The Hartford 2014 Annual Report Download - page 67

Download and view the complete annual report

Please find page 67 of the 2014 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

|

|

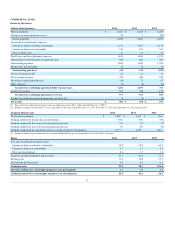

Core Earnings

Core earnings, a non-GAAP measure, is an important measure of the Company’s operating performance. The Company believes that core earnings provides

investors with a valuable measure of the performance of the Company’s ongoing businesses because it reveals trends in our insurance and financial services

businesses that may be obscured by including the net effect of certain realized capital gains and losses, discontinued operations, pension settlements, loss on

extinguishment of debt, gains and losses on business disposition transactions, certain restructuring and other costs and the impact of Unlocks to DAC, SIA,

URR and death and other insurance benefit reserve balances. Some realized capital gains and losses are primarily driven by investment decisions and external

economic developments, the nature and timing of which are unrelated to the insurance and underwriting aspects of our business. Accordingly, core earnings

excludes the effect of all realized gains and losses (net of tax and the effects of DAC) that tend to be highly variable from period to period based on capital

market conditions. The Company believes, however, that some realized capital gains and losses are integrally related to our insurance operations, so core

earnings includes net realized gains and losses such as net periodic settlements on credit derivatives. These net realized gains and losses are directly related

to an offsetting item included in the income statement such as net investment income. Net income (loss) is the most directly comparable U.S. GAAP measure.

Core earnings should not be considered as a substitute for net income (loss) and does not reflect the overall profitability of the Company’s business.

Therefore, the Company believes that it is useful for investors to evaluate both net income (loss) and core earnings when reviewing the Company’s

performance.

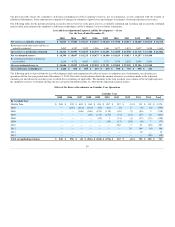

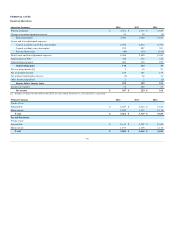

A reconciliation of net income to core earnings is set forth below:

Less: Unlock charge, after-tax

(62)

(109)

(138)

Less: Restructuring and other costs, after-tax

(49)

(44)

(129)

Less: Loss from discontinued operations, after-tax

(551)

(1,049)

(258)

Less: Pension settlement, after-tax

(83)

—

—

Less: Loss on extinguishment of debt, after-tax

—

(138)

(587)

Less: Net reinsurance gain (loss) on dispositions, after-tax

15

(24)

(388)

Less: Net realized capital gains (losses), after-tax and DAC, excluded from core earnings [1]

(20)

121

340

[1] Excludes net realized gain on dispositions of $1.0 billion, after-tax, for the year ended December 31, 2013 relating to the sales of the Retirement Plans and Individual Life

businesses which are included in net reinsurance loss on dispositions, after-tax.

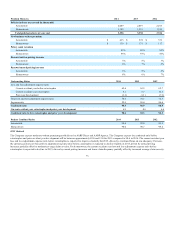

Current accident year loss and loss adjustment expense ratio before catastrophes

The current accident year loss and loss adjustment expense ratio before catastrophes is a measure of the cost of non-catastrophe claims incurred in the current

accident year divided by earned premiums. Management believes that the current accident year loss and loss adjustment expense ratio before catastrophes is

a performance measure that is useful to investors as it removes the impact of volatile and unpredictable catastrophe losses and prior accident year reserve

development.

Expense ratio

The expense ratio for the underwriting segments of Commercial Lines and Personal Lines is the ratio of underwriting expenses to earned premiums.

Underwriting expenses include the amortization of deferred policy acquisition costs and insurance operating costs and expenses, including certain

centralized services and bad debt expense. Deferred policy acquisition costs include commissions, taxes, licenses and fees and other underwriting expenses

and are amortized over the policy term.

The expense ratio for Group Benefits is expressed as the ratio of insurance operating costs and other expenses and amortization of deferred policy acquisition

costs, to premiums and other considerations, excluding buyout premiums.

Fee Income

Fee income is largely driven from amounts collected as a result of contractually defined percentages of assets under management. These fees are generally

collected on a daily basis. Therefore, the growth in assets under management either through positive net flows or net sales, or favorable equity market

performance will have a favorable impact on fee income. Conversely, either negative net flows or net sales, or unfavorable equity market performance will

reduce fee income.

67