The Hartford 2014 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2014 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

|

|

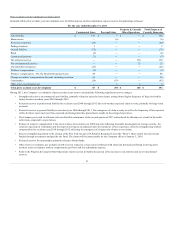

Current trends contributing to reserve uncertainty

The Hartford is a multi-line company in the property and casualty insurance business. The Hartford is therefore subject to reserve uncertainty stemming from

a number of conditions, including but not limited to those noted above, any of which could be material at any point in time. Certain issues may become more

or less important over time as conditions change. As various market conditions develop, management must assess whether those conditions constitute a long-

term trend that should result in a reserving action (i.e., increasing or decreasing the reserve).

Within Commercial Lines and Property & Casualty Other Operations, the Company has exposure to claims asserted for bodily injury as a result of long-term

or continuous exposure to harmful products or substances. Examples include, but are not limited to, pharmaceutical products, silica and lead paint. The

Company also has exposure to claims from construction defects, where property damage or bodily injury from negligent construction is alleged. In addition,

the Company has exposure to claims asserted against religious institutions and other organizations relating to molestation or abuse. Such exposures may

involve potentially long latency periods and may implicate coverage in multiple policy periods. These factors make reserves for such claims more uncertain

than other bodily injury or property damage claims. With regard to these exposures, the Company is monitoring trends in litigation, the external

environment, the similarities to other mass torts and the potential impact on the Company’s reserves.

In Personal Lines, reserving estimates are generally less variable than for the Company’s other property and casualty segments because of the coverages

having relatively shorter periods of loss emergence. Estimates, however, can still vary due to a number of factors, including interpretations of frequency and

severity trends and their impact on recorded reserve levels. Severity trends can be impacted by changes in internal claim handling and case reserving

practices in addition to changes in the external environment. These changes in claim practices increase the uncertainty in the interpretation of case reserve

data, which increases the uncertainty in recorded reserve levels. In addition, the introduction of new products and class plans has led to a different mix of

business by type of insured than the Company experienced in the past. Such changes in mix increase the uncertainty of the reserve projections, since

historical data and reporting patterns may not be applicable to the new business.

In standard commercial lines, workers’ compensation is the Company’s single biggest line of business and the line of business with the longest pattern of loss

emergence. Medical costs make up more than 50% of workers’ compensation payments. To the extent that payment patterns are impacted by increases or

decreases in the frequency of settlement payments, historical patterns would be less reliable, increasing the uncertainty around reserve estimates. As such,

reserve estimates for workers’ compensation are particularly sensitive to changes in medical inflation, the changing use of medical care procedures and

changes in state legislative and regulatory environments. In addition, a changing economic environment can affect the ability of an injured worker to return

to work and the length of time a worker receives disability benefits.

In specialty lines, many lines of insurance are “long-tail”, including large deductible workers’ compensation insurance; as such, reserve estimates for these

lines are more difficult to determine than reserve estimates for shorter-tail lines of insurance. Estimating required reserve levels for large deductible workers’

compensation insurance is further complicated by the uncertainty of whether losses that are attributable to the deductible amount will be paid by the insured;

if such losses are not paid by the insured due to financial difficulties, the Company would be contractually liable. Auto severity trends can be impacted by

changes in internal claim handling and case reserving practices in addition to changes in the external environment. These changes in claim practices increase

the uncertainty in the interpretation of case reserve data, which increases the uncertainty in recorded reserve levels. Another example of reserve variability

relates to reserves for directors’ and officers’ insurance. There is potential volatility in the required level of reserves due to the continued uncertainty

regarding the number and severity of class action suits. Additionally, the Company’s exposure to losses under directors’ and officers’ insurance policies is

primarily in excess layers, making estimates of loss more complex.

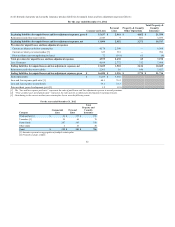

Impact of changes in key assumptions on reserve volatility

As stated above, the Company’s practice is to estimate reserves using a variety of methods, assumptions and data elements. Within its reserve estimation

process for reserves other than asbestos and environmental, the Company does not consistently use statistical loss distributions or confidence levels around

its reserve estimate and, as a result, does not disclose reserve ranges.

The reserve estimation process includes assumptions about a number of factors in the internal and external environment. Across most lines of business, the

most important assumptions are future loss development factors applied to paid or reported losses to date. The trend in loss costs is also a key assumption,

particularly in the most recent accident years, where loss development factors are less credible.

45