Duke Energy 2015 Annual Report Download - page 40

Download and view the complete annual report

Please find page 40 of the 2015 Duke Energy annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

|

|

PART I

20

industry. The availability of credit under Duke Energy’s Master Credit Facility

depends upon the ability of the banks providing commitments under the facility

to provide funds when their obligations to do so arise. Systematic risk of the

banking system and the financial markets could prevent a bank from meeting its

obligations under the facility agreement.

Duke Energy maintains a revolving credit facility to provide backup for its

commercial paper program and letters of credit to support variable rate demand

tax-exempt bonds that may be put to the Duke Energy Registrant issuer at

the option of the holder. The facility includes borrowing sublimits for the Duke

Energy Registrants, each of whom is a party to the credit facility, and financial

covenants that limit the amount of debt that can be outstanding as a percentage

of the total capital for the specific entity. Failure to maintain these covenants at

a particular entity could preclude Duke Energy from issuing commercial paper or

the Duke Energy Registrants from issuing letters of credit or borrowing under the

Master Credit Facility.

The Duke Energy Registrants must meet credit quality standards and

there is no assurance they will maintain investment grade credit ratings.

If the Duke Energy Registrants are unable to maintain investment grade

credit ratings, they would be required under credit agreements to provide

collateral in the form of letters of credit or cash, which may materially

adversely affect their liquidity.

Each of the Duke Energy Registrants’ senior long-term debt issuances is

currently rated investment grade by various rating agencies. The Duke Energy

Registrants cannot ensure their senior long-term debt will be rated investment

grade in the future.

If the rating agencies were to rate the Duke Energy Registrants below

investment grade, borrowing costs would increase, perhaps significantly.

In addition, the potential pool of investors and funding sources would likely

decrease. Further, if the short-term debt rating were to fall, access to the

commercial paper market could be significantly limited.

A downgrade below investment grade could also require the posting of

additional collateral in the form of letters of credit or cash under various credit,

commodity and capacity agreements and trigger termination clauses in some

interest rate derivative agreements, which would require cash payments. All

of these events would likely reduce the Duke Energy Registrants’ liquidity and

profitability and could have a material effect on their financial position, results

of operations or cash flows.

Non-compliance with debt covenants or conditions could adversely affect

the Duke Energy Registrants’ ability to execute future borrowings.

The Duke Energy Registrants’ debt and credit agreements contain

various financial and other covenants. Failure to meet those covenants

beyond applicable grace periods could result in accelerated due dates and/or

termination of the agreements.

Market performance and other changes may decrease the value of the

NDTF investments of Duke Energy Carolinas, Duke Energy Progress and

Duke Energy Florida, which then could require significant additional

funding.

Ownership and operation of nuclear generation facilities also requires the

maintenance of funded trusts that are intended to pay for the decommissioning

costs of the respective nuclear power plants. The performance of the capital

markets affects the values of the assets held in trust to satisfy these future

obligations. Duke Energy Carolinas, Duke Energy Progress and Duke Energy Florida

have significant obligations in this area and hold significant assets in these trusts.

These assets are subject to market fluctuations and will yield uncertain returns,

which may fall below projected rates of return. Although a number of factors

impact funding requirements, a decline in the market value of the assets may

increase the funding requirements of the obligations for decommissioning nuclear

plants. If Duke Energy Carolinas, Duke Energy Progress and Duke Energy Florida

are unable to successfully manage their NDTF assets, their financial condition,

results of operations and cash flows could be negatively affected.

Poor investment performance of the Duke Energy pension plan holdings

and other factors impacting pension plan costs could unfavorably impact

the Duke Energy Registrants’ liquidity and results of operations.

The costs of providing non-contributory defined benefit pension plans

are dependent upon a number of factors, such as the rates of return on plan

assets, discount rates, the level of interest rates used to measure the required

minimum funding levels of the plans, future government regulation and required

or voluntary contributions made to the plans. The Subsidiary Registrants

are allocated their proportionate share of the cost and obligations related to

these plans. Without sustained growth in the pension investments over time

to increase the value of plan assets and, depending upon the other factors

impacting costs as listed above, Duke Energy could be required to fund its

plans with significant amounts of cash. Such cash funding obligations, and the

Subsidiary Registrants’ proportionate share of such cash funding obligations,

could have a material impact on the Duke Energy Registrants’ financial position,

results of operations or cash flows.

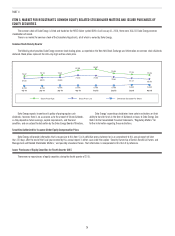

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.