The Hartford 2014 Annual Report Download - page 91

Download and view the complete annual report

Please find page 91 of the 2014 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

|

|

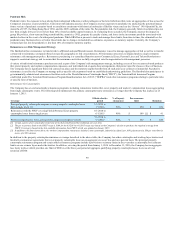

In addition to the reinsurance protection provided by The Hartford's traditional property catastrophe reinsurance program described above, until February 18,

2015, the Hartford had a fully collateralized reinsurance coverage from Foundation Re III for losses sustained from qualifying hurricane loss events. Under

the terms of the treaty, the Company had coverage for losses from hurricanes using a customized industry index contract designed to replicate The Hartford's

own catastrophe losses, with a provision that the actual losses incurred by the Company for covered events, net of reinsurance recoveries, cannot be less than

zero.

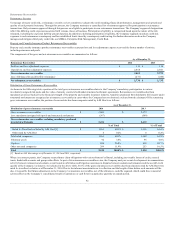

The following table summarizes the terms of the reinsurance treaty with Foundation Re III that was in place as of December 31, 2014:

Hurricane loss events affecting the Gulf and

Eastern Coast of the United States

2/18/2011 to

2/18/2015

At the time of the purchase, 67.5% of $200 in losses in

excess of an index loss trigger equating to approximately

$1.4 billion in losses to The Hartford

$135

There have been no events that are expected to trigger a recovery under the Foundation Re III reinsurance program and, accordingly, the Company has not

recorded any recoveries from the associated reinsurance treaty. The Company did not replace the Foundation Re III treaty when it expired in February 2015.

Reinsurance for Terrorism

For the risk of terrorism, private sector catastrophe reinsurance capacity is generally limited and largely unavailable for terrorism losses caused by nuclear,

biological, chemical or radiological weapons attacks. As such, the Company's principal reinsurance protection against large-scale terrorist attacks is the

coverage currently provided through the TRIPRA 2015. On January 12, 2015, the President signed TRIPRA 2015, extending TRIPRA 2007, through the end

of 2020. TRIPRA 2015 provides a backstop for insurance-related losses resulting from any “act of terrorism”, which is certified by the Secretary of Homeland

Security and Attorney General and requires consultation by the Secretary of Treasury, for losses that that exceed a threshold of industry losses of $100 in

2015, and continue to increase to $200 by 2020. Under the program, in any one calendar year, the federal government would pay losses of 85% in 2015,

which then continue to decrease 1% annually, starting on January 1st, 2016, down to 80% by the year 2020, from a certified act of terrorism after an insurer's

losses exceed 20% of the Company's eligible direct commercial earned premiums of the prior calendar year up to a combined annual aggregate limit for the

federal government and all insurers of $100 billion. The Company's estimated deductible under the program is $1.19 billion for 2015. If an act of terrorism or

acts of terrorism result in covered losses exceeding the $100 billion annual industry aggregate limit, a future Congress would be responsible for determining

how additional losses in excess of $100 billion will be paid.

Among other items, TRIPRA required that the President's Working Group on Financial Markets (“PWG”) continue to perform an analysis regarding the long-

term availability and affordability of insurance for terrorism risk. Among the findings detailed in the PWG's initial report, released October 2, 2006, were that

the high level of uncertainty associated with predicting the frequency of terrorist attacks, coupled with the unwillingness of some insurance policyholders to

purchase insurance coverage, makes predicting long-term development of the terrorism risk market difficult, and that there is likely little potential for future

market development for NBCR coverage. The January 2011 PWG report notes some improvements in capacity and modeling, but also noted that take-up

rates for terrorism coverage remained relatively flat over the past three years and that insurers remain uncertain about the ability of models to predict the

frequency and severity of terrorist attacks. The April 2014 PWG report notes that the availability and affordability of insurance for terrorism risk has not

changed appreciably since 2010. Take up rates have increased since the first year of TRIA and are stable at 60% in the aggregate. The private market does not

have capacity to provide reinsurance for terrorism risk to the extent provided by TRIPRA. With respect to NBCR coverage, a December 2008 study by the

U.S. Government Accountability Office (“GAO”) found that property and casualty insurers still generally seek to exclude NBCR coverage from their

commercial policies when permitted. However, while nuclear, pollution and contamination exclusions are contained in many property and liability insurance

policies, the GAO report concluded that such exclusions may be subject to challenges in court because they were not specifically drafted to address terrorist

attacks. Furthermore, workers compensation policies generally have no exclusion or limitations. The GAO found that commercial property and casualty

policyholders, including companies that own high-value properties in large cities, generally reported that they could not obtain NBCR coverage.

Commercial property and casualty insurers generally remain unwilling to offer NBCR coverage because of uncertainties about the risk and the potential for

catastrophic losses.

91