Wells Fargo 2008 Annual Report Download - page 60

Download and view the complete annual report

Please find page 60 of the 2008 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

|

|

Credit Risk Management Process

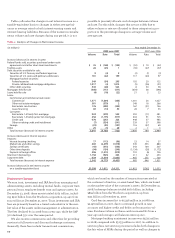

Our credit risk management process provides for decentral-

ized management and accountability by our lines of business.

Our overall credit process includes comprehensive credit

policies, judgmental or statistical credit underwriting, fre-

quent and detailed risk measurement and modeling, exten-

sive credit training programs and a continual loan review and

audit process. In addition, regulatory examiners review and

perform detailed tests of our credit underwriting, loan admin-

istration and allowance processes. We continually evaluate

and modify our credit policies to address unacceptable levels

of risk as they are identified.

Managing credit risk is a company-wide process. We have

credit policies for all banking and nonbanking operations

incurring credit risk with customers or counterparties that

provide a prudent approach to credit risk management. We

use detailed tracking and analysis to measure credit perfor-

mance and exception rates, and we routinely review and mod-

ify credit policies as appropriate. We have corporate data

integrity standards to ensure accurate and complete credit

performance reporting for the consolidated company. We

strive to identify problem loans early and have dedicated,

specialized collection and work-out units.

The Chief Credit and Risk Officer provides company-wide

credit oversight. Each business unit with direct credit risks

has a senior credit officer who has the primary responsibility

for managing its own credit risk. The Chief Credit and Risk

Officer delegates authority, limits and other requirements to

the business units. These delegations are routinely reviewed

and amended if there are significant changes in personnel,

credit performance or business requirements. The Chief

Credit and Risk Officer is a member of the Company’s

Management Committee and reports to the Chief Executive

Officer. The Chief Credit and Risk Officer provides a quarterly

credit review to the Credit Committee of the Board of

Directors and meets with them periodically.

Our business units and the office of the Chief Credit and

Risk Officer periodically review all credit risk portfolios to

ensure that the risk identification processes are functioning

properly and that credit standards are followed. Business

units conduct quality assurance reviews to ensure that loans

meet portfolio or investor credit standards. Our loan examin-

ers in risk asset review and internal audit independently

review portfolios with credit risk, monitor performance, sam-

ple credits, review and test adherence to credit policy and

recommend/require corrective actions as necessary.

Transactions with Related Parties

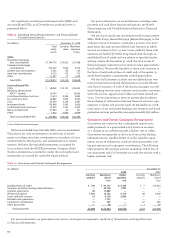

FAS 57, Related Party Disclosures, requires disclosure of mate-

rial related party transactions, other than compensation

arrangements, expense allowances and other similar items in

Our primary business focus on middle-market commer-

cial, commercial real estate, residential real estate, auto, cred-

it card and small consumer lending results in portfolio diver-

sification. We assess loan portfolios for geographic, industry

or other concentrations and use mitigation strategies, which

may include loan sales, syndications or third party insurance,

to minimize these concentrations, as we deem appropriate.

In our commercial loan, commercial real estate loan and

lease financing portfolios, larger or more complex loans are

individually underwritten and judgmentally risk rated. They

are periodically monitored and prompt corrective actions are

taken on deteriorating loans. Smaller, more homogeneous

commercial small business loans are approved and moni-

tored using statistical techniques.

Retail loans are typically underwritten with statistical

decision-making tools and are managed throughout their life

cycle on a portfolio basis. The Chief Credit and Risk Officer

establishes corporate standards for model development and

validation to ensure sound credit decisions and regulatory

compliance, and approves new model implementation and

periodic validation.

Residential real estate mortgages are one of our core prod-

ucts. We offer a broad spectrum of first mortgage and junior

lien loans that we consider mostly prime or near prime. These

loans are almost entirely secured by a primary residence for

the purpose of purchase money, refinance, debt consolidation

or home improvements. We now hold option adjustable rate

mortgages (option ARMs) in the Pick-a-Pay portfolio

acquired from Wachovia. This portfolio will be managed as a

liquidating portfolio. See page 61 of this Report for additional

information on the Pick-a-Pay portfolio. It has not been our

practice, nor do we intend to originate negative amortizing

option ARMs or variable-rate mortgage products with fixed

payment amounts. We have manageable ARM reset risk

across our Wells Fargo originated and owned mortgage loan

portfolios.

We originate mortgage loans through a variety of sources,

including our retail sales force and licensed real estate bro-

kers. We apply consistent credit policies, borrower documen-

tation standards, Federal Deposit Insurance Corporation

Improvement Act of 1991 (FDICIA) compliant appraisal

requirements, and sound underwriting, regardless of applica-

tion source. We perform quality control reviews for third

party originated loans and actively manage or terminate

sources that do not meet our credit standards. For example,

during 2007 we stopped originating first and junior lien resi-

the ordinary course of business. We had no related party

transactions required to be reported under FAS 57 for the

years ended December 31, 2008, 2007 and 2006.

Risk Management