The Hartford 2014 Annual Report Download - page 188

Download and view the complete annual report

Please find page 188 of the 2014 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

|

|

Table of Contents

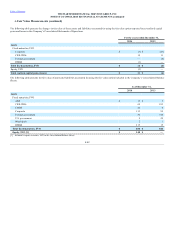

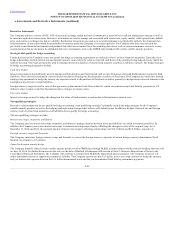

The Company utilizes a variety of OTC, OTC-cleared and exchange traded derivative instruments as a part of its overall risk management strategy as well as

to enter into replication transactions. Derivative instruments are used to manage risk associated with interest rate, equity market, credit spread, issuer default,

price, and currency exchange rate risk or volatility. Replication transactions are used as an economical means to synthetically replicate the characteristics

and performance of assets that would be permissible investments under the Company’s investment policies. The Company also may enter into and has

previously issued financial instruments and products that either are accounted for as free-standing derivatives, such as certain reinsurance contracts, or may

contain features that are deemed to be embedded derivative instruments, such as the GMWB rider included with certain variable annuity products.

Certain derivatives the Company enters into satisfy the hedge accounting requirements as outlined in Note 1 of these financial statements. Typically, these

hedge relationships include interest rate and foreign currency swaps where the terms or expected cash flows of the securities being hedged closely match the

terms of the swap. The swaps are typically used to manage interest rate duration of certain fixed maturity securities or liability contracts. The hedge strategies

by hedge accounting designation include:

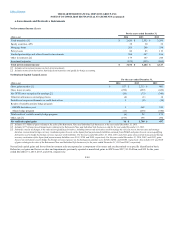

Cash flow hedges

Interest rate swaps are predominantly used to manage portfolio duration and better match cash receipts from assets with cash disbursements required to fund

liabilities. These derivatives primarily convert interest receipts on floating-rate fixed maturity securities to fixed rates. The Company also enters into forward

starting swap agreements to hedge the interest rate exposure related to the purchase of fixed-rate securities, primarily to hedge interest rate risk inherent in the

assumptions used to price certain liabilities.

Foreign currency swaps are used to convert foreign currency-denominated cash flows related to certain investment receipts and liability payments to U.S.

dollars in order to reduce cash flow fluctuations due to changes in currency rates.

Fair value hedges

Interest rate swaps are used to hedge the changes in fair value of fixed maturity securities due to fluctuations in interest rates.

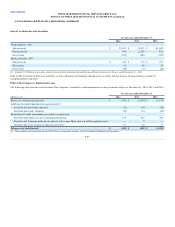

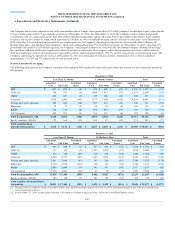

Derivative relationships that do not qualify for hedge accounting (“non-qualifying strategies”) primarily include the hedge program for the Company's

variable annuity products as well as the hedging and replication strategies that utilize credit default swaps. In addition, hedges of interest rate and foreign

currency risk of certain fixed maturities and liabilities do not qualify for hedge accounting.

The non-qualifying strategies include:

Interest rate swaps, swaptions, and futures

The Company may use interest rate swaps, swaptions, and futures to manage duration between assets and liabilities in certain investment portfolios. In

addition, the Company enters into interest rate swaps to terminate existing swaps, thereby offsetting the changes in value of the original swap. As of

December 31, 2014 and 2013, the notional amount of interest rate swaps in offsetting relationships was $13.1 billion and $6.9 billion, respectively.

Foreign currency swaps and forwards

The Company enters into foreign currency swaps and forwards to convert the foreign currency exposures of certain foreign currency-denominated fixed

maturity investments to U.S. dollars.

Japan fixed payout annuity hedge

The Company formerly offered certain variable annuity products with a GMIB rider through HLIKK, a former indirect wholly-owned subsidiary that was sold

on June 30, 2014. For further discussion on the sale, see the Sale of Hartford Life Insurance KK section in Note 2 - Business Dispositions of Notes to the

Consolidated Financial Statements. The Company will continue to reinsure from HLIKK the Japan fixed payout annuities. The Company invests in U.S.

dollar denominated assets to support the reinsurance liability. The Company entered into pay U.S. dollar, receive yen swap contracts to hedge the currency

and yen interest rate exposure between the U.S. dollar denominated assets and the yen denominated fixed liability reinsurance payments.

F-52