Telus 2010 Annual Report Download - page 58

Download and view the complete annual report

Please find page 58 of the 2010 Telus annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

|

|

54 . TELUS 2010 annual report

Reporting back on TELUS’ 2010 financing and capital structure management plan

Maintain position of fully hedging foreign exchange exposure for indebtedness

Maintained for the 8% U.S. dollar Notes due June 2011, the only foreign currency-denominated debt issue. The Company unwound the portion of its

cross currency interest rate swaps associated with the early partial redemption of 45% of these Notes outstanding at September 2, 2010 (see Section 7.3

Cash used by financing activities).

Preserve access to the capital markets at a reasonable cost by maintaining investment grade credit ratings in the range of BBB+

to A–, or the equivalent, in the future

At February 24, 2011, investment grade credit ratings from the four rating agencies that cover TELUS were in the desired range with a stable trend or outlook.

from the open market with no discount. Non-Voting Shares acquired

with optional cash payments at 100% of the average price under

the DRISP program will also change from treasury issuance to market

purchase, which will come into effect on March 1, 2011. The change

will result in increased cash outlays in respect of dividend payments.

While anticipated cash flow is expected to be more than sufficient

to meet current requirements and remain in compliance with TELUS’

financial policies, these intentions could constrain TELUS’ ability to invest

in its operations for future growth. As described in Section 1.5, payment

of net cash income taxes and funding of defined benefit pension plans

will reduce the after-tax cash flow otherwise available to return capital to

the Company’s shareholders. If actual results are different from TELUS’

expectations, there can be no assurance that TELUS will not need to

change its financing plans, or its intention to pay dividends according

to the target payout guideline. For the related risk discussion, see

Section 10.6 Financing and debt requirements.

4.4 Disclosure controls and procedures

and internal control over financial reporting

Disclosure controls and procedures

Disclosure controls and procedures are designed to provide reasonable

assurance that all relevant information is gathered and reported to senior

management, including the President and Chief Executive Officer (CEO)

and the Executive Vice-President and Chief Financial Officer (CFO),

on a timely basis so that appropriate decisions can be made regarding

public disclosure.

The CEO and the CFO have evaluated the effectiveness of the

Company’s disclosure controls and procedures related to the preparation

of the MD&A and the Consolidated financial statements. They have

concluded that the Company’s disclosure controls and procedures were

effective, at a reasonable assurance level, to ensure that material infor-

mation relating to the Company and its consolidated subsidiaries would

be made known to them by others within those entities, particularly

during the period in which the MD&A and the Consolidated financial

statements contained in this report were being prepared.

Internal control over financial reporting

Internal control over financial reporting is designed to provide reasonable

assurance regarding the reliability of financial reporting and the prepara-

tion of financial statements in accordance with Canadian GAAP and the

requirements of the Securities and Exchange Commission in the United

States, as applicable. TELUS’ CEO and CFO have assessed the effective-

ness of the Company’s internal control over financial reporting as at

December 31, 2010, in accordance with Internal Control – Integrated

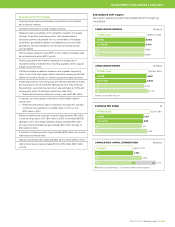

TELUS’ 2011 financing and capital structure

management plan

At December 31, 2010, TELUS had access to undrawn credit facilities

of more than $1.8 billion and availability of $100 million under its accounts

receivable securitization program. At December 31, 2010, the Company

had access to a shelf prospectus pursuant to which it can issue up

to $2 billion of debt and equity. TELUS believes that its investment grade

credit ratings provide reasonable access to capital markets to facilitate

future debt issuance.

The Company’s long-term debt principal maturities are illustrated

in the adjacent chart, including maturity of its 8% U.S. dollar Notes in

June 2011. TELUS expects to maintain its current position of fully hedging

its foreign exchange exposure for indebtedness on the U.S. dollar debt.

TELUS may issue additional long-term debt to refinance the 8% U.S. dol-

lar Notes, although the Company has sufficient unutilized credit facilities

to refinance this debt without accessing the long-term debt markets.

At the end of 2010, 93% of TELUS’ total debt was on a fixed-rate

basis and the weighted average term to maturity was approximately

5.7 years, up from 5.0 years at the end of 2009.

LONG-TERM DEBT PRINCIPAL MATURITIES

AS AT DECEMBER 31, 2010 ($ millions)

Maturities in 2011 include the derivative liability associated with U.S. dollar Notes,

at exchange rates in effect on December 31, 2010.

1,142

700

625

404

300

2025

2024

2023

2022

2021

2020

2019

2018

2017

2016

2015

2013

2014

2012

2011

700

1,000

1,000

175

249

200

TELUS expects to generate free cash flow in 2011, which would

be available to, among other things, pay dividends to holders of Common

Shares and Non-Voting Shares. Effective March 1, 2011, TELUS will

change its current practice of issuing shares from treasury at a 3%

discount for reinvested dividends under the dividend reinvestment and

share purchase (DRISP) program and switch back to purchasing shares