Wells Fargo 2008 Annual Report Download - page 69

Download and view the complete annual report

Please find page 69 of the 2008 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

|

|

estimated loss emergence coverage periods to the most

conservative of each company within FFIEC guidelines as

described below. The reserve for unfunded credit commit-

ments was $698 million at December 31, 2008, and $211 million

at December 31, 2007.

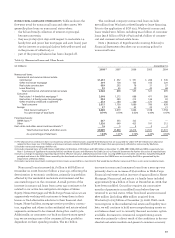

The ratio of the allowance for credit losses to total nonac-

crual loans was 319% and 206% at December 31, 2008 and

2007, respectively. The increase in this ratio reflects the addi-

tion of $9.3 billion (including $1.5 billion of conforming and

purchase accounting adjustments) of Wachovia allowance for

credit losses, but excludes $20.0 billion of SOP 03-3 loans that

were previously reflected as nonaccrual by Wachovia. This

ratio may fluctuate significantly from period to period due to

such factors as the mix of loan types in the portfolio, borrow-

er credit strength and the value and marketability of collater-

al. Over half of nonaccrual loans were home mortgages, auto

and other consumer loans at December 31, 2008. Nonaccrual

loans are generally written down to fair value less cost to sell

at the time they are placed on nonaccrual and accounted for

on a cost recovery basis.

The ratio of the allowance for loan losses to annual net

charge-offs was 268%, 150% and 175% at December 31, 2008,

2007 and 2006, respectively. The increase in this ratio pri-

marily relates to the addition of $8.7 billion (including $1.2

billion of conforming adjustments) from Wachovia while net

charge-offs do not include any amounts from Wachovia as

the acquisition closed at year end. This ratio may fluctuate

significantly from period to period due to many factors,

including general economic conditions, customer credit

strength and the marketability of collateral. While we consid-

er the ratio of the allowance for loan losses to annual net

charge-offs, such trends are not determinative in and of

themselves, as we use several analytical tools in determining

the adequacy of the allowance for loan losses. The allowance

for loan losses reflects management’s estimate of credit losses

inherent in the loan portfolio based on loss emergence peri-

ods of the respective loans, underlying economic and market

conditions, among other factors. See “Critical Accounting

Policies – Allowance for Credit Losses” for additional infor-

mation. The allowance for loan losses at December 31, 2008,

also includes the allowance acquired from the Wachovia

acquisition, while 2008 net charge-offs do not include activity

related to Wachovia.

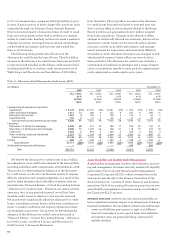

The provision for credit losses totaled $16.0 billion in 2008,

$4.9 billion in 2007 and $2.2 billion in 2006. In 2008, the pro-

vision included a credit reserve build of $8.1 billion in excess

of net charge-offs, which included $3.9 billion to conform loss

emergence coverage periods to the most conservative of each

company within FFIEC guidelines. Of the $3.9 billion, $2.7 bil-

lion related to Wells Fargo consumer loans to extend the loss

emergence period to 12 months of estimated incurred losses

for all consumer portfolios, a period which is FFIEC compliant

and which best fits the projected loss emergence period of the

combined company’s consumer loan portfolio, and is consis-

tent with Wells Fargo consumer loan portfolio loss emer-

gence trends reflecting our increased loss mitigation efforts.

The remaining $1.2 billion conforming adjustment was

related to an increase in the allowance for loan losses for

legacy Wachovia commercial and Pick-a-Pay portfolios to

align with the respective Wells Fargo methodology. The

remainder of the reserve build was attributable to higher pro-

jected loss rates across the majority of the consumer credit

businesses, and some credit deterioration and growth in the

wholesale portfolios. In 2007, the provision included $1.4 bil-

lion in excess of net charge-offs, which was our estimate of

the increase in incurred losses in our loan portfolio at year-

end 2007, primarily related to the Home Equity portfolio.

Net charge-offs in 2008 were 1.97% of average total loans,

compared with 1.03% in 2007 and 0.73% in 2006. Home Equity

net charge-offs totaled $2.2 billion (2.59% of average Home

Equity loans) in 2008, a $1.6 billion increase from $595 mil-

lion (0.73%) in 2007. The increase was primarily due to loans

in geographic markets that have experienced the most abrupt

and steepest declines in housing prices coupled with a deteri-

orating economic environment impacting our customers.

Since our loss experience through third party channels pro-

duced unexpectedly high results, we segregated these loans

into a liquidating portfolio. As previously disclosed, while the

$10.3 billion of loans in this liquidating portfolio represented

about 1% of total loans outstanding at December 31, 2008,

these loans represent some of the highest risk in our

$129.5 billion Home Equity portfolios. The loans in the liqui-

dating portfolio were primarily sourced through wholesale

(brokers) and correspondents. Our real estate 1-4 family first

mortgage portfolio began to experience credit deterioration

in 2008 given the continued decline in housing prices and the

economic environment, with net charge-offs of $503 million

(0.67% of average loans) for 2008, up from $87 million (0.14%)

for 2007.

Although credit quality in Wells Fargo Financial’s real

estate-secured lending business has deteriorated, we have not

experienced the level of credit degradation that many non-

prime lenders have because of our disciplined underwriting

practices. Wells Fargo Financial has continued its long-stand-

ing practice not to use brokers or correspondents in its U.S.

debt consolidation business.

Auto portfolio net charge-offs for 2008 were $1.23 billion

(4.50% of average auto loans), compared with $1.02 billion

(3.45%) in 2007. While we have continued to reduce the size

of this portfolio and limited additional growth, the economic

environment has adversely affected portfolio results. We

have remained focused on our loss mitigation strategies,

however, credit performance has deteriorated as a result of

increased unemployment and depressed used car values,

resulting in higher than expected losses for the year.

Consumer credit card net charge-offs for 2008 were

$1.42 billion (7.22% of average credit card loans), compared

with $712 million (4.49%) in 2007. The increase in credit card

net charge-offs was due to an overall weakening in the economy

and its impact to our customers.

Credit performance in the commercial and commercial real

estate portfolio showed signs of deterioration given the current

economic environment, with net charge-offs of $1.79 billion