Telus 2010 Annual Report Download - page 83

Download and view the complete annual report

Please find page 83 of the 2010 Telus annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

|

|

TELUS 2010 annual report . 79

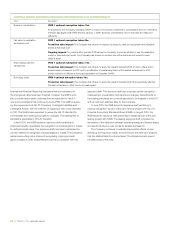

Effects of transition

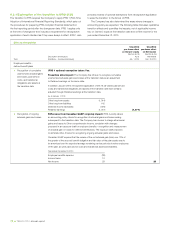

Topic

Unaudited Unaudited

pro forma effect pro forma effect

on Owners’ equity on Net income

(Section 8.2.2) (Section 8.2.3)

Description and impacts As at Year ended

($ millions – increase (decrease)) Jan. 1, 2010 Dec. 31, 2010

Impairment of assets Difference from Canadian GAAP: IFRS requires that increases in recoverable

amounts of impaired assets subsequent to the time of impairment be recognized

as an impairment reversal (except for goodwill), but only to the extent that the resulting

carrying amount would not exceed the carrying amount that would have existed had

an impairment amount not initially been recognized. Canadian GAAP did not allow

for increases in recoverable amounts of impaired assets subsequent to the time of

impairment to be recognized.

IFRS requires, given the Company’s facts and circumstances, that the Company’s

spectrum licences be assessed for impairment as a part of the Wireless cash-

generating unit. The result is that the $910 million impairment recorded by the

Company in 2002 would not have been required under IFRS. Previously, given the

Company’s facts and circumstances, the application of Canadian GAAP resulted

in the Company’s spectrum licences being assessed for impairment separately.

Transition date impact: In addition to impairment reversals, IFRS transitional

rules require the amortization cessation for intangible assets with indefinite lives to

be accounted for retrospectively with the result being the reversal of the amortization

previously recorded under Canadian GAAP. When Canadian GAAP introduced

impairment of assets for intangible assets with indefinite lives, it concurrently ceased

requiring their amortization on a prospective basis and thus $108 million of associated

amortization recorded to then by the Company was not reversed. The Company has

also recorded impairment reversals, net of accumulated depreciation of $91 million

at the transition date for certain property, plant and equipment impairments recorded

by predecessor companies.

As at January 1, 2010

Property, plant and equipment, net 91

Intangible assets, net (impairment reversal) 910

Intangible assets, net (amortization reversal) 108

Deferred income tax liability 281

Retained earnings 828 828

Ongoing impact: The transition date impairment reversal for property, plant and

equipment impairment recorded in predecessor companies results in a minor increase

in depreciation expense. Volatility in Net income could result from periodic impairment

tests, should the facts support a future impairment.

Year ended December 31, 2010

Depreciation 5

Income taxes (1)

Net income (4) (4)

Sale of accounts receivable Difference from Canadian GAAP: IFRS does not permit de-recognition of the

accounts receivable sold to an arm’s-length securitization trust, given the Company’s

facts and circumstances. IFRS considers the sale proceeds to be short-term

borrowings of the Company. Canadian GAAP de-recognized accounts receivable

sold to the arm’s-length securitization trust with which the Company transacts.

Transition date impact: Proceeds from the sale of accounts receivable under the

Company’s accounts receivable securitization agreement are recorded as short-term

borrowings, rather than a reduction of Accounts receivable (or de-recognition).

As at January 1, 2010

Accounts receivable 501

Short-term borrowings 500

Accounts payable and accrued liabilities (1)

Income and other taxes payable 1

Retained earnings 1 1

Ongoing impact: Accounts receivable securitization expenses of $8 million for the

year ended December 31, 2010, are included in Financing costs under IFRS, rather

than in Other expense under Canadian GAAP. –

MANAGEMENT’S DISCUSSION & ANALYSIS: 8