Sallie Mae 2007 Annual Report Download - page 99

Download and view the complete annual report

Please find page 99 of the 2007 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

|

|

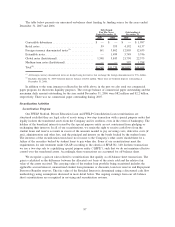

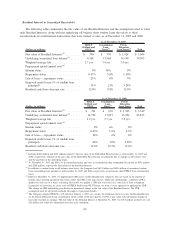

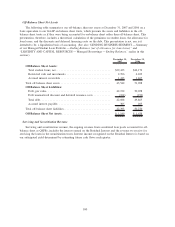

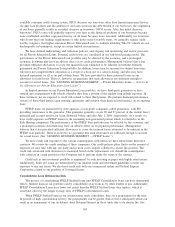

The following table summarizes our securitization activity for the years ended December 31, 2007, 2006

and 2005. Those securitizations listed as sales are off-balance sheet transactions and those listed as financings

remain on-balance sheet.

No. of

Transactions

Loan

Amount

Securitized

Pre-Tax

Gain

Gain

%

No. of

Transactions

Loan

Amount

Securitized

Pre-Tax

Gain

Gain

%

No. of

Transactions

Loan

Amount

Securitized

Pre-Tax

Gain

Gain

%

2007 2006 2005

Years Ended December 31,

(Dollars in millions)

Securitizations — sales:

FFELP Stafford/PLUS loans . . . — $ — $ — —% 2 $ 5,004 $ 17 .3% 3 $ 6,533 $ 68 1.1%

FFELP Consolidation Loans . . . — — — — 4 9,503 55 .6 2 4,011 31 .8

Private Education Loans ...... 1 2,001 367 18.4 3 5,088 830 16.3 2 3,005 453 15.1

Total securitizations — sales . . . 1 2,001 $367 18.4% 9 19,595 $902 4.6% 7 13,549 $552 4.1%

Securitizations — financings:

FFELP Stafford/PLUS loans

(1)

. . 3 8,955 — — — —

FFELP Consolidation Loans

(1)

. . 5 14,476 4 12,506 5 12,503

Total securitizations —

financings ............. 8 23,431 4 12,506 5 12,503

Total securitizations ......... 9 $25,432 13 $32,101 12 $26,052

(1)

In certain securitizations there are terms within the deal structure that result in such securitizations not qualifying for sale treatment

and accordingly, they are accounted for on-balance sheet as variable interest entities (“VIEs”). Terms that prevent sale treatment

include: (1) allowing the Company to hold certain rights that can affect the remarketing of certain bonds, (2) allowing the trust to enter

into interest rate cap agreements after initial settlement of the securitization, which do not relate to the reissuance of third party

beneficial interests or (3) allowing the Company to hold an unconditional call option related to a certain percentage of the securitized

assets.

The increase in the Private Education Loans gain as a percentage of loans securitized from 16.3 percent

for the year ended December 31, 2006 to 18.4 percent for the year ended December 31, 2007 is primarily due

to a higher spread earned on the assets securitized.

The decrease in the FFELP Stafford/PLUS loans gain as a percentage of loans securitized from 1.1 percent

for the year ended December 31, 2005 to .3 percent for the year ended December 31, 2006 is primarily due to:

1) an increase in the CPR assumption to account for continued high levels of FFELP Consolidation Loan

activity; 2) an increase in the discount rate to reflect higher long-term interest rates; 3) the re-introduction of

Risk Sharing with the Reconciliation Legislation during 2005 reauthorizing the student loan programs of the

Higher Education Act; and 4) an increase in the amount of student loan premiums included in the carrying

value of the loans sold. The higher premiums also affected FFELP Consolidation Loan securitizations and

were primarily due to the securitization of loans previously acquired through business combinations. These

loans carried higher premiums based on the allocation of the purchase price through purchase accounting.

Higher premiums were also due to loans acquired through zero-fee lending and the school-as-lender channels.

98