SunTrust 2015 Annual Report Download - page 91

Download and view the complete annual report

Please find page 91 of the 2015 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

|

|

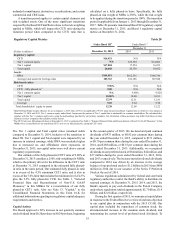

63

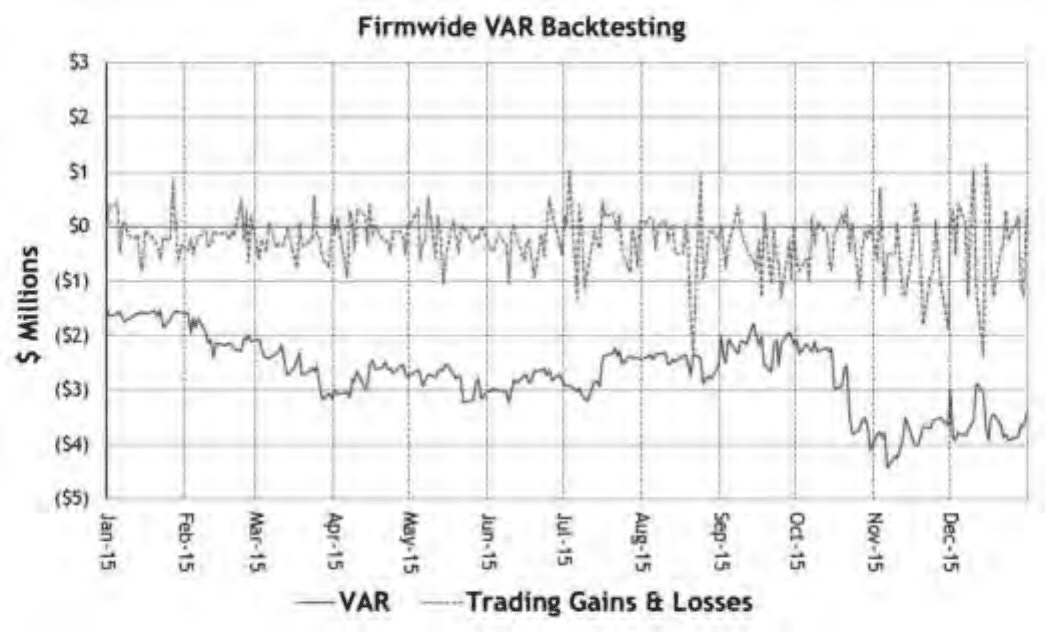

We have valuation policies, procedures, and methodologies for

all covered positions. Additionally, trading positions are reported

in accordance with U.S. GAAP and are subject to independent

price verification. See Note 17, "Derivative Financial

Instruments" and Note 18, "Fair Value Election and

Measurement" to the Consolidated Financial Statements in this

Form 10-K, as well as the "Critical Accounting Policies" section

of this MD&A for discussion of valuation policies, procedures,

and methodologies.

Model risk management: Our approach for validating and

evaluating the accuracy of internal and vended models and

associated processes includes developmental and

implementation testing and ongoing monitoring and

maintenance performed by the various model developers in

conjunction with model owners. The MRMG is responsible for

the independent model validation for the VAR and Stressed VAR

models. The validation typically includes evaluation of all model

documentation, as well as model monitoring and maintenance

plans. In addition, the MRMG performs its own testing. Due to

ongoing developments in financial markets, evolution in

modeling approaches, and for purposes of model enhancement,

we assess the performance of all VAR models regularly through

the model monitoring and maintenance process.

Stress testing: We use a comprehensive range of stress testing

techniques to help monitor risks across trading desks and to

augment standard daily VAR and other risk limits reporting. The

stress testing framework is designed to quantify the impact of

extreme but plausible stress scenarios that could lead to large

unexpected losses. Our stress tests include historical repeats and

simulations using hypothetical risk factor shocks. All trading

positions within each applicable market risk category (interest

rate risk, equity risk, foreign exchange rate risk, credit spread

risk, and commodity price risk) are included in our

comprehensive stress testing framework. We review stress

testing scenarios on an ongoing basis and make updates as

necessary to ensure that both current and potential emerging risks

are captured appropriately.

Trading portfolio capital adequacy: We assess capital adequacy

on a regular basis, based on estimates of our risk profile and

capital positions under baseline and stressed scenarios. Scenarios

consider material risks, including credit risk, market risk, and

operational risk. Our assessment of capital adequacy arising from

market risk also includes a review of risk arising from material

portfolios of covered positions. See the “Capital Resources”

section in this MD&A for additional discussion of capital

adequacy.

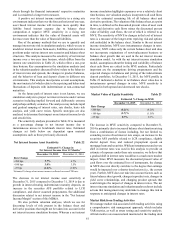

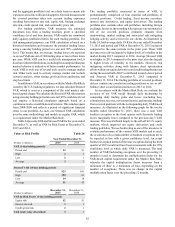

Liquidity Risk Management

Liquidity risk is the risk of being unable, at a reasonable cost, to

meet financial obligations as they come due. We manage

liquidity risk utilizing three lines of defense as described below.

These lines of defense are designed to mitigate our three primary

liquidity risks: structural (“mismatch”) liquidity risk, market

liquidity risk, and contingent liquidity risk. Structural liquidity

risk arises from our maturity transformation activities and

balance sheet structure, which may create mismatches in the

timing of cash inflows and outflows. Market liquidity risk, which

we also describe as refinancing or refunding risk, constitutes the

risk that we could lose access to the financial markets or the cost