Telus 2010 Annual Report Download - page 132

Download and view the complete annual report

Please find page 132 of the 2010 Telus annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

|

|

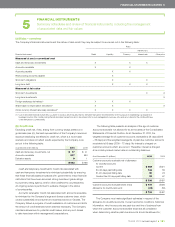

128 . TELUS 2010 annual report

believes that its financial policies and guidelines, which are reviewed

annually, are currently at the optimal level and, by maintaining credit

ratings in the range of BBB+ to A–, or the equivalent, provide reasonable

access to capital.

During 2010, the Company’s strategy, which was unchanged from

2009 (other than to change the dividend payout ratio guideline to 55–65%

of adjusted net earnings on a prospective basis), included maintain-

ing the financial policy set out in the following schedule. The Company

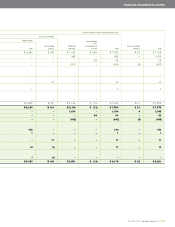

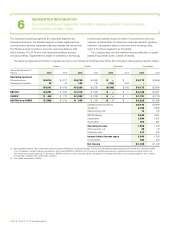

As at, or twelve-month periods ended, December 31 ($ in millions) Policy 2010 2009

Components of debt and coverage ratios

Net debt(1) $ß6,869 $ß7,312

EBITDA – excluding restructuring costs(2) $ß3,717 $ß3,681

Net interest cost(3) $ 510 $ 532

Debt ratio

Net debt to EBITDA – excluding restructuring costs 1.5–2.0 1.8 2.0

Coverage ratios

Earnings coverage (interest coverage on long-term debt)(4) 3.8 3.1

EBITDA – excluding restructuring costs interest coverage(5) 7.3 6.9

Other measures

Dividend payout ratio of adjusted net earnings(6) 65% 67%

Dividend payout ratio 65% 61%

(4) Earnings coverage (interest coverage on long-term debt) is defined as net income

before interest expense on long-term debt and income tax expense, divided by

interest expense on long-term debt (including losses recorded on the redemption

of long-term debt, if any).

(5) EBITDA – excluding restructuring costs interest coverage is defined as EBITDA

– excluding restructuring costs divided by net interest cost. This measure is

substantially the same as the coverage ratio covenant in the Company’s credit

facilities.

(6) Adjusted net earnings per Common Share and Non-Voting Share is calculated

as follows:

2010 2009

Net income attributable to Common Shares

and Non-Voting Shares $ 1,034 $ 998

Income tax-related adjustments (30) (165)

Loss on redemption of long-term debt,

net of income taxes 37 69

Impacts of share options with the net-cash

settlement feature, net of income taxes (7) 1

Adjusted net earnings $ 1,034 $ 903

Adjusted net earnings per Common Share

and Non-Voting Share – basic $ 3.23 $ß2.84

(1) Net debt is calculated as follows:

2010 2009

Long-term debt (Note 18) $ß6,056 $ß6,172

Debt issuance costs netted against long-term debt 28 30

Derivative liabilities, net 404 721

Accumulated other comprehensive income amounts

arising from financial instruments used to manage

interest rate and currency risks associated with

U.S. dollar denominated debt (excluding tax effects) (2) (70)

Cash and temporary investments, net (17) (41)

Cumulative proceeds from accounts receivable

securitization (Note 14) 400 500

Net debt $ß6,869 $ß7,312

(2) EBITDA – excluding restructuring costs is calculated as follows:

2010 2009

EBITDA (Note 6) $ 3,643 $ß3,491

Restructuring costs (Note 7) 74 190

EBITDA – excluding restructuring costs $ 3,717 $ß3,681

(3) Net interest cost is defined as financing costs before gains on redemption and

repayment of debt, calculated on a twelve-month trailing basis (losses recorded on

the redemption of long-term debt, if any, are included in net interest cost).

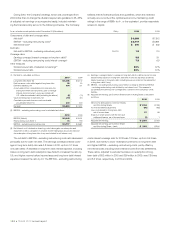

costs interest coverage ratio for 2010 was 7.3 times, up from 6.9 times

in 2009, due mainly to lower redemption premiums on long-term debt

and higher EBITDA – excluding restructuring costs, partly offset by

net interest costs including lower interest income from tax settlements.

These ratios, adjusted to exclude the losses on redemption of long-

term debt of $52 million in 2010 and $99 million in 2009, was 7.8 times

and 8.5 times, respectively, in 2010 and 2009.

The net debt to EBITDA – excluding restructuring costs ratio decreased

principally due to lower net debt. The earnings coverage (interest cover-

age on long-term debt) ratio was 3.8 times in 2010, up from 3.1 times

one year earlier. A decrease in long-term debt interest expense, including

losses on long-term debt redemption (see Note 8), increased the ratio by

0.6, and higher income before income taxes and long-term debt interest

expense increased the ratio by 0.1. The EBITDA – excluding restructuring