The Hartford 2014 Annual Report Download - page 115

Download and view the complete annual report

Please find page 115 of the 2014 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

|

|

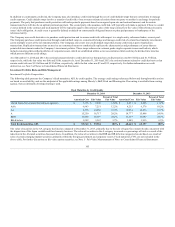

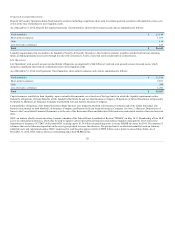

Other-Than-Temporary Impairments

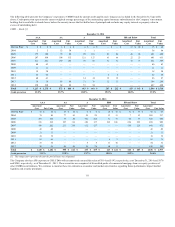

The following table presents the Company’s impairments recognized in earnings by security type excluding intent-to-sell impairment relating to the sales of

Retirement Plans and Individual Life businesses.

ABS $ — $ 9 $ 29

CRE CDOs — 2 10

CMBS

Bonds 2 17 24

IOs 1 4 3

Corporate 35 20 28

Equity 11 15 65

Municipal 3 — —

Agency 3 — —

RMBS Non-agency

RMBS Alt-A — — 1

Sub-prime 1 6 12

Other 3 — —

Total

[1] Excludes $177 of intent-to-sell impairments related to the sales of the Retirement Plans and Individual Life businesses.

Year ended December 31, 2014

For the year ended December 31, 2014, impairments recognized in earnings were comprised of credit impairments of $37, securities that the Company intends

to sell of $17, impairments on equity securities of $2, and other impairments of $3.

Impairments for the year ended December 31, 2014 were primarily credit impairments concentrated in corporate securities. The corporate securities were

impaired due to certain issuers that have experienced financial difficulty and either defaulted or are expected to default on contractually obligated principal

and interest payments. Also included in credit impairments for the year ended December 31, 2014, were private placements that were impaired due to declines

in expected cash flows related to the underlying referenced securities. The Company’s determination of expected future cash flows used to calculate the

credit loss amount is a quantitative and qualitative process. The Company incorporates its best estimate of future cash flows using internal assumptions and

judgments that are informed by economic and industry specific trends, as well as our expectation with respect to security specific developments. Credit

impairments for the year ended December 31, 2014 were primarily identified through security specific reviews and resulted from changes in the financial

condition and near term prospects of certain issuers. Other impairments for the year ended December 31, 2014 primarily related to certain equity, AFS

securities with debt-like characteristics that the Company intends to sell.

In addition to the credit impairments recognized in earnings, the Company recognized non-credit impairments in other comprehensive income of $5 for the

year ended December 31, 2014, predominantly concentrated in corporate securities and CMBS. These non-credit impairments represent the difference

between fair value and the Company’s best estimate of expected future cash flows discounted at the security’s effective yield prior to impairment, rather than

at current market implied credit spreads. These non-credit impairments primarily represent increases in market liquidity premiums and credit spread widening

that occurred after the securities were purchased, as well as a discount for variable-rate coupons which are paying less than at purchase date. In general, larger

liquidity premiums and wider credit spreads are the result of deterioration of the underlying collateral performance of the securities, as well as the risk

premium required to reflect future uncertainty in the real estate market.

Future impairments may develop as the result of changes in intent to sell specific securities or if actual results underperform current modeling assumptions,

which may be the result of, but are not limited to, macroeconomic factors and security-specific performance below current expectations. Ultimate loss

formation will be a function of macroeconomic factors and idiosyncratic security-specific performance.

115