Wells Fargo 2008 Annual Report Download - page 164

Download and view the complete annual report

Please find page 164 of the 2008 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172

|

|

Condensed Consolidating Statement of Cash Flows

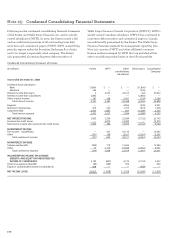

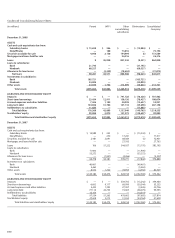

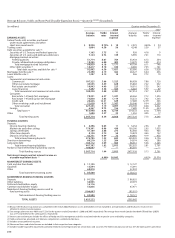

(in millions) Parent WFFI Other Consolidated

consolidating Company

subsidiaries/

eliminations

Year ended December 31, 2006

Cash flows from operating activities:

Net cash provided by operating activities $ 3,536 $ 1,179 $ 23,261 $ 27,976

Cash flows from investing activities:

Securities available for sale:

Sales proceeds 353 822 52,129 53,304

Prepayments and maturities 14 259 7,048 7,321

Purchases (378) (1,032) (61,052) (62,462)

Loans:

Increase in banking subsidiaries’ loan

originations, net of collections — (2,003) (35,727) (37,730)

Proceeds from sales (including participations) of loans

originated for investment by banking subsidiaries — 50 38,293 38,343

Purchases (including participations) of loans by

banking subsidiaries — (202) (5,136) (5,338)

Principal collected on nonbank entities’ loans — 19,998 3,923 23,921

Loans originated by nonbank entities — (22,382) (4,592) (26,974)

Net repayments from (advances to) subsidiaries (500) — 500 —

Capital notes and term loans made to subsidiaries (7,805) — 7,805 —

Principal collected on notes/loans made to subsidiaries 4,926 — (4,926) —

Net decrease (increase) in investment in subsidiaries (145) — 145 —

Net cash paid for acquisitions — — (626) (626)

Other, net — 1,081 (7,422) (6,341)

Net cash used by investing activities (3,535) (3,409) (9,638) (16,582)

Cash flows from financing activities:

Net change in:

Deposits — — (4,452) (4,452)

Short-term borrowings 931 (1,297) (10,790) (11,156)

Long-term debt:

Proceeds from issuance 13,448 8,670 (1,863) 20,255

Repayment (7,362) (5,217) (30) (12,609)

Common stock:

Proceeds from issuance 1,764 — — 1,764

Repurchased (1,965) — — (1,965)

Cash dividends paid (3,641) — — (3,641)

Excess tax benefits related to stock option payments 227 — — 227

Other, net 12 70 (268) (186)

Net cash provided (used) by financing activities 3,414 2,226 (17,403) (11,763)

Net change in cash and due from banks 3,415 (4) (3,780) (369)

Cash and due from banks at beginning of year 10,794 474 4,129 15,397

Cash and due from banks at end of year $14,209 $ 470 $ 349 $ 15,028

Note 26: Regulatory and Agency Capital Requirements

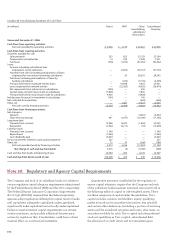

The Company and each of its subsidiary banks are subject to

various regulatory capital adequacy requirements administered

by the Federal Reserve Board (FRB) and the OCC, respectively.

The Federal Deposit Insurance Corporation Improvement

Act of 1991 (FDICIA) required that the federal regulatory

agencies adopt regulations defining five capital tiers for banks:

well capitalized, adequately capitalized, undercapitalized,

significantly undercapitalized and critically undercapitalized.

Failure to meet minimum capital requirements can initiate

certain mandatory, and possibly additional discretionary,

actions by regulators that, if undertaken, could have a direct

material effect on our financial statements.

Quantitative measures, established by the regulators to

ensure capital adequacy, require that the Company and each

of the subsidiary banks maintain minimum ratios (set forth in

the following table) of capital to risk-weighted assets. There

are three categories of capital under the guidelines. Tier 1

capital includes common stockholders’ equity, qualifying

preferred stock and trust preferred securities, less goodwill

and certain other deductions (including a portion of servicing

assets and the unrealized net gains and losses, after taxes, on

securities available for sale). Tier 2 capital includes preferred

stock not qualifying as Tier 1 capital, subordinated debt,

the allowance for credit losses and net unrealized gains