The Hartford 2014 Annual Report Download - page 172

Download and view the complete annual report

Please find page 172 of the 2014 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

|

|

Table of Contents

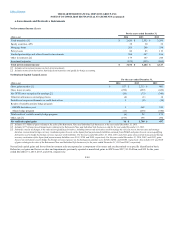

At each valuation date, the Company assumes expected returns based on:

• risk-free rates as represented by the Eurodollar futures, LIBOR deposits and swap rates to derive forward curve rates;

• market implied volatility assumptions for each underlying index based primarily on a blend of observed market “implied volatility” data;

• correlations of historical returns across underlying well known market indices based on actual observed returns over the ten years preceding the

valuation date; and

• three years of history for fund indexes compared to separate account fund regression.

On a daily basis, the Company updates capital market assumptions used in the GMWB liability model such as interest rates, equity indices and the blend of

implied equity index volatilities. The Company monitors various aspects of policyholder behavior and may modify certain of its assumptions, including

living benefit lapses and withdrawal rates, if credible emerging data indicates that changes are warranted. In addition, the Company will continue to evaluate

policyholder behavior assumptions as we begin to implement initiatives to reduce the size of the variable annuity business. At a minimum, all policyholder

behavior assumptions are reviewed and updated, as appropriate, in conjunction with the completion of the Company’s comprehensive study to refine its

estimate of future gross profits during the third quarter of each year.

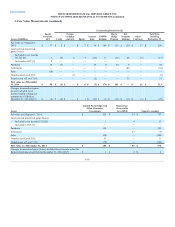

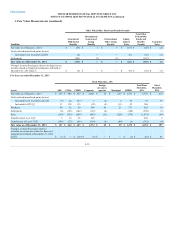

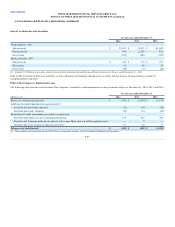

Credit Standing Adjustment

This assumption makes an adjustment that market participants would make, in determining fair value, to reflect the risk that guaranteed benefit obligations,

or the GMWB reinsurance recoverables will not be fulfilled. The Company incorporates a blend of observable Company and reinsurer credit default spreads

from capital markets, adjusted for market recoverability. The credit standing adjustment assumption, net of reinsurance, resulted in pre-tax realized gains

(losses) of $3, $(13) and $(69), for the years ended December 31, 2014, 2013 and 2012, respectively. As of December 31, 2014 and 2013, the credit standing

adjustment was $1 and $(1), respectively.

Margins

The behavior risk margin adds a margin that market participants would require, in determining fair value, for the risk that the Company’s assumptions about

policyholder behavior could differ from actual experience. The behavior risk margin is calculated by taking the difference between adverse policyholder

behavior assumptions and best estimate assumptions.

Assumption updates, including policyholder behavior assumptions, affected best estimates and margins for total pre-tax realized gains of $31, $75 and $274

for the years ended December 31, 2014, 2013 and 2012, respectively. As of December 31, 2014 and 2013, the behavior risk margin was $74 and $108,

respectively.

In addition to the non-market-based updates described above, the Company recognized non-market-based updates driven by the relative outperformance

(underperformance) of the underlying actively managed funds as compared to their respective indices resulting in pre-tax realized gains (losses) of

approximately $5, $33 and $106 for the years ended December 31, 2014, 2013 and 2012, respectively.

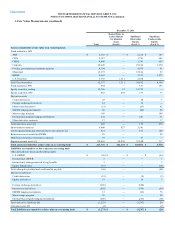

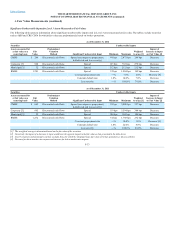

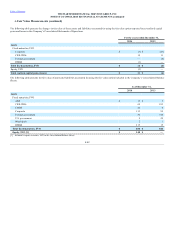

Significant unobservable inputs used in the fair value measurement of the GMWB embedded derivative and the GMWB reinsurance derivative are

withdrawal utilization and withdrawal rates, lapse rates, reset elections and equity volatility. The following table provides quantitative information about the

significant unobservable inputs and is applicable to all of the GMWB embedded derivative and the GMWB reinsurance derivative. Significant increases in

any of the significant unobservable inputs, in isolation, will generally have an increase or decrease correlation with the fair value measurement, as shown in

the table.

Withdrawal Utilization [2] 20% 100% Increase

Withdrawal Rates [3] —% 8% Increase

Lapse Rates [4] —% 75% Decrease

Reset Elections [5] 20% 75% Increase

Equity Volatility [6] 10% 40% Increase

[1] Conversely, the impact of a decrease in input would have the opposite impact to the fair value as that presented in the table.

[2] Range represents assumed cumulative percentages of policyholders taking withdrawals.

[3] Range represents assumed cumulative annual amount withdrawn by policyholders.

[4] Range represents assumed annual percentages of full surrender of the underlying variable annuity contracts across all policy durations for in force business.

[5] Range represents assumed cumulative percentages of policyholders that would elect to reset their guaranteed benefit base.

[6] Range represents implied market volatilities for equity indices based on multiple pricing sources.

F-36