SunTrust 2015 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2015 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

|

|

46

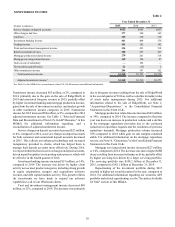

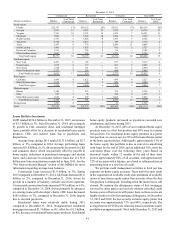

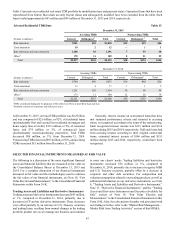

Nonperforming Loans

NPLs at December 31, 2015 totaled $672 million, a $38 million,

or 6% increase from December 31, 2014. Commercial NPLs

increased $146 million, or 84%, due largely to downgrades of

certain energy-related loans. While certain of these loans may

be current with respect to their contractual debt service

agreements, the recent decline in oil prices and projected

slowdown in global economic growth, combined with facts and

circumstances associated with these specific loan arrangements,

raised uncertainty regarding the full collectability of principal.

Therefore, we prudently stopped accruing interest on these loans

in the fourth quarter of 2015 and classified the loans as NPLs.

See the "Critical Accounting Policies" section of this Form 10-

K for additional information regarding our policy on loans

classified as nonaccrual. See the "Loans" section of this MD&A

for additional information regarding our energy-related loan

exposure. Residential NPLs declined $111 million, or 24%, due

largely to the sale of $122 million in nonperforming mortgages

during 2015.

Interest income on consumer and residential nonaccrual

loans, if recognized, is recognized on a cash basis. Interest

income on commercial nonaccrual loans is not generally

recognized until after the principal amount has been reduced to

zero. We recognized $22 million of interest income related to

nonaccrual loans during both 2015 and 2014. If all such loans

had been accruing interest according to their original contractual

terms, estimated interest income of $28 million and $47 million

would have been recognized in 2015 and 2014, respectively.

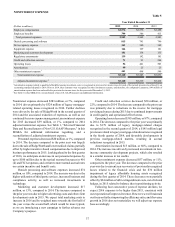

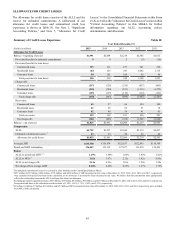

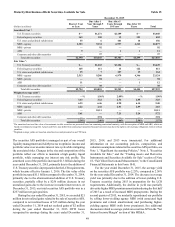

Other Nonperforming Assets

OREO decreased $43 million, or 43%, during 2015 compared

to 2014 as a result of net decreases of $36 million in residential

homes, $6 million in commercial properties, and $1 million in

residential construction related properties. Sales of OREO

resulted in proceeds of $120 million and $235 million during

2015 and 2014, respectively, contributing to net gains on sales

of OREO of $23 million and $42 million, respectively, inclusive

of valuation reserves.

Geographically, most of our OREO properties are located

in Florida, Georgia, and North Carolina. Residential and

commercial real estate properties comprised 70% and 20%,

respectively, of the $56 million in total OREO at December 31,

2015, with the remainder related to land and other properties.

Upon foreclosure, the values of these properties were reevaluated

and, if necessary, written down to their then-current estimated

value less estimated costs to sell. Any further decreases in

property values could result in additional losses as they are

periodically revalued. See the "Non-recurring Fair Value

Measurements" section within Note 18, "Fair Value Election and

Measurement," to the Consolidated Financial Statements in this

Form 10-K for additional information.

Gains and losses on the sale of OREO are recorded in other

noninterest expense in the Consolidated Statements of Income.

Sales of OREO and the related gains or losses are highly

dependent on our disposition strategy and buyer opportunities.

We are actively managing and disposing of these foreclosed

assets to minimize future losses.

Accruing loans past due 90 days or more included LHFI and

LHFS, and totaled $981 million and $1.1 billion, at December

31, 2015 and 2014, respectively. Of these, 96% and 97% were

government-guaranteed at December 31, 2015 and 2014,

respectively. Accruing LHFI past due 90 days or more decreased

$76 million, or 7%, during 2015, primarily driven by reductions

in government-guaranteed loans.

Restructured Loans

To maximize the collection of loan balances, we evaluate

troubled loans on a case-by-case basis to determine if a loan

modification is appropriate. We pursue loan modifications when

there is a reasonable chance that an appropriate modification

would allow our client to continue servicing the debt. For loans

secured by residential real estate, if the client demonstrates a loss

of income such that the client cannot reasonably support a

modified loan, we may pursue short sales and/or deed-in-lieu

arrangements. For loans secured by income producing

commercial properties, we perform an in-depth and ongoing

programmatic review. We review a number of factors, including

cash flows, loan structures, collateral values, and guarantees to

identify loans within our income producing commercial loan

portfolio that are most likely to experience distress.

Based on our review of the aforementioned factors, and our

assessment of overall risk, we evaluate the benefits of proactively

initiating discussions with our clients to improve a loan’s risk

profile. In some cases, we may renegotiate terms of their loans

so that they have a higher likelihood of continuing to perform.

To date, we have restructured loans in a variety of ways to help

our clients service their debt and to mitigate the potential for

additional losses. The primary restructuring methods being

offered to our residential clients are reductions in interest rates,

extensions of terms, or forgiveness of principal. For commercial

loans, the primary restructuring method is the extension of terms.

Loans with modifications deemed to be economic

concessions resulting from borrower financial difficulties are

reported as TDRs. Accruing loans may retain accruing status at

the time of restructure and the status is determined by, among

other things, the nature of the restructure, the borrower's

repayment history, and the borrower's repayment capacity.

Nonaccruing loans that are modified and demonstrate a

sustainable history of repayment performance in accordance

with their modified terms, typically six months, are usually

reclassified to accruing TDR status. Generally, once a residential

loan becomes a TDR, we expect that the loan will continue to

be reported as a TDR for its remaining life, even after returning

to accruing status (unless the modified rates and terms at the time

of modification were available in the market at the time of the

modification, or if the loan is subsequently remodified at market

rates). We note that some restructurings may not ultimately result

in the complete collection of principal and interest (as modified

by the terms of the restructuring), culminating in default, which

could result in additional incremental losses. These potential

incremental losses are factored into our ALLL estimate. The level

of re-defaults will likely be affected by future economic

conditions. See Note 6, "Loans," to the Consolidated Financial

Statements in this Form 10-K for more information.