Duke Energy 2015 Annual Report Download - page 71

Download and view the complete annual report

Please find page 71 of the 2015 Duke Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

|

|

51

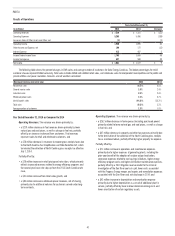

PART II

The majority of Duke Energy’s business is in environments that are either

fully or partially rate-regulated. In such environments, revenue requirements

are adjusted periodically by regulators based on factors including levels of

costs, sales volumes and costs of capital. Accordingly, Duke Energy’s regulated

utilities operate to some degree with a buffer from the direct effects, positive

or negative, of significant swings in market or economic conditions. However,

significant changes in discount rates over a prolonged period may have a

material impact on the fair value of equity.

As of August 31, 2015, all of the reporting units’ estimated fair value of

equity substantially exceeded the carrying value of equity.

For further information, see Note 11 to the Consolidated Financial

Statements, “Goodwill and Intangible Assets.”

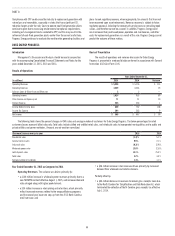

Long-Lived Asset Impairment Assessments, Excluding Regulated Operations

Property, plant and equipment, excluding plant held for sale, is stated

at the lower of carrying value (historical cost less accumulated depreciation

and previously recorded impairments) or fair value, if impaired. Duke Energy

evaluates property, plant and equipment for impairment when events or changes

in circumstances (such as a significant change in cash flow projections, the

determination that it is more likely than not an asset or asset group will be

sold) indicate the carrying value of such assets may not be recoverable. The

determination of whether an impairment has occurred is based on an estimate

of undiscounted future cash flows attributable to the assets, as compared with

their carrying value.

Performing an impairment evaluation involves a significant degree of

estimation and judgment in areas such as identifying circumstances that

indicate an impairment may exist, identifying and grouping affected assets, and

developing the undiscounted future cash flows. If an impairment has occurred,

the amount of the impairment recognized is determined by estimating the fair

value and recording a loss if the carrying value is greater than the fair value.

Additionally, determining fair value requires probability weighting future cash

flows to reflect expectations about possible variations in their amounts or

timing and the selection of an appropriate discount rate. Although cash flow

estimates are based on relevant information available at the time the estimates

are made, estimates of future cash flows are, by nature, highly uncertain and

may vary significantly from actual results. For assets identified as held for

sale, the carrying value is compared to the estimated fair value less cost to sell

to determine if an impairment loss is required. Until the assets are disposed

of, their estimated fair value is re-evaluated when circumstances or events

change.

When determining whether an asset or asset group has been impaired,

management groups assets at the lowest level that has discrete cash flows.

For further information, see Note 2 to the Consolidated Financial

Statements, “Acquisition and Dispositions.”

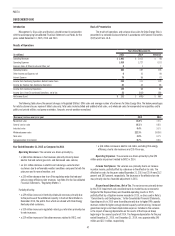

Accounting for Loss Contingencies

Preparation of financial statements and related disclosures require

judgments regarding the future outcome of contingent events. Duke Energy is

involved in certain legal and environmental matters arising in the normal course

of business. Estimating probable losses requires analysis of multiple forecasts

and scenarios that often depend on judgments about potential actions by third

parties, such as federal, state and local courts and regulators. Contingent

liabilities are often resolved over long periods of time. Amounts recorded in the

consolidated financial statements may differ from the actual outcome once the

contingency is resolved, which could have a material impact on future results of

operations, financial position and cash flows of Duke Energy.

For further information, see Notes 4 and 5 to the Consolidated Financial

Statements, “Regulatory Matters” and “Commitments and Contingencies.”

Revenue Recognition

Revenues on sales of electricity and gas are recognized when either the

service is provided or the product is delivered. Operating revenues include

unbilled electric and gas revenues earned when service has been delivered

but not billed by the end of the accounting period. Unbilled retail revenues

are estimated by applying an average revenue per kilowatt-hour (kWh) or per

thousand cubic feet (Mcf) for all customer classes to the number of estimated

kWh or Mcf delivered but not billed. Unbilled wholesale energy revenues are

calculated by applying the contractual rate per MWh to the number of estimated

MWh delivered but not yet billed. Unbilled wholesale demand revenues are

calculated by applying the contractual rate per MW to the MW volume delivered

but not yet billed. The amount of unbilled revenues can vary significantly from

period to period as a result of numerous factors, including seasonality, weather,

customer usage patterns, customer mix, timing of rendering customer bills, and

the average price in effect for customer classes.

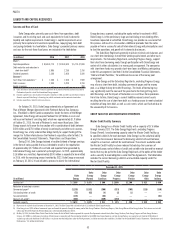

Pension and Other Post-Retirement Benefits

The calculation of pension expense, other post-retirement benefit expense

and net pension and other post-retirement assets or liabilities require the use

of assumptions and election of permissible accounting alternatives. Changes

in assumptions can result in different expense and reported asset or liability

amounts, and future actual experience can differ from the assumptions. Duke

Energy believes the most critical assumptions for pension and other post-

retirement benefits are the expected long-term rate of return on plan assets and

the assumed discount rate applied to future benefit payments. Additionally, the

health care cost trend rate assumption is critical to Duke Energy’s estimate of

other post-retirement benefits.

Duke Energy elects to amortize net actuarial gains or losses in excess

of the corridor of 10 percent of the greater of the market-related value of plan

assets or plan projected benefit obligation, into net pension or other post-

retirement benefit expense over the average remaining service period of active

covered employees. Prior service cost or credit, which represents the effect

on plan liabilities due to plan amendments, is amortized over the average

remaining service period of active covered employees.

Duke Energy maintains non-contributory defined benefit retirement

plans. The plans cover most U.S. employees using a cash balance formula.

Under a cash balance formula, a plan participant accumulates a retirement

benefit consisting of pay credits based upon a percentage of current eligible

earnings based on age and years of service and current interest credits. Certain

employees are covered under plans that use a final average earnings formula.

As of January 1, 2014, the qualified and non-qualified non-contributory defined

benefit plans are closed to new and rehired non-union, and certain unionized

employees.

Duke Energy provides some health care and life insurance benefits

for retired employees on a contributory and non-contributory basis. Certain

employees are eligible for these benefits if they have met age and service

requirements at retirement, as defined in the plans.

As of December 31, 2015, Duke Energy assumes pension and other post-

retirement plan assets will generate a long-term rate of return of 6.50 percent.

The expected long-term rate of return was developed using a weighted average

calculation of expected returns based primarily on future expected returns across

asset classes considering the use of active asset managers, where applicable.

Equity securities are held for their higher expected returns. Debt securities