The Hartford 2014 Annual Report Download - page 189

Download and view the complete annual report

Please find page 189 of the 2014 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

|

|

Table of Contents

Credit contracts

Credit default swaps are used to purchase credit protection on an individual entity or referenced index to economically hedge against default risk and credit-

related changes in value on fixed maturity securities. Credit default swaps are also used to assume credit risk related to an individual entity or referenced

index as a part of replication transactions. These contracts require the Company to pay or receive a periodic fee in exchange for compensation from the

counterparty should the referenced security issuers experience a credit event, as defined in the contract. The Company is also exposed to credit risk related to

credit derivatives embedded within certain fixed maturity securities which are comprised of structured securities that contain credit derivatives that reference

a standard index of corporate securities. In addition, the Company enters into credit default swaps to terminate existing credit default swaps, thereby

offsetting the changes in value of the original swap going forward.

Equity index swaps and options

Beginning in 2014, the Company entered into total return swaps to hedge equity risk of equity common stock investments which are accounted for using fair

value option in order to align the accounting treatment with net realized capital gains (losses). The Company also enters into equity index options with the

purpose of hedging the impact of an adverse equity market environment on the investment portfolio. In addition, the Company formerly offered certain

equity indexed products, a portion of which contain embedded derivatives that require bifurcation. The Company uses equity index swaps to economically

hedge the equity volatility risk associated with the equity indexed products.

GMWB derivatives, net

The Company formerly offered certain variable annuity products with GMWB riders. The GMWB product is a bifurcated embedded derivative (“GMWB

product derivatives”) that has a notional value equal to the GRB. The Company uses reinsurance contracts to transfer a portion of its risk of loss due to

GMWB. The reinsurance contracts covering GMWB (“GMWB reinsurance contracts”) are accounted for as free-standing derivatives with a notional amount

equal to the GRB amount.

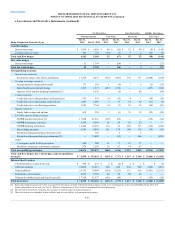

The Company utilizes derivatives (“GMWB hedging instruments”) as part of an actively managed program designed to hedge a portion of the capital market

risk exposures of the non-reinsured GMWB riders due to changes in interest rates, equity market levels, and equity volatility. These derivatives include

customized swaps, interest rate swaps and futures, and equity swaps, options and futures, on certain indices including the S&P 500 index, EAFE index and

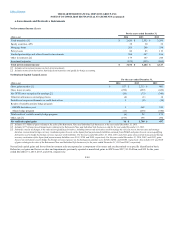

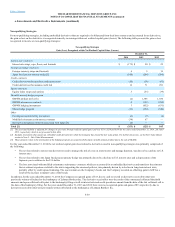

NASDAQ index. The following table presents notional and fair value for GMWB hedging instruments.

Customized swaps $ 7,041 $ 7,839

$ 124 $ 74

Equity swaps, options, and futures 3,761 4,237

39 44

Interest rate swaps and futures 3,640 6,615

11 (77)

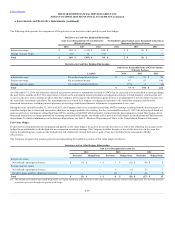

Macro hedge program

The Company utilizes equity options, swaps and foreign currency options to partially hedge against a decline in the equity markets and the resulting

statutory surplus and capital impact primarily arising from the guaranteed minimum death benefit ("GMDB") and GMWB obligations. The following table

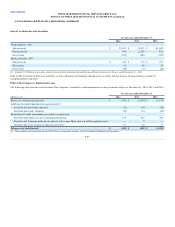

presents notional and fair value for the macro hedge program.

Equity options and swaps $ 5,983 $ 9,934

$ 141 $ 139

Foreign currency options 400 —

— —

Contingent capital facility put option

The Company entered into a put option agreement that provides the Company the right to require a third-party trust to purchase, at any time, The Hartford’s

junior subordinated notes in a maximum aggregate principal amount of $500. Under the put option agreement, The Hartford will pay premiums on a periodic

basis and will reimburse the trust for certain fees and ordinary expenses.

F-53