Sallie Mae 2007 Annual Report Download - page 5

Download and view the complete annual report

Please find page 5 of the 2007 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

|

|

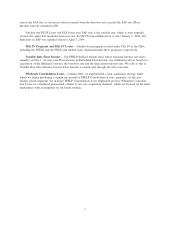

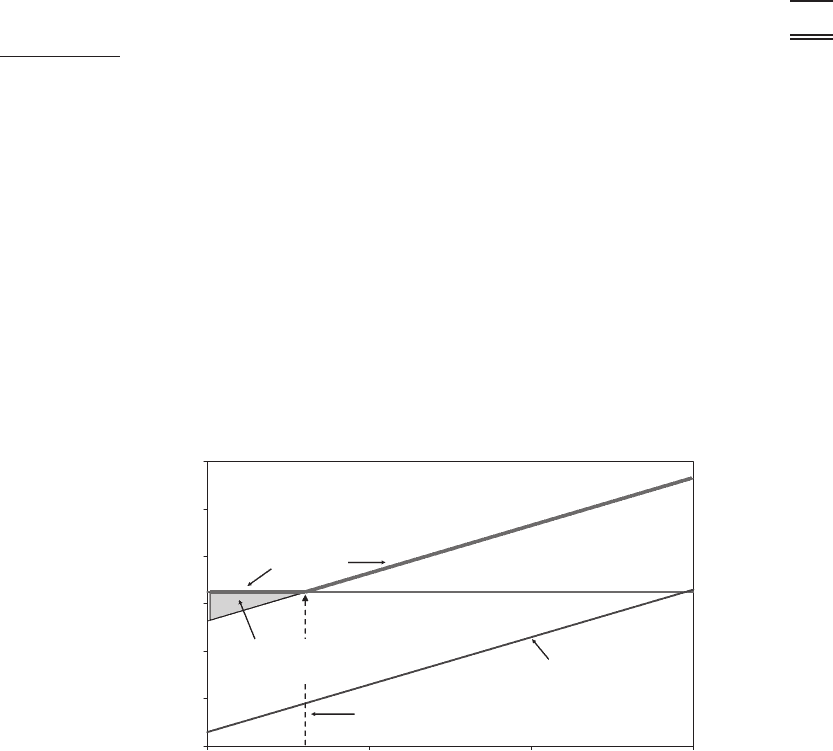

In accordance with new legislation enacted in 2006, lenders are required to rebate Floor Income to ED for all

new FFELP loans disbursed on or after April 1, 2006.

The following example shows the mechanics of Floor Income for a typical fixed rate FFELP Consolida-

tion Loan (with a commercial paper-based SAP spread of 2.64 percent):

Fixed Borrower Rate ...................................................... 7.25%

SAP Spread over Commercial Paper Rate ....................................... (2.64)%

Floor Strike Rate

(1)

........................................................ 4.61%

(1)

The interest rate at which the underlying index (Treasury bill or commercial paper) plus the fixed SAP spread equals the fixed

borrower rate. Floor Income is earned anytime the interest rate of the underlying index declines below this rate.

Based on this example, if the quarterly average commercial paper rate is over 4.61 percent, the holder of the

student loan will earn at a floating rate based on the SAP formula, which in this example is a fixed spread to

commercial paper of 2.64 percent. On the other hand, if the quarterly average commercial paper rate is below

4.61 percent, the SAP formula will produce a rate below the fixed borrower rate of 7.25 percent and the loan

holder earns at the borrower rate of 7.25 percent. The difference between the fixed borrower rate and the

lender’s expected yield based on the SAP formula is referred to as Floor Income. Our student loan assets are

generally funded with floating rate debt, so when student loans are earning at the fixed borrower rate,

decreases in interest rates may increase Floor Income.

Graphic Depiction of Floor Income:

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

10.00%

4.00% 5.00% 6.00% 7.00%

Commercial Paper Rate

Floor Strike Rate @ 4.61%

Lender Yield

Floor Income

Fixed Borrower Rate = 7.25%

Special Allowance Payment (SAP) Rate = 2.64%

Floating Debt Rate

Fixed Borrower Rate

Yield

Floor Income Contracts — We enter into contracts with counterparties under which, in exchange for an

upfront fee representing the present value of the Floor Income that we expect to earn on a notional amount of

underlying student loans being economically hedged, we will pay the counterparties the Floor Income earned

on that notional amount over the life of the Floor Income Contract. Specifically, we agree to pay the

counterparty the difference, if positive, between the fixed borrower rate less the SAP (see definition below)

spread and the average of the applicable interest rate index on that notional amount, regardless of the actual

balance of underlying student loans, over the life of the contract. The contracts generally do not extend over

the life of the underlying student loans. This contract effectively locks in the amount of Floor Income we will

earn over the period of the contract. Floor Income Contracts are not considered effective hedges under

SFAS No. 133, “Accounting for Derivative Instruments and Hedging Activities,” and each quarter we must

record the change in fair value of these contracts through income.

4