The Hartford 2014 Annual Report Download - page 90

Download and view the complete annual report

Please find page 90 of the 2014 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

|

|

Pandemic risk is the exposure to loss arising from widespread influenza or other pathogens or bacterial infections that create an aggregation of loss across the

Company's insurance or asset portfolios. Consistent with industry practice, the Company assesses exposure to pandemics by analyzing the potential impact

from a variety of pandemic scenarios based on conditions consistent with historical outbreaks of flu-like viruses such as the “Severe” 1918 Spanish Flu, the

Asian flu of 1957, the Hong Kong flu of 1968, and the 2009 outbreak of the swine flu. For pandemic risk, the Company generally limits its estimated pre-tax

loss from a single 250 year event to less than 10% of total available capital resources. In evaluating these scenarios, the Company assesses the impact on

group life policies, short-term and long term disability, annuities, COLI, property & casualty claims, and losses in the investment portfolio associated with

market declines in the event of a widespread pandemic. While ERM has a process to track and manage these limits, from time to time, the estimated loss for

pandemics may fluctuate above or below these limits due to changes in modeled loss estimates, exposures, or statutory surplus. Currently, the Company's

estimated pre-tax loss for pandemic is less than 10% of enterprise statutory surplus.

The Hartford utilizes reinsurance to transfer risk to affiliated and unaffiliated insurers. Reinsurance is used to manage aggregation of risk as well as to transfer

certain risk to reinsurance companies based on specific geographic or risk concentrations. All reinsurance processes are aligned under a single enterprise

reinsurance risk management policy. Reinsurance purchasing is a centralized function across Commercial Lines, Personal Lines and Talcott Resolution to

support a consistent strategy and to ensure that the reinsurance activities are fully integrated into the organization's risk management processes.

A variety of traditional reinsurance products are used as part of the Company's risk management strategy, including excess of loss occurrence-based products

that protect property and workers compensation exposures, and individual risk or quota share arrangements, that protect specific classes or lines of business.

The Company has no significant finite risk contracts in place and the statutory surplus benefit from all such prior year contracts is immaterial. Facultative

reinsurance is used by the Company to manage policy-specific risk exposures based on established underwriting guidelines. The Hartford also participates in

governmentally administered reinsurance facilities such as the Florida Hurricane Catastrophe Fund (“FHCF”), the Terrorism Risk Insurance Program

established under The Terrorism Risk Insurance Program Reauthorization Act of 2015 (“TRIPRA”) and other reinsurance programs relating to particular risks

or specific lines of business.

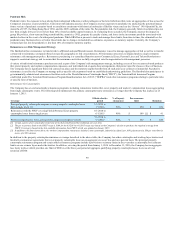

Reinsurance for Catastrophes

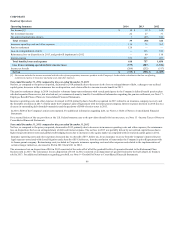

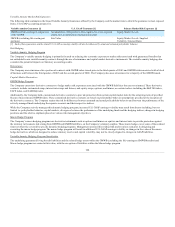

The Company has several catastrophe reinsurance programs, including reinsurance treaties that cover property and workers’ compensation losses aggregating

from single catastrophe events. The following table summarizes the primary catastrophe treaty reinsurance coverages that the Company has in place as of

January 1, 2015:

Principal property catastrophe program covering property catastrophe losses

from a single event [1]

1/1/2015 to

1/1/2016

90%

$ 850

$ 350

Reinsurance with the FHCF covering Florida Personal Lines property

catastrophe losses from a single event

6/1/2014 to

6/1/2015

90%

$ 109 [2] $ 41

Workers compensation losses arising from a single catastrophe event [3]

7/1/2014 to

7/1/2015

80%

$ 350

$ 100

[1] Certain aspects of our catastrophe treaty have terms that extend beyond the traditional one year term.

[2] The per occurrence limit on the FHCF treaty is $109 for the 6/1/2014 to 6/1/2015 treaty year based on the Company's election to purchase the required coverage from

FHCF. Coverage is based on the best available information from FHCF, which was updated in January 2015.

[3] In addition to the limit shown above, the workers compensation reinsurance includes a non-catastrophe, industrial accident layer, 80% placement of a $30 per event limit in

excess of a $20 retention.

In addition to the property catastrophe reinsurance coverage described in the above table, the Company has other catastrophe and working layer treaties and

facultative reinsurance agreements that cover property catastrophe losses on an aggregate excess of loss and on a per risk basis. The principal property

catastrophe reinsurance program and certain other reinsurance programs include a provision to reinstate limits in the event that a catastrophe loss exhausts

limits on one or more layers under the treaties. In addition, covering the period from January 1, 2014 to December 31, 2016, the Company has an aggregate

loss treaty in place which provides one limit of $200 over the three-year period of aggregate qualifying property catastrophe losses in excess of a net

retention of $860.

90