,000 shares of Wells Fargo’s Fixed

Rate Cumulative Perpetual Preferred Stock, Series D without

par value, having a liquidation amount per share equal to

$1,000,000, for a total price of $25 billion. We pay cumulative

dividends on the preferred securities at a rate of 5% per year

for the first five years and thereafter at a rate of 9% per year.

Unless permitted under the provisions of the American

Recovery and Reinvestment Act of 2009, we may not redeem

the preferred securities during the first three years except

with the proceeds from a “qualifying equity offering.” After

three years, we may, at our option, redeem the preferred secu-

rities at par value plus accrued and unpaid dividends. The

preferred securities are generally non-voting. Prior to

October 28, 2011, unless we have redeemed the preferred

securities or the Treasury Department has transferred the

preferred securities to a third party, the consent of the

Treasury Department will be required for us to increase our

common stock dividend or repurchase our common stock or

other equity or capital securities, other than in connection

with benefit plans consistent with past practice and certain

other circumstances specified in the Securities Purchase

Agreements. The terms of the Treasury Department’s pur-

chase of the preferred securities include certain restrictions

on certain forms of executive compensation and limits on the

tax deductibility of compensation we pay to executive man-

agement. As part of its purchase of the preferred securities,

the Treasury Department also received warrants to purchase

110,261,688 shares of our common stock at an initial per share

exercise price of $34.01, subject to customary anti-dilution

provisions. The warrants expire ten years from the issuance

date. Both the preferred securities and warrants will be

accounted for as components of Tier 1 capital.

The Company and each of our subsidiary banks are sub-

ject to various regulatory capital adequacy requirements

administered by the Federal Reserve Board and the OCC.

Risk-based capital guidelines establish a risk-adjusted ratio

relating capital to different categories of assets and off-bal-

ance sheet exposures. At December 31, 2008, the Company

and each of our subsidiary banks were “well capitalized”

under applicable regulatory capital adequacy guidelines. See

Note 26 (Regulatory and Agency Capital Requirements) to

Financial Statements for additional information.