Wells Fargo 2008 Annual Report Download - page 72

Download and view the complete annual report

Please find page 72 of the 2008 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

|

|

application, providing the commitment, and securitizing and

selling the loan, interest rate changes will impact origination

and servicing fees with a lag. The amount and timing of the

impact on origination and servicing fees will depend on the

magnitude, speed and duration of the change in interest rates.

Under FAS 159, The Fair Value Option for Financial Assets

and Financial Liabilities, including an amendment of FASB

Statement No. 115, which we adopted January 1, 2007, we

elected to measure MHFS at fair value prospectively for new

prime MHFS originations for which an active secondary mar-

ket and readily available market prices existed to reliably

support fair value pricing models used for these loans. At

December 31, 2008, we elected to measure at fair value simi-

lar MHFS acquired from Wachovia. Loan origination fees on

these loans are recorded when earned, and related direct loan

origination costs and fees are recognized when incurred. We

also elected to measure at fair value certain of our other

interests held related to residential loan sales and securitiza-

tions. We believe that the election for new prime MHFS and

other interests held (which are now hedged with free-stand-

ing derivatives (economic hedges) along with our MSRs)

reduces certain timing differences and better matches

changes in the value of these assets with changes in the value

of derivatives used as economic hedges for these assets.

During 2008, in response to continued secondary market

illiquidity, we continued to originate certain prime non-

agency loans to be held for investment for the foreseeable

future rather than to be held for sale.

Under FAS 156, Accounting for Servicing of Financial

Assets – an amendment of FASB Statement No. 140, we elected

to use the fair value measurement method to initially mea-

sure and carry our residential MSRs, which represent sub-

stantially all of our MSRs. Under this method, the MSRs are

recorded at fair value at the time we sell or securitize the

related mortgage loans. The carrying value of MSRs reflects

changes in fair value at the end of each quarter and changes

are included in net servicing income, a component of mort-

gage banking noninterest income. If the fair value of the

MSRs increases, income is recognized; if the fair value of the

MSRs decreases, a loss is recognized. We use a dynamic and

sophisticated model to estimate the fair value of our MSRs

and periodically benchmark our estimates to independent

appraisals. While the valuation of MSRs can be highly subjec-

tive and involve complex judgments by management about

matters that are inherently unpredictable, changes in interest

rates influence a variety of significant assumptions included

in the periodic valuation of MSRs. Assumptions affected

include prepayment speed, expected returns and potential

risks on the servicing asset portfolio, the value of escrow bal-

ances and other servicing valuation elements impacted by

interest rates.

A decline in interest rates generally increases the propen-

sity for refinancing, reduces the expected duration of the ser-

vicing portfolio and therefore reduces the estimated fair

value of MSRs. This reduction in fair value causes a charge to

income (net of any gains on free-standing derivatives (eco-

nomic hedges) used to hedge MSRs). We may choose not to

fully hedge all of the potential decline in the value of our

MSRs resulting from a decline in interest rates because the

potential increase in origination/servicing fees in that sce-

nario provides a partial “natural business hedge.” An increase

in interest rates generally reduces the propensity for refi-

nancing, increases the expected duration of the servicing

portfolio and therefore increases the estimated fair value of

the MSRs. However, an increase in interest rates can also

reduce mortgage loan demand and therefore reduce origina-

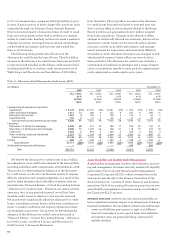

tion income. In 2008, a $3,341 million decrease in the fair

value of our MSRs and $3,099 million of gains on free-stand-

ing derivatives used to hedge the MSRs resulted in a net loss

of $242 million.

Hedging the various sources of interest rate risk in mort-

gage banking is a complex process that requires sophisticated

modeling and constant monitoring. While we attempt to bal-

ance these various aspects of the mortgage business, there

are several potential risks to earnings:

• MSRs valuation changes associated with interest rate

changes are recorded in earnings immediately within the

accounting period in which those interest rate changes

occur, whereas the impact of those same changes in inter-

est rates on origination and servicing fees occur with a lag

and over time. Thus, the mortgage business could be pro-

tected from adverse changes in interest rates over a period

of time on a cumulative basis but still display large varia-

tions in income from one accounting period to the next.

• The degree to which the “natural business hedge” offsets

changes in MSRs valuations is imperfect, varies at differ-

ent points in the interest rate cycle, and depends not just

on the direction of interest rates but on the pattern of

quarterly interest rate changes.

• Origination volumes, the valuation of MSRs and hedging

results and associated costs are also impacted by many

factors. Such factors include the mix of new business

between ARMs and fixed-rated mortgages, the relation-

ship between short-term and long-term interest rates, the

degree of volatility in interest rates, the relationship

between mortgage interest rates and other interest rate

markets, and other interest rate factors. Many of these fac-

tors are hard to predict and we may not be able to directly

or perfectly hedge their effect.

• While our hedging activities are designed to balance our

mortgage banking interest rate risks, the financial instru-

ments we use may not perfectly correlate with the values

and income being hedged. For example, the change in the

value of ARMs production held for sale from changes in

mortgage interest rates may or may not be fully offset by

Treasury and LIBOR index-based financial instruments

used as economic hedges for such ARMs.

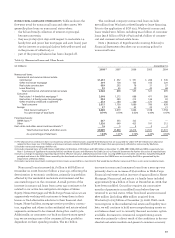

The total carrying value of our residential and commercial

MSRs was $16.2 billion at December 31, 2008, and $17.2 billion

at December 31, 2007. The weighted-average note rate on the

owned servicing portfolio was 5.92% at December 31, 2008,

and 6.01% at December 31, 2007. Our total MSRs were 0.87%

of mortgage loans serviced for others at December 31, 2008,

compared with 1.20% at December 31, 2007.