The Hartford 2014 Annual Report Download - page 122

Download and view the complete annual report

Please find page 122 of the 2014 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

|

|

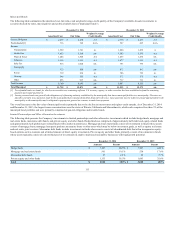

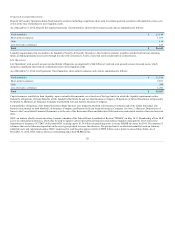

Total Life contractholder obligations $ 186,943

Less: Separate account assets [1] 134,702

Contracts without a surrender provision and/or fixed payout dates [2] $ 22,135

U.S. Fixed MVA annuities and Other [3] 8,748

Guaranteed investment contracts (“GIC”) [4] 26

Other [5] 21,332

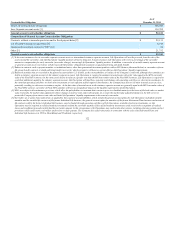

[1] In the event customers elect to surrender separate account assets or international statutory separate accounts, Life Operations will use the proceeds from the sale of the

assets to fund the surrender, and Life Operations’ liquidity position will not be impacted. In many instances Life Operations will receive a percentage of the surrender

amount as compensation for early surrender (surrender charge), increasing Life Operations’ liquidity position. In addition, a surrender of variable annuity separate account

or general account assets (see below) will decrease Life Operations’ obligation for payments on guaranteed living and death benefits.

[2] Relates to contracts such as payout annuities or institutional notes, other than guaranteed investment products with an MVA feature (discussed below) or surrenders of term

life, group benefit contracts or death and living benefit reserves for which surrenders will have no current effect on Life Operations’ liquidity requirements.

[3] Relates to annuities that are recorded in the general account (under U.S. GAAP), as the contractholders are subject to the Company's credit risk, although these annuities are

held in a statutory separate account. In the statutory separate account, Life Operations is required to maintain invested assets with a fair value equal to the MVA surrender

value of the Fixed MVA contract. In the event assets decline in value at a greater rate than the MVA surrender value of the Fixed MVA contract, Life Operations is required to

contribute additional capital to the statutory separate account. Life Operations will fund these required contributions with operating cash flows or short-term investments. In

the event that operating cash flows or short-term investments are not sufficient to fund required contributions, the Company may have to sell other invested assets at a loss,

potentially resulting in a decrease in statutory surplus. As the fair value of invested assets in the statutory separate account are generally equal to the MVA surrender value of

the Fixed MVA contract, surrender of Fixed MVA annuities will have an insignificant impact on the liquidity requirements of Life Operations.

[4] GICs are subject to discontinuance provisions which allow the policyholders to terminate their contracts prior to scheduled maturity at the lesser of the book value or market

value. Generally, the market value adjustment reflects changes in interest rates and credit spreads. As a result, the market value adjustment feature in the GIC serves to

protect the Company from interest rate risks and limit Life Operations’ liquidity requirements in the event of a surrender.

[5] Surrenders of, or policy loans taken from, as applicable, these general account liabilities, which include the general account option for Life Operations' individual variable

annuities and the variable life contracts of the former Individual Life business, the general account option for annuities of the former Retirement Plans business and universal

life contracts sold by the former Individual Life business, may be funded through operating cash flows of Life Operations, available short-term investments, or Life

Operations may be required to sell fixed maturity investments to fund the surrender payment. Sales of fixed maturity investments could result in the recognition of realized

losses and insufficient proceeds to fully fund the surrender amount. In this circumstance, Life Operations may need to take other actions, including enforcing certain contract

provisions which could restrict surrenders and/or slow or defer payouts. The Company has ceded reinsurance in connection with the sales of its Retirement Plans and

Individual Life businesses in 2013 to MassMutual and Prudential, respectively.

122