Sallie Mae 2007 Annual Report Download - page 105

Download and view the complete annual report

Please find page 105 of the 2007 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

|

|

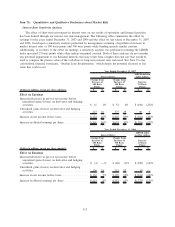

impact that changes in interest rates may have on net interest income, the more significant of which are related

to student loan volumes and pricing, the timing of cash flows from our student loan portfolio, particularly the

impact of Floor Income and the rate of student loan consolidations, basis risk, credit spreads and the maturity

of our debt and derivatives. (See also “Interest Rate Risk Management.”)

As discussed in more detail under “BUSINESS SEGMENTS — Limitations of ‘Core Earnings,’” even

though we believe our derivatives are economic hedges, some of them do not qualify for hedge accounting

treatment under SFAS No. 133. Therefore, changes in interest rates can cause volatility in those earnings for

the market value of our derivatives. Under SFAS No. 133, these changes in derivative market values are

recorded through earnings with no consideration for the corresponding change in the fair value of the hedged

item. Changes in interest rates can also have a material effect on the amount of Floor Income earned in our

student loan portfolio and the valuation of our Retained Interest asset. Our earnings can also be materially

affected by changes in our estimate of the rate at which loans may prepay in our portfolios as measured by the

CPR. The value of the Retained Interests on FFELP Stafford securitizations is particularly affected by the level

of Consolidation Loan activity. We face a number of other challenges and risks that can materially affect our

future results such as changes in:

• applicable laws and regulations, which may change the volume, average term, effective yields and

refinancing options of student loans under the FFELP or provide advantages to competing FFELP and

non-FFELP loan providers;

• demand and competition for education financing;

• financing preferences of students and their families;

• borrower default rates on Private Education Loans;

• continued access to the capital markets for funding at favorable spreads particularly for our non-

federally insured Private Education Loan portfolio; and

• our operating execution and efficiencies, including errors, omissions, and effectiveness of internal

control.

Our foreign currency exchange rate exposure is primarily the result of foreign denominated liabilities

issued by the Company. Cross-currency interest rate swaps are used to lock-in the exchange rate for the term

of the liability. In addition, the Company has foreign exchange rate exposure as a result of international

operations; however, the exposure is minimal at this time.

Political/Regulatory Risk

Because we operate in a federally sponsored loan program, we are subject to political and regulatory risk.

The Higher Education Act of 1965 (“HEA”) which authorizes the FFELP, is subject to comprehensive

reauthorization every five years and to frequent statutory and regulatory changes. Past changes included

reduced loan yields paid to lenders in 1993 and 1998, increased fees paid by lenders in 1993, decreased level

of the government guaranty in 1993 and reduced fees to guarantors and collectors, among others. The

Secretary of Education oversees and implements the HEA and periodically issues regulations and interpreta-

tions that may impact our business.

The HEA expired in 2003 and has since been extended by a series of temporary measures. Most recently,

the Third Higher Education Extension Act of 2007 extended the HEA programs through March 31, 2008. The

student loan programs under the HEA were reauthorized by the Higher Education Reconciliation Act

(“HERA”), which was enacted February 8, 2006. In addition, the president signed into law the College Cost

Reduction and Access Act (“CCRAA”) on September 27, 2007, and the Department of Education amended

the FFELP regulations on November 1, 2007. The statutory and regulatory changes included in the above

could have a material impact on the Company. See “RECENT DEVELOPMENTS” for additional discussion.

Liquidity Risk (See “LIQUIDITY AND CAPITAL RESOURCES)

Credit Risk

We bear the full risk of borrower and closed school losses experienced in our Private Education Loan

portfolio. These loans are underwritten and priced according to risk, generally determined by a commercially

104