Telus 2010 Annual Report Download - page 78

Download and view the complete annual report

Please find page 78 of the 2010 Telus annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

|

|

74 . TELUS 2010 annual report

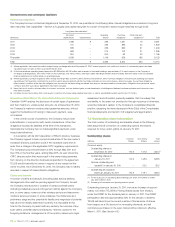

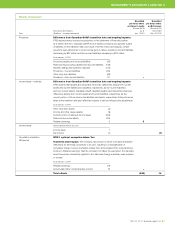

.After changeover to IFRS on January 1, 2011, described and illustrated in Section 8.2, the Company’s critical accounting estimates affect line items

on the Consolidated statements of income and other comprehensive income items, and line items on the Consolidated statements of financial

position, as follows:

Consolidated statements of income and other comprehensive income (IFRS-IASB)

Other

comprehensive

Operating expenses

income (Item never

Goods and Employee Amortization subsequently

Consolidated statements of Operating services benefits of intangible reclassified

financial position (IFRS-IASB) revenues purchased expense Depreciation assets to income)

Accounts receivable X

Short-term borrowings (securitized accounts receivable) X

Inventories X

Property, plant and equipment, net X

Intangible assets, net, and Goodwill, net(1) X

Investments X

Price cap deferral account

Advance billings and customer deposits X

Provisions (non-current liabilities) X

Employee defined benefit pension plans X X(2) X(2) X

(1) Accounting estimate, as applicable to intangible assets with indefinite lives and goodwill, primarily affects the Company’s wireless cash generating unit.

(2) Accounting estimate impact due to internal labour capitalization rates.

Accounts receivable

General

.The Company considers the business area that gave rise to the

accounts receivable, performs statistical analysis of portfolio delin-

quency trends and performs specific account identification when

determining its allowance for doubtful accounts. This information is

also used in conjunction with current market-based rates of borrowing

to determine the fair value of its residual cash flows arising from

accounts receivable securitization. The fair value of the Company’s

residual cash flows arising from the accounts receivable securitization

is also referred to as its retained interest. As described further in

Section 8.2.1, proceeds from the sale of accounts receivable are

recorded as Short-term borrowings under IFRS-IASB, rather than

a reduction of Accounts receivable (or de-recognition) under

Canadian GAAP.

.Assumptions underlying the allowance for doubtful accounts include

portfolio delinquency trends and specific account assessments

made when performing specific account identification. Assumptions

underlying the determination of the fair value of residual cash

flows arising from accounts receivable securitization include those

developed when determining the allowance for doubtful accounts

as well as the effective annual discount rate.

.These accounting estimates are in respect of the Accounts

receivable line item on the Company’s Consolidated statements

of financial position comprising approximately 5% of Total assets

as at December 31, 2010 (4% as at December 31, 2009). Based

on unaudited pro forma IFRS-IASB financial information, Accounts

receivable are approximately 7% of Total assets at December 31,

2010 (approximately 6% at January 1, 2010). If the future were to

adversely differ from management’s best estimates of the fair value

of the residual cash flows and the allowance for doubtful accounts,

the Company could experience a bad debt charge in the future.

Such a bad debt charge does not result in a cash outflow.

Key economic assumptions used to determine the

fair value of residual cash flows arising from accounts

receivable securitization

.The estimate of the Company’s fair value of its retained interest

could materially change from period to period due to the

fair value estimate being a function of the amount of accounts

receivable sold, which can vary on a monthly basis. See Note 14

of the Consolidated financial statements for further analysis.

The allowance for doubtful accounts

.The estimate of the Company’s allowance for doubtful accounts

could materially change from period to period due to the

allowance being a function of the balance and composition of

accounts receivable, which can vary on a month-to-month basis.

The variance in the balance of accounts receivable can arise

from a variance in the amount and composition of operating

revenues, from a variance in the amount of accounts receivable

sold to the securitization trust and from variances in accounts

receivable collection performance.

Inventories

The allowance for inventory obsolescence

.The Company determines its allowance for inventory obsolescence

based upon expected inventory turnover, inventory aging, and current

and future expectations with respect to product offerings.

.Assumptions underlying the allowance for inventory obsolescence

include future sales trends and offerings and the expected inventory

requirements and inventory composition necessary to support

these future sales offerings. The estimate of the Company’s allow-

ance for inventory obsolescence could materially change from

period to period due to changes in product offerings and consumer

acceptance of those products.