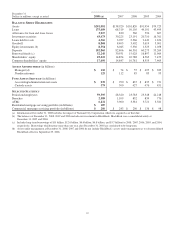

PNC Bank 2008 Annual Report Download - page 20

Download and view the complete annual report

Please find page 20 of the 2008 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

|

|

Over the last several years, there has been an increasing

regulatory focus on compliance with anti-money laundering

laws and regulations, resulting in, among other things, several

significant publicly-announced enforcement actions. There

has also been a heightened focus recently, by customers and

the media as well as by regulators, on the protection of

confidential customer information. A failure to have adequate

procedures to comply with anti-money laundering laws and

regulations or to protect the confidentiality of customer

information could expose us to damages, fines and regulatory

penalties, which could be significant, and could also injure our

reputation with customers and others with whom we do

business.

We must comply with generally accepted accounting

principles established by the Financial Accounting

Standards Board, accounting, disclosure and other rules

set forth by the SEC, income tax and other regulations

established by the US Department of the Treasury, and

revenue rulings and other guidance issued by the Internal

Revenue Service, which affect our financial condition and

results of operations.

Changes in accounting standards, or interpretations of those

standards, can impact our revenue recognition and expense

policies and affect our estimation methods used to prepare the

consolidated financial statements. Changes in income tax

regulations, revenue rulings, revenue procedures, and other

guidance can impact our tax liability and alter the timing of

cash flows associated with tax deductions and payments. New

guidance often dictates how changes to standards and

regulations are to be presented in our consolidated financial

statements, as either an adjustment to beginning retained

earnings for the period or as income or expense in current

period earnings. In some cases, changes may be applied to

previously reported disclosures.

The determination of the amount of loss allowances and

impairments taken on our assets is highly subjective and

could materially impact our results of operations or

financial position.

The determination of the amount of loss allowances and asset

impairments varies by asset type and is based upon our

periodic evaluation and assessment of known and inherent

risks associated with the respective asset class. Such

evaluations and assessments are revised as conditions change

and new information becomes available. Management updates

its evaluations regularly and reflects changes in allowances

and impairments in operations as such evaluations are revised.

There can be no assurance that our management has

accurately assessed the level of impairments taken and

allowances reflected in our financial statements. Furthermore,

additional impairments may need to be taken or allowances

provided for in the future. Historical trends may not be

indicative of future impairments or allowances.

Our asset valuation may include methodologies,

estimations and assumptions that are subject to differing

interpretations and could result in changes to asset

valuations that may materially adversely affect our results

of operations or financial condition.

We must use estimates, assumptions, and judgments when

financial assets and liabilities are measured and reported at

fair value. Assets and liabilities carried at fair value inherently

result in a higher degree of financial statement volatility. Fair

values and the information used to record valuation

adjustments for certain assets and liabilities are based on

quoted market prices and/or other observable inputs provided

by independent third-party sources, when available. When

such third-party information is not available, we estimate fair

value primarily by using cash flows and other financial

modeling techniques utilizing assumptions such as credit

quality, liquidity, interest rates and other relevant inputs.

Changes in underlying factors, assumptions, or estimates in

any of these areas could materially impact our future financial

condition and results of operations.

During periods of market disruption, including periods of

significantly rising or high interest rates, rapidly widening

credit spreads or illiquidity, it may be difficult to value certain

of our assets if trading becomes less frequent and/or market

data becomes less observable. There may be certain asset

classes that were in active markets with significant observable

data that become illiquid due to the current financial

environment. In such cases, certain asset valuations may

require more subjectivity and management judgment. As such,

valuations may include inputs and assumptions that are less

observable or require greater estimation. Further, rapidly

changing and unprecedented credit and equity market

conditions could materially impact the valuation of assets as

reported within our consolidated financial statements, and the

period-to-period changes in value could vary significantly.

Decreases in value may have a material adverse effect on our

results of operations or financial condition.

Our business and financial performance could be adversely

affected, directly or indirectly, by natural disasters, by

terrorist activities or by international hostilities.

The impact of natural disasters, terrorist activities and

international hostilities cannot be predicted with respect to

severity or duration. However, any of these could impact us

directly (for example, by causing significant damage to our

facilities or preventing us from conducting our business in the

ordinary course), or could impact us indirectly through a

direct impact on our borrowers, depositors, other customers,

suppliers or other counterparties. We could also suffer adverse

consequences to the extent that natural disasters, terrorist

activities or international hostilities affect the economy and

capital and other financial markets generally. These types of

impacts could lead, for example, to an increase in

delinquencies, bankruptcies or defaults that could result in our

experiencing higher levels of nonperforming assets, net

charge-offs and provisions for credit losses.

16