Sallie Mae 2007 Annual Report Download - page 108

Download and view the complete annual report

Please find page 108 of the 2007 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

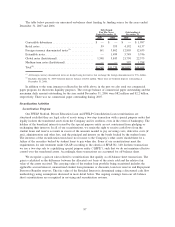

|

|

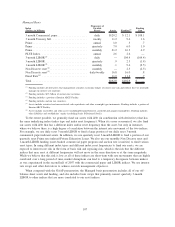

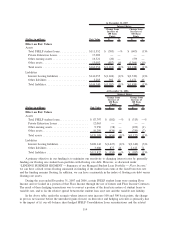

Managed Basis

Index

(Dollars in billions)

Frequency of

Variable

Resets Assets Funding

(1)

Funding

Gap

3 month Commercial paper ................... daily $120.2 $ 12.1 $ 108.1

3 month Treasury bill ....................... weekly 11.2 9.6 1.6

Prime ................................... annual 1.0 .3 .7

Prime ................................... quarterly 7.0 6.0 1.0

Prime ................................... monthly 21.2 16.3 4.9

PLUS Index .............................. annual 2.6 2.6 —

3-month LIBOR

(2)

......................... daily — 104.4 (104.4)

3-month LIBOR ........................... quarterly .9 2.3 (1.4)

1-month LIBOR

(3)

......................... monthly .1 9.6 (9.5)

Non Discrete reset

(4)

........................ monthly — 2.5 (2.5)

Non Discrete reset

(5)

........................ daily/weekly 16.8 16.0 .8

Fixed Rate

(6)

............................. 11.9 11.2 .7

Total ................................... $192.9 $192.9 $ —

(1)

Funding includes all derivatives that management considers economic hedges of interest rate risk and reflects how we internally

manage our interest rate exposure.

(2)

Funding includes $2.5 billion of auction rate securities.

(3)

Funding includes a portion of Interim ABCP Facility.

(4)

Funding includes auction rate securities.

(5)

Assets include restricted and non-restricted cash equivalents and other overnight type instruments. Funding includes a portion of

Interim ABCP Facility.

(6)

Assets include receivables and other assets (including Retained Interests, goodwill and acquired intangibles). Funding includes

other liabilities and stockholders’ equity (excluding Series B Preferred Stock).

To the extent possible, we generally fund our assets with debt (in combination with derivatives) that has

the same underlying index (index type and index reset frequency). When it is more economical, we also fund

our assets with debt that has a different index and/or reset frequency than the asset, but only in instances

where we believe there is a high degree of correlation between the interest rate movement of the two indices.

For example, we use daily reset 3-month LIBOR to fund a large portion of our daily reset 3-month

commercial paper indexed assets. In addition, we use quarterly reset 3-month LIBOR to fund a portion of our

quarterly reset Prime rate indexed Private Education Loans. We also use our monthly Non Discrete reset and

1-month LIBOR funding (asset-backed commercial paper program and auction rate securities) to fund various

asset types. In using different index types and different index reset frequencies to fund our assets, we are

exposed to interest rate risk in the form of basis risk and repricing risk, which is the risk that the different

indices that may reset at different frequencies will not move in the same direction or at the same magnitude.

While we believe that this risk is low as all of these indices are short-term with rate movements that are highly

correlated over a long period of time, market disruptions can lead to a temporary divergence between indices

as was experienced in the second half of 2007 with the commercial paper and LIBOR indices. We use interest

rate swaps and other derivatives to achieve our risk management objectives.

When compared with the GAAP presentation, the Managed basis presentation includes all of our off-

balance sheet assets and funding, and also includes basis swaps that primarily convert quarterly 3-month

LIBOR to other indices that are more correlated to our asset indices.

107