Duke Energy 2015 Annual Report Download - page 196

Download and view the complete annual report

Please find page 196 of the 2015 Duke Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

186 -

187

187 -

188

188 -

189

189 -

190

190 -

191

191 -

192

192 -

193

193 -

194

194 -

195

195 -

196

196 -

197

197 -

198

198 -

199

199 -

200

200 -

201

201 -

202

202 -

203

203 -

204

204 -

205

205 -

206

206 -

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

|

|

176

PART II

DUKE ENERGY CORPORATION • DUKE ENERGY CAROLINAS, LLC • PROGRESS ENERGY, INC. •

DUKE ENERGY PROGRESS, LLC. • DUKE ENERGY FLORIDA, LLC. • DUKE ENERGY OHIO, INC. • DUKE ENERGY INDIANA, INC.

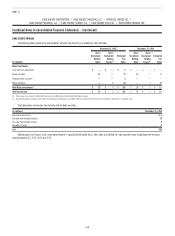

Combined Notes to Consolidated Financial Statements – (Continued)

OTHER FAIR VALUE DISCLOSURES

The fair value and book value of long-term debt, including current maturities, is summarized in the following table. Estimates determined are not necessarily

indicative of amounts that could have been settled in current markets. Fair value of long-term debt uses Level 2 measurements.

December 31, 2015 December 31, 2014

(in millions) Book Value Fair Value Book Value Fair Value

Duke Energy $ 39,569 $42,537 $39,868 $44,566

Duke Energy Carolinas 8,367 9,156 8,353 9,626

Progress Energy 14,464 15,856 14,668 16,951

Duke Energy Progress 6,518 6,757 6,170 6,696

Duke Energy Florida 4,266 4,908 4,823 5,767

Duke Energy Ohio 1,598 1,724 1,760 1,970

Duke Energy Indiana 3,768 4,219 3,769 4,456

At both December 31, 2015 and December 31, 2014, fair value of cash and cash equivalents, accounts and notes receivable, accounts payable, notes payable

and commercial paper, and non-recourse notes payable of variable interest entities are not materially different from their carrying amounts because of the short-term

nature of these instruments and/or because the stated rates approximate market rates.

17. VARIABLE INTEREST ENTITIES

A VIE is an entity that is evaluated for consolidation using more than

a simple analysis of voting control. The analysis to determine whether an

entity is a VIE considers contracts with an entity, credit support for an entity,

the adequacy of the equity investment of an entity and the relationship of

voting power to the amount of equity invested in an entity. This analysis is

performed either upon the creation of a legal entity or upon the occurrence of

an event requiring reevaluation, such as a significant change in an entity’s

assets or activities. A qualitative analysis of control determines the party that

consolidates a VIE. This assessment is based on (i) what party has the power

to direct the most significant activities of the VIE that impact its economic

performance and (ii) what party has rights to receive benefits or is obligated

to absorb losses that are significant to the VIE. The analysis of the party that

consolidates a VIE is a continual reassessment.

No financial support was provided to any of the consolidated VIEs during

the years ended December 31, 2015, 2014 and 2013, or is expected to be

provided in the future, that was not previously contractually required.