Telus 2010 Annual Report Download - page 154

Download and view the complete annual report

Please find page 154 of the 2010 Telus annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

|

|

150 . TELUS 2010 annual report

The best estimates of fiscal 2011 employer contributions to the

Company’s defined benefit plans are approximately $298 million (including

a discretionary contribution of $200 million made in January 2011) for

defined benefit pension plans and $NIL for other defined benefit plans.

These estimates (other than for the non-recurring contribution of $200 mil-

lion made in January 2011) are based upon the mid-year 2010 annual

funding reports that were prepared by actuaries using December 31, 2009,

actuarial valuations. The funding reports are based on the pension

plans’ fiscal years, which are calendar years. The next annual funding

valuations are expected to be prepared mid-year 2011.

(k) Assumptions

Management is required to make significant estimates about certain

actuarial and economic assumptions to be used in determining defined

benefit pension costs, accrued benefit obligations and pension plan

assets. These significant estimates are of a long-term nature, which is

consistent with the nature of employee future benefits.

The discount rate, which is used to determine the accrued benefit

obligation, is based on the yield on long-term, high-quality fixed term

investments, and is set annually. The expected long-term rate of return

is based upon forecasted returns of the major asset categories and

weighted by the plans’ target asset allocations. Future increases

in compensation are based upon the current benefits policies and

economic forecasts.

(j) Employer contributions

The determination of the minimum funding amounts for substantially

all of the Company’s registered defined benefit pension plans is governed

by the Pension Benefits Standards Act, 1985, which requires that, in

addition to current service costs being funded, both going-concern and

solvency valuations be performed on a specified periodic basis.

.Any excess of plan assets over plan liabilities determined in the

going-concern valuation reduces the Company’s minimum funding

requirement of current service costs, but may not reduce the

requirement to an amount less than the employees’ contributions.

The going-concern valuation generally determines the excess

(if any) of a plan’s assets over its liabilities, determined on a projected

benefit basis.

.As of the date of these consolidated financial statements, the

solvency valuation generally requires that a plan’s liabilities, deter-

mined on the basis that the plan is terminated on the valuation

date, in excess of its assets (if any) be funded, at a minimum,

in equal annual amounts over a period not exceeding five years.

In the latter half of 2009, the Canadian Federal Government

announced proposals that would, among other things, affect the

solvency funding methodology for pension plans governed by

the Pension Benefits Standards Act, 1985; the impact of these

proposals, if any, on the Company will depend upon the final

enacted form of the proposals.

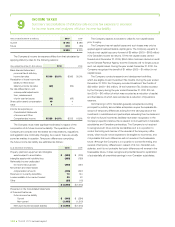

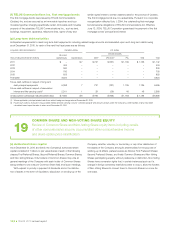

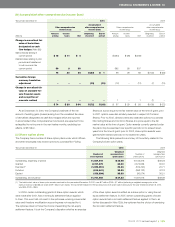

The significant weighted average actuarial assumptions arising from these estimates and adopted in measuring the Company’s accrued benefit

obligations are as follows:

Pension benefit plans Other benefit plans

2010 2009 2010 2009

Discount rate used to determine:

Net benefit costs for the year ended December 31 5.85% 7.25% 5.67% 7.11%

Accrued benefit obligation as at December 31 5.25% 5.85% 4.97% 5.65%

Expected long-term rate of return(1) on plan assets used to determine:

Net benefit costs for the year ended December 31 7.25% 7.25% 2.50% 3.00%

Accrued benefit obligation as at December 31 7.00% 7.25% 2.50% 2.50%

Rate of future increases in compensation used to determine:

Net benefit costs for the year ended December 31 3.00% 3.00% – –

Accrued benefit obligation as at December 31 3.00% 3.00% – –

(1) The expected long-term rate of return is based upon forecasted returns of the major asset categories and weighted by the plans’ target asset allocations (see (g)). Forecasted returns

arise from the Company’s ongoing review of trends, economic conditions, data provided by actuaries and updating of underlying historical information.

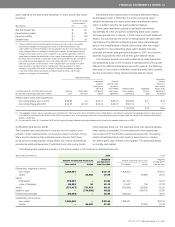

2010 sensitivity of key assumptions (year ended, or as at, December 31, 2010) Pension benefit plans Other benefit plans

Change in Change in Change in Change in

(millions) obligation expense obligation expense

Impact of hypothetical 25 basis point decrease(1) in:

Discount rate $ß219 $ß20 $ß1 $ß–

Expected long-term rate of return on plan assets $ß16 $ß–

Rate of future increases in compensation $ß 26 $ß 5 $ß– $ß–

(1) These sensitivities are hypothetical and should be used with caution. Favourable hypothetical changes in the assumptions result in decreased amounts, and unfavourable hypothetical

changes in the assumptions result in increased amounts, of the obligations and expenses. Changes in amounts based on a 25 basis point variation in assumptions generally cannot

be extrapolated because the relationship of the change in assumption to the change in amounts may not be linear. Also, in this table, the effect of a variation in a particular assumption

on the change in obligation or change in expense is calculated without changing any other assumption; in reality, changes in one factor may result in changes in another (for example,

increases in discount rates may result in increased expectations about the long-term rate of return on plan assets), which might magnify or counteract the sensitivities.