The Hartford 2014 Annual Report Download - page 215

Download and view the complete annual report

Please find page 215 of the 2014 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

205 -

206

206 -

207

207 -

208

208 -

209

209 -

210

210 -

211

211 -

212

212 -

213

213 -

214

214 -

215

215 -

216

216 -

217

217 -

218

218 -

219

219 -

220

220 -

221

221 -

222

222 -

223

223 -

224

224 -

225

225 -

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

-

277

-

278

-

279

-

280

-

281

-

282

-

283

-

284

-

285

-

286

-

287

-

288

-

289

-

290

-

291

-

292

-

293

-

294

-

295

-

296

|

|

Table of Contents

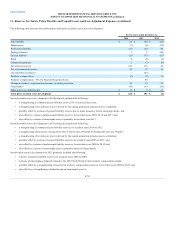

The Company continues to receive asbestos and environmental claims. Asbestos claims relate primarily to bodily injuries asserted by people who came in

contact with asbestos or products containing asbestos. Environmental claims relate primarily to pollution and related clean-up costs.

The Company wrote several different categories of insurance contracts that may cover asbestos and environmental claims. First, the Company wrote primary

policies providing the first layer of coverage in an insured’s liability program. Second, the Company wrote excess policies providing higher layers of

coverage for losses that exhaust the limits of underlying coverage. Third, the Company acted as a reinsurer assuming a portion of those risks assumed by

other insurers writing primary, excess and reinsurance coverages. Fourth, subsidiaries of the Company participated in the London Market, writing both direct

insurance and assumed reinsurance business.

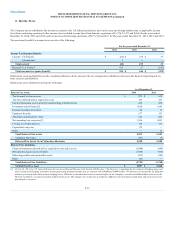

Significant uncertainty limits the ability of insurers and reinsurers to estimate the ultimate reserves necessary for unpaid losses and expenses related to

environmental and particularly asbestos claims. The degree of variability of reserve estimates for these exposures is significantly greater than for other more

traditional exposures.

In the case of the reserves for asbestos exposures, factors contributing to the high degree of uncertainty include inadequate loss development patterns,

plaintiffs’ expanding theories of liability, the risks inherent in major litigation, and inconsistent emerging legal doctrines. Furthermore, over time, insurers,

including the Company, have experienced significant changes in the rate at which asbestos claims are brought, the claims experience of particular insureds,

and the value of claims, making predictions of future exposure from past experience uncertain. Plaintiffs and insureds also have sought to use bankruptcy

proceedings, including “pre-packaged” bankruptcies, to accelerate and increase loss payments by insurers. In addition, some policyholders have asserted new

classes of claims for coverages to which an aggregate limit of liability may not apply. Further uncertainties include insolvencies of other carriers and

unanticipated developments pertaining to the Company’s ability to recover reinsurance for asbestos and environmental claims. Management believes these

issues are not likely to be resolved in the near future.

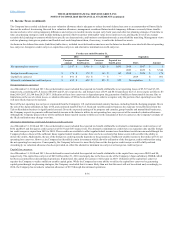

In the case of the reserves for environmental exposures, factors contributing to the high degree of uncertainty include expanding theories of liability and

damages, the risks inherent in major litigation, inconsistent decisions concerning the existence and scope of coverage for environmental claims, and

uncertainty as to the monetary amount being sought by the claimant from the insured.

The reporting pattern for assumed reinsurance claims, including those related to asbestos and environmental claims, is much longer than for direct claims. In

many instances, it takes months or years to determine that the policyholder’s own obligations have been met and how the reinsurance in question may apply

to such claims. The delay in reporting reinsurance claims and exposures adds to the uncertainty of estimating the related reserves.

It is also not possible to predict changes in the legal and legislative environment and their effect on the future development of asbestos and environmental

claims.

Given the factors described above, the Company believes the actuarial tools and other techniques it employs to estimate the ultimate cost of claims for more

traditional kinds of insurance exposure are less precise in estimating reserves for certain of its asbestos and environmental exposures. For this reason, the

Company principally relies on exposure-based analysis to estimate the ultimate costs of these claims and regularly evaluates new account information in

assessing its potential asbestos and environmental exposures. The Company supplements this exposure-based analysis with evaluations of the Company’s

historical direct net loss and expense paid and reported experience, and net loss and expense paid and reported experience by calendar and/or report year, to

assess any emerging trends, fluctuations or characteristics suggested by the aggregate paid and reported activity.

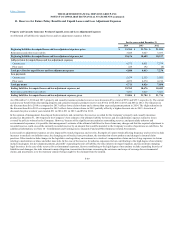

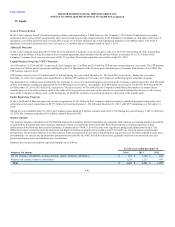

As of December 31, 2014 and 2013, the Company reported $1.7 billion of net asbestos reserves and $247 and $276 of net environmental reserves,

respectively. The Company believes that its current asbestos and environmental reserves are appropriate. However, analyses of future developments could

cause The Hartford to change its estimates and ranges of its asbestos and environmental reserves, and the effect of these changes could be material to the

Company’s consolidated operating results and liquidity.

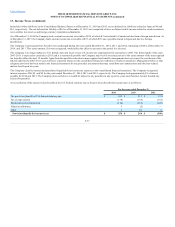

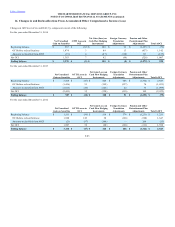

The total rental expense on operating leases was $62, $79, and $105 in 2014, 2013, and 2012, respectively, which excludes sublease rental income of $4, $8,

and $6 in 2014, 2013 and 2012, respectively.

F-79