The Hartford 2014 Annual Report Download - page 110

Download and view the complete annual report

Please find page 110 of the 2014 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

|

|

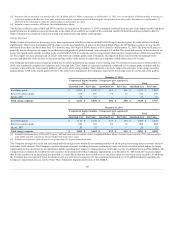

The Company’s European investment exposure largely relates to corporate entities which are domiciled in or generated a significant portion of its revenue

within the United Kingdom, Germany, the Netherlands and Switzerland. Entities domiciled in the United Kingdom comprise the Company's largest exposure;

as of December 31, 2014 and 2013, the exposure totals less than 3% of total invested assets. The majority of the European investments are U.S. dollar-

denominated, and those securities that are pound and euro-denominated are hedged to U.S. dollars or support foreign-denominated liabilities. For a

discussion of foreign currency risks, see the Foreign Currency Exchange Risk section of this MD&A. The Company does not hold any sovereign exposure to

the peripheral region and does not hold any exposure to issuers in Greece. As of December 31, 2014 and 2013, the Company’s unfunded commitments

associated with its investment portfolio was immaterial, and the weighted average credit quality of European investments was A- and A-, respectively.

As of December 31, 2014 and 2013, the Company’s credit default swaps that provide credit protection on European issuers had a notional amount of $44 and

$190, respectively, and a fair value of $0 and $(1), respectively. As of December 31, 2014 and 2013 these credit default swaps that reference single name

corporate and financial European issuers, of which a notional value of $3 and $23, respectively, related to the peripheral region. The maturity dates of credit

defaults swaps are primarily consistent with the hedged bonds. For further information on the use of the Company’s credit derivatives and counterparty credit

quality, see Derivative Instruments within the Credit Risk section of this MD&A.

In addition to the credit risk associated with the investment portfolio, the Company has $231 of reinsurance recoverables due from legal entity counterparties

domiciled within Europe. For a more detail discussion of the Company's reinsurance arrangements, see Note 7 - Reinsurance of Notes to Consolidated

Financial Statements.

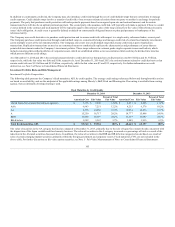

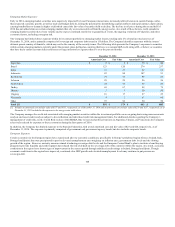

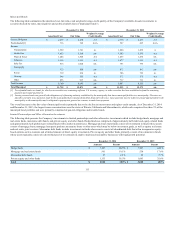

Financial Services

The Company’s exposure to the financial services sector is predominantly through investment grade banking and insurance institutions. The following table

presents the Company’s fixed maturity, AFS and equity, AFS securities in the financial services sector that are included in the Securities by Type table above.

AAA $ 31 $ 34 $ 3 $ 49 $ 52 $ 3

AA 401 436 35 468 493 25

A 2,610 2,804 194 2,518 2,616 98

BBB 1,681 1,734 53 1,978 1,952 (26)

BB & below 368 407 39 264 288 24

The Company's exposure to the financial services sector remained relatively consistent, as the impact of sales was largely offset by higher valuations due to a

decline in interest rates.

Commercial Real Estate

Commercial real estate market fundamentals, including property prices, financial conditions, transaction volume, and delinquencies, continue to improve. In

addition, the availability of credit has increased and there is now less concern about the ability of borrowers to refinance as loans come due.

110