PNC Bank 2008 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2008 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

|

|

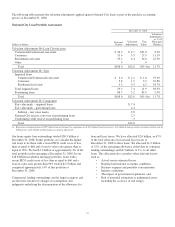

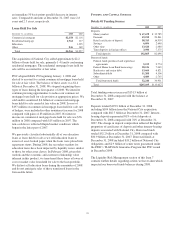

Assets of Market Street Funding LLC

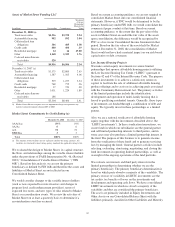

In millions Outstanding Commitments

Weighted

Average

Remaining

Maturity In

Years

December 31, 2008 (a)

Trade receivables $1,516 $3,370 2.34

Automobile financing 992 992 3.94

Collateralized loan

obligations 306 405 1.58

Credit cards 400 400 .19

Residential mortgage 14 14 27.00

Other 1,168 1,325 1.76

Cash and miscellaneous

receivables 520

Total $4,916 $6,506 2.34

December 31, 2007 (a)

Trade receivables $1,375 $2,865 2.63

Automobile financing 1,387 1,565 4.06

Collateralized loan

obligations 519 1,257 2.54

Credit cards 769 775 .26

Residential mortgage 37 720 .90

Other 1,031 1,224 1.89

Cash and miscellaneous

receivables 186

Total $5,304 $8,406 2.41

(a) Market Street did not recognize an asset impairment charge or experience any

material rating downgrades during 2007 or 2008.

Market Street Commitments by Credit Rating (a)

December 31, 2008 December 31, 2007

AAA/Aaa 19% 19%

AA/Aa 66

A/A 72 72

BBB/Baa 33

Total 100% 100%

(a) The majority of our facilities are not explicitly rated by the rating agencies. All

facilities are structured to meet rating agency standards for applicable rating levels.

We evaluated the design of Market Street, its capital structure,

the Note, and relationships among the variable interest holders

under the provisions of FASB Interpretation No. 46, (Revised

2003) “Consolidation of Variable Interest Entities” (“FIN

46R”). Based on this analysis, we are not the primary

beneficiary as defined by FIN 46R and therefore the assets and

liabilities of Market Street are not reflected in our

Consolidated Balance Sheet.

We would consider changes to the variable interest holders

(such as new expected loss note investors and changes to

program-level credit enhancement providers), terms of

expected loss notes, and new types of risks related to Market

Street as reconsideration events. We review the activities of

Market Street on at least a quarterly basis to determine if a

reconsideration event has occurred.

Based on current accounting guidance, we are not required to

consolidate Market Street into our consolidated financial

statements. However, if PNC would be determined to be the

primary beneficiary under FIN 46R, we would consolidate the

commercial paper conduit at that time. Based on current

accounting guidance, to the extent that the par value of the

assets in Market Street exceeded the fair value of the assets

upon consolidation, the difference would be recognized by

PNC as a loss in our Consolidated Income Statement in that

period. Based on the fair value of the assets held by Market

Street at December 31, 2008, the consolidation of Market

Street would not have had a material impact on our risk-based

capital ratios or debt covenants.

Low Income Housing Projects

We make certain equity investments in various limited

partnerships that sponsor affordable housing projects utilizing

the Low Income Housing Tax Credit (“LIHTC”) pursuant to

Sections 42 and 47 of the Internal Revenue Code. The purpose

of these investments is to achieve a satisfactory return on

capital, to facilitate the sale of additional affordable housing

product offerings and to assist us in achieving goals associated

with the Community Reinvestment Act. The primary activities

of the limited partnerships include the identification,

development and operation of multi-family housing that is

leased to qualifying residential tenants. Generally, these types

of investments are funded through a combination of debt and

equity. We typically invest in these partnerships as a limited

partner.

Also, we are a national syndicator of affordable housing

equity (together with the investments described above, the

“LIHTC investments”). In these syndication transactions, we

create funds in which our subsidiaries are the general partner

and sell limited partnership interests to third parties, and in

some cases may also purchase a limited partnership interest in

the fund. The purpose of this business is to generate income

from the syndication of these funds and to generate servicing

fees by managing the funds. General partner activities include

selecting, evaluating, structuring, negotiating, and closing the

fund investments in operating limited partnerships, as well as

oversight of the ongoing operations of the fund portfolio.

We evaluate our interests and third party interests in the

limited partnerships in determining whether we are the

primary beneficiary. The primary beneficiary determination is

based on which party absorbs a majority of the variability. The

primary sources of variability in LIHTC investments are the

tax credits, tax benefits of losses on the investments and

development and operating cash flows. We have consolidated

LIHTC investments in which we absorb a majority of the

variability and thus are considered the primary beneficiary.

The assets are primarily included in Equity Investments and

Other Assets on our Consolidated Balance Sheet with the

liabilities primarily classified in Other Liabilities and Minority

39