Wells Fargo 2008 Annual Report Download - page 57

Download and view the complete annual report

Please find page 57 of the 2008 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

|

|

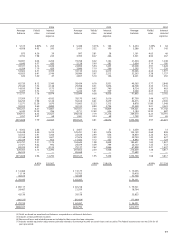

Table 10: Deposits

(in millions) December 31,%

2008 2007 Change

Noninterest-bearing $150,837 $ 84,348 79%

Interest-bearing checking 72,828 5,277 NM

Market rate and

other savings 306,255 153,924 99

Savings certificates 182,043 42,708 326

Foreign deposits (1) 33,469 25,474 31

Core deposits 745,432 311,731 139

Other time deposits 28,498 3,654 680

Other foreign deposits 7,472 29,075 (74)

Total deposits $781,402 $344,460 127

NM – Not meaningful

(1) Reflects Eurodollar sweep balances included in core deposits.

Off-Balance Sheet Arrangements

In the ordinary course of business, we engage in financial

transactions that are not recorded in the balance sheet, or may

be recorded in the balance sheet in amounts that are different

from the full contract or notional amount of the transaction.

These transactions are designed to (1) meet the financial needs

of customers, (2) manage our credit, market or liquidity risks,

(3) diversify our funding sources, and/or (4) optimize capital.

These are described below as off-balance sheet transactions

with unconsolidated entities, and guarantees and certain

contingent arrangements.

Off-Balance Sheet Transactions with Unconsolidated Entities

In the normal course of business, we enter into various types

of on- and off-balance sheet transactions with special purpose

entities (SPEs). SPEs are corporations, trusts or partnerships

that are established for a limited purpose. The majority of SPEs

are formed in connection with securitization transactions. In a

securitization transaction, assets from our balance sheet are

transferred to an SPE, which then issues to investors various

forms of interests in those assets and may also enter into

derivative transactions. In a securitization transaction, we

typically receive cash and/or other interests in an SPE as pro-

ceeds for the assets we transfer. Also, in certain transactions,

we may retain the right to service the transferred receivables

and to repurchase those receivables from the SPE if the out-

standing balance of the receivables fall to a level where the

cost exceeds the benefits of servicing such receivables.

In connection with our securitization activities, we have

various forms of ongoing involvement with SPEs, which may

include:

• underwriting securities issued by SPEs and subsequently

making markets in those securities;

• providing liquidity facilities to support short-term

obligations of SPEs issued to third party investors;

• providing credit enhancement to securities issued by SPEs

or market value guarantees of assets held by SPEs through

the use of letters of credit, financial guarantees, credit

default swaps and total return swaps;

• entering into other derivative contracts with SPEs;

• holding senior or subordinated interests in SPEs;

• acting as servicer or investment manager for SPEs; and

• providing administrative or trustee services to SPEs.

The SPEs we use are primarily either qualifying SPEs

(QSPEs) or variable interest entities (VIEs). A QSPE repre-

sents a specific type of SPE. A QSPE is a passive entity that

has significant limitations on the types of assets and deriva-

tive instruments it may own and the extent of activities and

decision making in which it may engage. For example, a

QSPE’s activities are generally limited to purchasing assets,

passing along the cash flows of those assets to its investors,

servicing its assets and, in certain transactions, issuing liabil-

ities. Among other restrictions on a QSPE’s activities, a QSPE

may not actively manage its assets through discretionary

sales or modifications. A QSPE is exempt from consolidation.

A VIE is an entity that has either a total equity investment

that is insufficient to permit the entity to finance its activities

without additional subordinated financial support or whose

equity investors lack the characteristics of a controlling

financial interest. A VIE is consolidated by its primary benefi-

ciary, which is the entity that, through its variable interests,

absorbs the majority of a VIE’s variability. A variable interest

is a contractual, ownership or other interest that changes

with changes in the fair value of the VIE’s net assets.

Deposits

Year-end deposit balances totaling $781.4 billion, which

included $426.2 billion from Wachovia (reflecting an increase

of $4.4 billion of interest rate related purchase accounting

adjustments), are shown in Table 10. A comparative detail of

average deposit balances is included in Table 3. Average core

deposits, which did not include Wachovia deposits, increased

$22.1 billion to $325.2 billion in 2008 from $303.1 billion in

2007. Average core deposits funded 53.8% and 58.2% of aver-

age total assets in 2008 and 2007, respectively. Total average

interest-bearing deposits increased to $266.1 billion in 2008 from

$239.2 billion in 2007, predominantly due to growth in market

rate and other savings, along with growth in foreign deposits,

offset by a decline in other time deposits. Total average non-

interest-bearing deposits declined to $87.8 billion in 2008

from $88.9 billion in 2007. Savings certificates decreased on

average to $39.5 billion in 2008 from $40.5 billion in 2007.