PNC Bank 2008 Annual Report Download - page 42

Download and view the complete annual report

Please find page 42 of the 2008 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

|

|

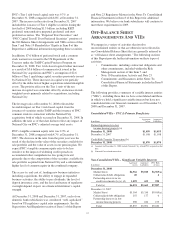

(a) PNC’s risk of loss consists of off-balance sheet liquidity commitments to Market

Street of $6.4 billion and other credit enhancements of $.6 billion at December 31,

2008. The comparable amounts were $8.8 billion and $.2 billion at December 31,

2007. These liquidity commitments are included in the Net Unfunded Credit

Commitments table in the Consolidated Balance Sheet Review section of this

Report.

(b) Amounts reported primarily represent low income housing projects.

(c) Amounts include the impact of National City.

(d) Aggregate assets and aggregate liabilities at December 31, 2008 represent

approximate balances due to limited availability of financial information associated

with the acquired National City partnerships that we did not sponsor.

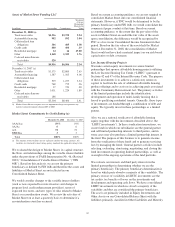

Market Street

Market Street Funding LLC (“Market Street”) is a multi-seller

asset-backed commercial paper conduit that is owned by an

independent third party. Market Street’s activities primarily

involve purchasing assets or making loans secured by interests

in pools of receivables from US corporations that desire

access to the commercial paper market. Market Street funds

the purchases of assets or loans by issuing commercial paper

which has been rated A1/P1 by Standard & Poor’s and

Moody’s, respectively, and is supported by pool-specific

credit enhancements, liquidity facilities and program-level

credit enhancement. Generally, Market Street mitigates its

potential interest rate risk by entering into agreements with its

borrowers that reflect interest rates based upon its weighted

average commercial paper cost of funds. During 2007 and

2008, Market Street met all of its funding needs through the

issuance of commercial paper.

Market Street commercial paper outstanding was $4.4 billion

at December 31, 2008 and $5.1 billion at December 31, 2007.

The weighted average maturity of the commercial paper was

24 days at December 31, 2008 compared with 32 days at

December 31, 2007.

Effective October 28, 2008, Market Street was approved to

participate in the Federal Reserve’s CPFF authorized under

Section 13(3) of the Federal Reserve Act. The CPFF

commitment to purchase up to $5.4 billion of three-month

Market Street commercial paper expires on October 30, 2009.

As of December 31, 2008, Market Street’s participation in this

program totaled $445 million. These trades matured at the end

of January 2009 and were replaced with commercial paper

sold to investors.

In the ordinary course of business during 2008, PNC Capital

Markets, acting as a placement agent for Market Street, held a

maximum daily position in Market Street commercial paper of

$75 million with an average of $12 million. This compares

with a maximum daily position of $113 million with an

average of $27 million for the year ended December 31, 2007.

PNC Capital Markets owned no Market Street commercial

paper at December 31, 2008 and owned less than $1 million of

such commercial paper at December 31, 2007. PNC Bank,

National Association (“PNC Bank, N.A.”) purchased

overnight maturities of Market Street commercial paper on

two days during September 2008 in the amounts of $197

million and $531 million and one day during October 2008 in

the amount of $278 million due to illiquidity in the

commercial paper market. We considered these transactions as

part of our evaluation of Market Street described below to

determine that we are not the primary beneficiary. PNC made

no other purchases of Market Street commercial paper during

2007 or 2008.

PNC Bank, N.A. provides certain administrative services, the

program-level credit enhancement and 99% of liquidity

facilities to Market Street in exchange for fees negotiated

based on market rates. PNC recognized program administrator

fees and commitment fees related to PNC’s portion of the

liquidity facilities of $21 million and $4 million, respectively,

for the year ended December 31, 2008. The comparable

amounts were $13 million and $4 million for the year ended

December 31, 2007.

The commercial paper obligations at December 31, 2008 and

December 31, 2007 were effectively collateralized by Market

Street’s assets. While PNC may be obligated to fund under the

$6.4 billion of liquidity facilities for events such as

commercial paper market disruptions, borrower bankruptcies,

collateral deficiencies or covenant violations, our credit risk

under the liquidity facilities is secondary to the risk of first

loss provided by the borrower or another third party in the

form of deal-specific credit enhancement, such as by the over

collateralization of the assets. Deal-specific credit

enhancement that supports the commercial paper issued by

Market Street is generally structured to cover a multiple of

expected losses for the pool of assets and is sized to generally

meet rating agency standards for comparably structured

transactions. In addition, PNC would be required to fund $1.0

billion of the liquidity facilities if the underlying assets are in

default. See Note 25 Commitments And Guarantees included

in the Notes To Consolidated Financial Statements of this

Report for additional information.

PNC provides program-level credit enhancement to cover net

losses in the amount of 10% of commitments, excluding

explicitly rated AAA/Aaa facilities. PNC provides 100% of

the enhancement in the form of a cash collateral account

funded by a loan facility. This facility expires in March 2013.

Until November 25, 2008, PNC provided only 25% of the

enhancement in the form of a cash collateral account funded

by a loan facility and provided a liquidity facility for the

remaining 75% of program-level enhancement.

Market Street has entered into a Subordinated Note Purchase

Agreement (“Note”) with an unrelated third party. The Note

provides first loss coverage whereby the investor absorbs

losses up to the amount of the Note, which was $6.6 million as

of December 31, 2008. Proceeds from the issuance of the Note

are held by Market Street in a first loss reserve account that

will be used to reimburse any losses incurred by Market

Street, PNC Bank, N.A. or other providers under the liquidity

facilities and the credit enhancement arrangements.

38