PNC Bank 2008 Annual Report Download - page 108

Download and view the complete annual report

Please find page 108 of the 2008 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

|

|

PNC REIT Corp., PNC has committed to purchase such

in-kind dividend from the applicable PNC REIT Corp. holders

in exchange for a cash payment representing the market value

of such in-kind dividend, and PNC has committed to

contribute such in-kind dividend to PNC Bank, N.A.

N

OTE

4L

OANS

,C

OMMITMENTS TO

E

XTEND

C

REDIT AND

C

ONCENTRATIONS OF

C

REDIT

R

ISK

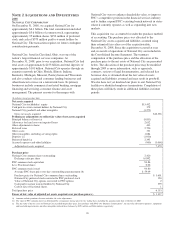

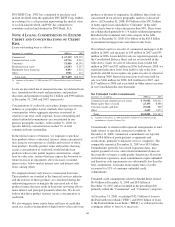

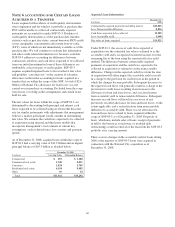

Loans outstanding were as follows:

December 31 - in millions 2008 (a) 2007

Commercial $ 67,319 $28,539

Commercial real estate 25,736 8,903

Consumer 52,489 18,393

Residential real estate 21,583 9,557

Equipment lease financing 6,461 2,514

Other 1,901 413

Total loans $175,489 $68,319

(a) Amounts at December 31, 2008 include $99.7 billion of loans related to National

City.

Loans are presented net of unearned income, net deferred loan

fees, unamortized discounts and premiums, and purchase

discounts and premiums totaling $4.1 billion and $990 million

at December 31, 2008 and 2007, respectively.

Concentrations of credit risk exist when changes in economic,

industry or geographic factors similarly affect groups of

counterparties whose aggregate exposure is material in

relation to our total credit exposure. Loans outstanding and

related unfunded commitments are concentrated in our

primary geographic markets. At December 31, 2008, no

specific industry concentration exceeded 7% of total

commercial loans outstanding.

In the normal course of business, we originate or purchase

loan products whose contractual features, when concentrated,

may increase our exposure as a holder and servicer of those

loan products. Possible product terms and features that may

create a concentration of credit risk would include loan

products whose terms permit negative amortization, a high

loan-to-value ratio, features that may expose the borrower to

future increases in repayments above increases in market

interest rates, below-market interest rates and interest-only

loans, among others.

We originate interest-only loans to commercial borrowers.

These products are standard in the financial services industry

and the features of these products are considered during the

underwriting process to mitigate the increased risk of this

product feature that may result in borrowers not being able to

make interest and principal payments when due. We do not

believe that these product features create a concentration of

credit risk.

We also originate home equity loans and lines of credit that

result in a credit concentration of high loan-to-value ratio loan

products at the time of origination. In addition, these loans are

concentrated in our primary geographic markets as discussed

above. At December 31, 2008, $6.8 billion of the $38.3 billion

of home equity loans (included in “Consumer” in the table

above) had a loan-to-value ratio greater than 90%. These loans

are collateralized primarily by 1-4 family residential properties.

Included in the residential real estate category in the table

above, at December 31, 2008, $5.6 billion of the $18.8 billion

of residential mortgage loans were interest-only loans.

We realized a net loss on sales of commercial mortgages of $6

million in 2008, and net gains of $39 million in 2007 and $55

million in 2006. Loans held for sale are reported separately on

the Consolidated Balance Sheet and are not included in the

table above. Gains on sales of education loans totaled $24

million in 2007 and $33 million in 2006. In February 2008, we

transferred education loans from held for sale to the loan

portfolio and did not recognize any gains on sales of education

loans during 2008. Interest income from total loans held for

sale was $166 million for 2008, $184 million for 2007, and

$157 million for 2006 and is included in Other interest income

in our Consolidated Income Statement.

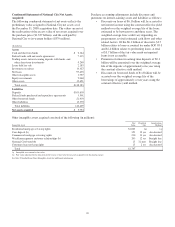

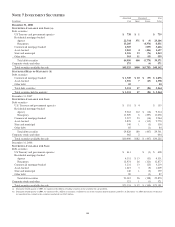

Net Unfunded Credit Commitments

December 31 - in millions 2008 (a) 2007

Commercial and commercial real estate $ 59,982 $42,021

Home equity lines of credit 23,195 8,680

Consumer credit card lines 19,028 969

Other 2,683 1,677

Total $104,888 $53,347

(a) Amounts at December 31, 2008 include $53.9 billion of net unfunded credit

commitments related to National City.

Commitments to extend credit represent arrangements to lend

funds subject to specified contractual conditions. At

December 31, 2008, commercial commitments are reported

net of $8.6 billion of participations, assignments and

syndications, primarily to financial services companies. The

comparable amount at December 31, 2007 was $8.9 billion.

Commitments generally have fixed expiration dates, may

require payment of a fee, and contain termination clauses in

the event the customer’s credit quality deteriorates. Based on

our historical experience, most commitments expire unfunded,

and therefore cash requirements are substantially less than the

total commitment. Consumer home equity lines of credit

accounted for 55% of consumer unfunded credit

commitments.

Unfunded credit commitments related to Market Street totaled

$6.4 billion at December 31, 2008 and $8.8 billion at

December 31, 2007 and are included in the preceding table

primarily within the “Commercial” and “Consumer” categories.

At December 31, 2008, we pledged $32.9 billion of loans to

the Federal Reserve Bank (“FRB”) and $50.0 billion of loans

to the Federal Home Loan Bank (“FHLB”) as collateral for the

contingent ability to borrow, if necessary.

104