Wells Fargo 2008 Annual Report Download - page 77

Download and view the complete annual report

Please find page 77 of the 2008 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

|

|

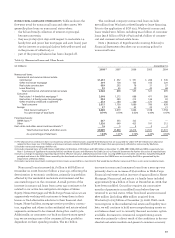

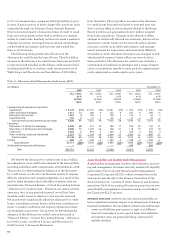

While the $2.7 billion in additional provisions reduced

consolidated net income after tax by 18%, consolidated full-

year earnings per share declined only 4% to $2.38 per share, a

strong overall result given the external environment and

higher credit costs.

Our results were as strong as they were because we largely

avoided or had negligible exposure to many of the problem

areas that resulted in significant costs and write-downs at

other large financial institutions and because we continued to

build our diversified franchise throughout 2007, once again

achieving growth rates, operating margins, and returns at or

near the top of the financial services industry, while at the same

time maintaining strong capital levels and strong liquidity.

We continued to make investments in 2007 by opening 87

regional banking stores and converting 42 stores acquired

from Placer Sierra Bancshares and National City Bank to our

network. We grew our sales and service force by adding 1,755

team members (full-time equivalents) in 2007, including 578

retail platform bankers. In fourth quarter 2007, we completed

the acquisition of Greater Bay Bancorp, with $7.4 billion in

assets, adding to our community banking, commercial insur-

ance brokerage, specialty finance and trust businesses.

Revenue, the sum of net interest income and noninterest

income, grew 10.4% to a record $39.4 billion in 2007 from

$35.7 billion in 2006. The breadth and depth of our business

model resulted in very strong and balanced growth in loans,

deposits and fee-based products. Many of our businesses con-

tinued to post double-digit, year-over-year revenue growth,

including business direct, wealth management, credit and

debit card, global remittance services, personal credit man-

agement, home mortgage, asset-based lending, asset manage-

ment, specialized financial services and international.

Among the many products and services that grew in 2007,

we achieved the following results:

• average loans grew 12%;

• average core deposits grew 13%;

• assets under management were up 14%;

• mortgage servicing fees were up 14%;

• insurance premiums were up 14%; and

• total noninterest income rose 17%, reflecting the breadth

of our cross-sell efforts.

ROA was 1.55% and ROE was 17.12% in 2007, compared

with 1.73% and 19.52%, respectively, in 2006. Both ROA and

ROE were, once again, at or near the top of our large bank

peers.

Net interest income on a taxable-equivalent basis was

$21.1 billion in 2007, up from $20.1 billion a year ago, reflect-

ing strong growth in earning assets. Average earning assets

grew 7% from 2006. Our net interest margin was 4.74% for

2007, compared with 4.83% in 2006, primarily due to earning

assets increasing at a slightly faster rate than core deposits.

Noninterest income increased 17% to $18.4 billion in 2007

from $15.7 billion in 2006. The increase was across our busi-

nesses, with double-digit increases in debit and credit card

fees (up 22%), deposit service charges (up 13%), trust and

investment fees (up 15%), and insurance revenue (up 14%).

Capital markets and equity investment results were also

strong. Mortgage banking noninterest income increased $822

million (36%) from 2006 because net servicing fee income

increased due to growth in loans serviced for others.

During 2007, noninterest income was affected by changes

in interest rates, widening credit spreads, and other credit

and housing market conditions, including:

• $(803) million – $479 million write-down of the mortgage

warehouse/pipeline, and $324 million write-down, primari-

ly due to mortgage loans repurchased, and an increase in

the repurchase reserve for projected early payment

defaults.

• $583 million – Increase in mortgage servicing income

reflecting a $571 million reduction in the value of MSRs

due to the decline in mortgage rates during the year, off-

set by a $1.15 billion gain on the financial instruments

hedging the MSRs. The ratio of MSRs to related loans ser-

viced for others at December 31, 2007, was 1.20%, the low-

est ratio in 10 quarters.

Noninterest expense was $22.8 billion in 2007, up 9.5%

from $20.8 billion in 2006, primarily due to continued invest-

ments in new stores and additional sales and service-related

team members. We grew our sales and service force by

adding 1,755 team members (full-time equivalents), including

578 retail platform bankers. The acquisition of Greater Bay

Bancorp added $87 million of expenses in 2007. Despite these

investments and the acquisition of Greater Bay Bancorp and

related integration expense, our efficiency ratio improved to

57.9% in 2007 from 58.4% in 2006. We obtained concurrence

from the staff of the SEC regarding our accounting for certain

transactions related to the restructuring of Visa, and record-

ed a litigation liability and corresponding expense, included

in operating losses, of $203 million for 2007 and $95 million

for 2006. In addition, expenses in 2007 included $433 million

in origination costs that, prior to the adoption of FAS 159,

would have been deferred and recognized as a reduction of

net gains on mortgage loan origination/sales activities at the

time of sale.

During 2007, net charge-offs were $3.54 billion (1.03% of

average total loans), up $1.3 billion from $2.25 billion (0.73%)

during 2006. Commercial and commercial real estate net

charge-offs increased $239 million in 2007 from 2006, of

which $162 million was from loans originated through our

Business Direct channel. Business Direct consists primarily

of unsecured lines of credit to small firms and sole propri-

etors that tend to perform in a manner similar to credit cards.

Total wholesale net charge-offs (excluding business direct)

were $103 million (0.08% of average loans). The remaining

balance of commercial and commercial real estate (other real

estate mortgage, real estate construction and lease financing)

continued to have low net charge-off rates in 2007.

National Home Equity Group portfolio net charge-offs

totaled $595 million (0.73% of average loans) in 2007, com-

pared with $110 million (0.14%) in 2006. Because the majority

of the Home Equity net charge-offs were concentrated in the

indirect or third party origination channels, which have a

higher percentage of 90% or greater combined loan-to-value

portfolios, we have discontinued third party activities not