PNC Bank 2008 Annual Report Download - page 137

Download and view the complete annual report

Please find page 137 of the 2008 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

|

|

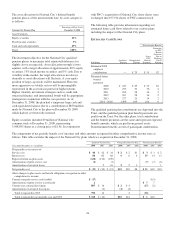

million were paid on January 30, 2007. The award payments

were funded by 17% in cash from BlackRock and

approximately one million shares of BlackRock common

stock transferred by PNC and distributed to LTIP participants.

As permitted under the award agreements, employees elected

to put 95% of the stock portion of the awards back to

BlackRock. These shares were retained by BlackRock as

treasury stock. We recognized a pretax gain of $82 million in

the first quarter of 2007 from the transfer of BlackRock

shares. The gain was included in other noninterest income and

reflected the excess of market value over book value of the

one million shares transferred in January 2007. Additional

BlackRock shares were distributed to LTIP participants during

the first quarter of 2008, resulting in a $3 million pretax gain

in other noninterest income.

BlackRock granted awards in 2007 under an additional LTIP

program, all of which are subject to achieving earnings

performance goals prior to the vesting date of September 29,

2011. Of the shares of BlackRock common stock that we have

agreed to transfer to fund their LTIP programs, approximately

1.6 million shares have been committed to fund the awards

vesting in 2011 and the amount remaining would then be

available for future awards.

Noninterest income for 2008 included a $243 million pretax

gain related to our commitment to fund additional BlackRock

LTIP programs. This gain represented the mark-to-market

adjustment related to our remaining BlackRock LTIP common

shares obligation as of December 31, 2008 and resulted from

the decrease in the market value of BlackRock common shares

for 2008. Noninterest income for 2007 and 2006 included

pretax charges totaling $209 million and $12 million,

respectively, related to an increase in the market value of

BlackRock common shares for these periods.

Additionally, we reported noninterest expense of $33 million

in 2006 related to the BlackRock LTIP awards.

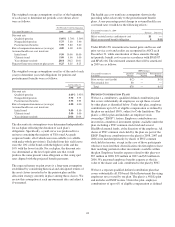

N

OTE

17 F

INANCIAL

D

ERIVATIVES

We use a variety of derivative financial instruments to help

manage interest rate, market and credit risk and reduce the

effects that changes in interest rates may have on net income,

fair value of assets and liabilities, and cash flows. These

instruments include interest rate swaps, interest rate caps and

floors, futures contracts, and total return swaps.

Fair Value Hedging Strategies

We enter into interest rate swaps, caps, floors and futures

derivative contracts to hedge bank notes, Federal Home Loan

Bank borrowings, senior debt and subordinated debt for

changes in fair value primarily due to changes in interest rates.

Adjustments related to the ineffective portion of fair value

hedging instruments are recorded in interest expense or

noninterest income depending on the hedged item.

Cash Flow Hedging Strategies

We enter into interest rate swap contracts to modify the

interest rate characteristics of designated commercial loans

from variable to fixed in order to reduce the impact of changes

in future cash flows due to interest rate changes. We hedged

our exposure to the variability of future cash flows for all

forecasted transactions for a maximum of 10 years for hedges

converting floating-rate commercial loans to fixed. The fair

value of these derivatives is reported in other assets or other

liabilities and offset in accumulated other comprehensive

income (loss) for the effective portion of the derivatives. We

subsequently reclassify any unrealized gains or losses related

to these swap contracts from accumulated other

comprehensive income (loss) into interest income in the same

period or periods during which the hedged forecasted

transaction affects earnings. Ineffectiveness of the strategies,

if any, is recognized immediately in earnings.

During the next twelve months, we expect to reclassify to

earnings $230 million of pretax net gains, or $149 million

after-tax, on cash flow hedge derivatives currently reported in

accumulated other comprehensive loss. This amount could

differ from amounts actually recognized due to changes in

interest rates and the addition of other hedges subsequent to

December 31, 2008. These net gains are anticipated to result

from net cash flows on receive fixed interest rate swaps that

would impact interest income recognized on the related

floating rate commercial loans.

As of December 31, 2008 we have determined that there were

no hedging positions where it was probable that certain

forecasted transactions may not occur within the originally

designated time period.

The ineffective portion of the change in value of our fair value

and cash flow hedge derivatives resulted in a net gain of $8

million for 2008, a net loss of $1 million for 2007, and a net

loss of $4 million in 2006.

Free-Standing Derivatives

To accommodate customer needs, we also enter into financial

derivative transactions primarily consisting of interest rate

swaps, interest rate caps and floors, futures, swaptions, and

foreign exchange and equity contracts. We primarily manage

our market risk exposure from customer positions through

transactions with third-party dealers. The credit risk associated

with derivatives executed with customers is essentially the

same as that involved in extending loans and is subject to

normal credit policies. We may obtain collateral based on our

assessment of the customer. For derivatives not designated as

an accounting hedge, the gain or loss is recognized in

noninterest income.

Also included in free-standing derivatives are transactions that

we enter into for risk management and proprietary purposes

that are not designated as accounting hedges, primarily

interest rate, basis and total rate of return swaps, interest rate

133