Sallie Mae 2007 Annual Report Download - page 94

Download and view the complete annual report

Please find page 94 of the 2007 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

|

|

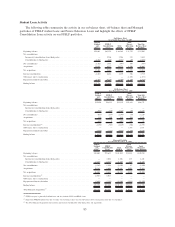

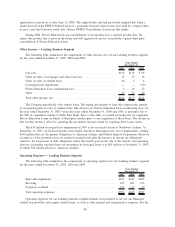

More recently, adverse conditions in the securitization markets increased the cost of borrowing in the

market for student loan asset-backed securities (“ABS”). In the third quarter of 2007, we completed one

$2.5 billion securitization transaction, compared to four securitization transactions totaling $13.0 billion in the

first quarter of 2007, the last full quarter before we entered into the Merger Agreement. In the fourth quarter

of 2007, we completed three securitization transactions totaling $4.9 billion. Although we expect ABS

financing to remain our primary source of funding, we expect our transaction volumes to be more limited and

pricing less favorable than in the past, with significantly reduced opportunities to issue subordinated tranches

of ABS.

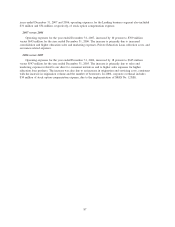

The Company has not recently and does not intend to rely on the auction rate securities market as a

source of funding. At December 31, 2007, we had $3.3 billion of taxable and $1.7 billion of tax-exempt

auction rate securities outstanding on a Managed Basis. In February 2008, an imbalance of supply and demand

in the auction rate securities market as a whole led to failures of the auctions pursuant to which certain of our

auction rate securities’ interest rates are set. As a result, certain of our auction rate securities bear interest at

the maximum rate allowable under their terms. The maximum allowable interest rate on our $3.3 billion of

taxable auction rate securities is generally LIBOR plus 1.50 percent. The maximum allowable interest rate on

many of our $1.7 billion of tax-exempt auction rate securities was recently amended to LIBOR plus 2.00

percent through May 31, 2008. After May 31, 2008, the maximum allowable rate on these securities will

revert to a formula driven rate, which, if in effect as of February 28, 2008, would have produced various

maximum rates ranging from up to 5.26 percent. The Company is currently exploring various options to

refinance its auction rate securities, if necessary.

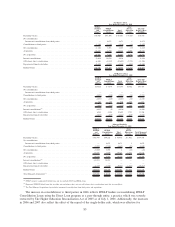

In the past, we employed reset rate note structures in conjunction with the issuance of certain tranches of

our term asset-backed securities. Reset rate notes are subject to periodic remarketing, at which time the

interest rates on the reset rate notes are reset. In the event a reset rate note cannot be remarketed on its

remarketing date, the interest rate generally steps up to and remains LIBOR plus 0.75 percent, until such time

as the bonds are successfully remarketed. The Company also has the option to repurchase the reset rate note

upon a failed remarketing and hold it as an investment until such time it can be remarketed. The Company’s

repurchase of a reset rate note requires additional funding, the availability and pricing of which may be less

favorable to the Company than it was at the time the reset rate note was originally issued. As of December 31,

2007, on a Managed Basis, the Company had $2.6 billion, $2.1 billion and $2.5 billion of reset rate notes due

to be remarketed in 2008, 2009 and 2010, and an additional $8.5 billion to be remarketed thereafter.

In order to meet our financing needs, we are exploring other sources of funding, including unsecured

debt, a financing source we have not used to fund our core businesses since the announcement of the Merger.

We expect the terms and conditions of new unsecured debt issues, including pricing and covenant require-

ments, will be less favorable to us than our recent ABS financings and unsecured debt we incurred in the past.

Our ability to access the unsecured debt market on attractive terms, or at all, will depend on our credit rating

and prevailing market conditions.

On April 30, 2007, in connection with the Merger Agreement, we entered into an aggregate interim

$30.0 billion asset-backed commercial paper conduit facilities (collectively, the “Interim ABCP Facility”) with

Bank of America, N.A., and JPMorgan Chase, N.A., which provided us with significant additional liquidity.

The Merger agreement contemplated a significant amount of whole loan sales as a main source of repayment

for this Interim ABCP Facility.

The Company has engaged J.P. Morgan Securities, Inc. (“JPMorgan”) and Banc of America Securities,

LLC (“BAS”) as Lead Arrangers and Joint Bookrunners along with Barclays Capital, The Royal Bank of

Scotland, plc and Deutsche Bank Securities, Inc. as Co-Lead Arrangers and Credit Suisse, New York Branch,

as Arranger to underwrite and arrange up to $28.0 billion of secured FFELP loan facilities and a $7.0 billion

secured private credit student loans facility (together, the “Facilities”). On January 28, 2008, we announced

that we had received commitments for $31.3 billion of 364-day financing from a consortium of banks led by

Bank of America, N.A., JPMorgan Chase, N.A., Barclays Capital, Deutsche Bank, Credit Suisse, and The

Royal Bank of Scotland, and from UBS. Funding under the commitments is subject to various conditions. As

of February 28, 2008, we anticipate closing on $23.4 billion of FFELP student loan ABCP conduit facilities

93