SunTrust 2015 Annual Report Download - page 112

Download and view the complete annual report

Please find page 112 of the 2015 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

|

|

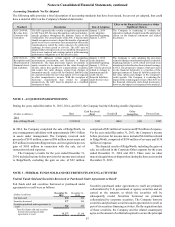

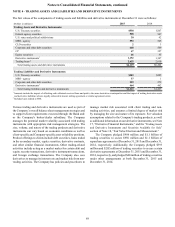

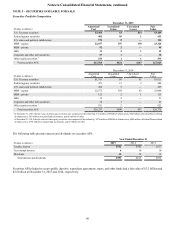

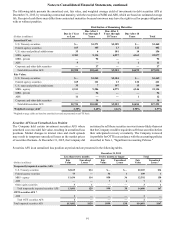

Notes to Consolidated Financial Statements, continued

84

would more-likely-than-not reduce the fair value of a reporting

unit below its carrying amount. In the third quarter of 2015, the

Company elected to prospectively change the date of its annual

goodwill impairment test from September 30 to October 1 to

better align the timing of the test with the availability of key

inputs.

If, after considering all relevant events and circumstances,

the Company determines it is not more-likely-than-not that the

fair value of a reporting unit is less than its carrying amount, then

performing an impairment test is not necessary. If the Company

elects to bypass the qualitative analysis, or concludes via

qualitative analysis that it is more-likely-than-not that the fair

value of a reporting unit is less than its carrying value, a two-

step goodwill impairment test is performed. In the first step, the

fair value of each reporting unit is compared with its carrying

value. If the fair value is greater than the carrying value, then the

reporting unit's goodwill is deemed not to be impaired. If the fair

value is less than the carrying value, then the second step is

performed, which measures the amount of impairment by

comparing the carrying amount of goodwill to its implied fair

value. If the implied fair value of the goodwill exceeds the

carrying amount, there is no impairment. If the carrying amount

exceeds the implied fair value of the goodwill, an impairment

charge is recorded for the excess.

Identified intangible assets that have a finite life are

amortized over their useful lives and are evaluated for

impairment whenever events or changes in circumstances

indicate the carrying amount of the assets may not be

recoverable. For additional information on the Company’s

activities related to goodwill and other intangibles, see Note 9,

“Goodwill and Other Intangible Assets.”

MSRs

The Company recognizes as assets the rights to service mortgage

loans, either when the loans are sold and the associated servicing

rights are retained or when servicing rights are purchased from

a third party. The Company has elected to measure all MSRs at

fair value. Fair value is determined by projecting net servicing

cash flows, which are then discounted to estimate fair value. The

Company actively hedges the change in fair value of its MSRs.

The fair value of MSRs is impacted by a variety of factors,

including prepayment assumptions, discount rates, delinquency

rates, contractually specified servicing fees, servicing costs, and

underlying portfolio characteristics. The underlying

assumptions and estimated values are corroborated by values

received from independent third parties and comparisons to

market transactions. MSRs are reported on the Consolidated

Balance Sheets in other intangible assets. Both servicing fees,

which are recognized when they are received, and changes in the

fair value of MSRs are reported in mortgage servicing related

income in the Consolidated Statements of Income. For additional

information on the Company’s servicing rights, see Note 9,

“Goodwill and Other Intangible Assets.”

Other Real Estate Owned

Assets acquired through, or in lieu of, loan foreclosure are held

for sale and are initially recorded at the lower of the loan’s cost

basis or the asset’s fair value at the date of foreclosure, less

estimated selling costs. To the extent fair value, less cost to sell,

is less than the loan’s cost basis, the difference is charged to the

ALLL at the date of transfer into OREO. The Company estimates

market values based primarily on appraisals and other market

information. Any subsequent changes in value as well as gains

or losses from the disposition on these assets are reported in

noninterest expense in the Consolidated Statements of Income.

For additional information on the Company's activities related

to OREO, see Note 18, “Fair Value Election and Measurement.”

Loan Sales and Securitizations

The Company sells and at times may securitize loans and other

financial assets. When the Company securitizes assets, it may

hold a portion of the securities issued, including senior interests,

subordinated and other residual interests, interest-only strips,

and principal-only strips, all of which are considered retained

interests in the transferred assets. Retained securitized interests

are recognized and initially measured at fair value. The interests

in securitized assets held by the Company are typically classified

as either securities AFS or trading assets and measured at fair

value, which is based on independent, third party market prices,

market prices for similar assets, or discounted cash flow

analyses. If market prices are not available, fair value is

calculated using management’s best estimates of key

assumptions, including credit losses, loan repayment speeds, and

discount rates commensurate with the risks involved.

The Company transfers first lien residential mortgage loans

in conjunction with GSE securitization transactions, whereby

the loans are exchanged for cash or securities that are readily

redeemable for cash and servicing rights are retained. Net gains

on the sale of residential mortgage loans are recorded at inception

of the associated IRLCs within mortgage production related

income in the Consolidated Statements of Income. The net gains

reflect the change in value of the loans resulting from changes

in interest rates from the time the Company enters into IRLCs

with borrowers and when the loan is closed, adjusted for pull

through rates and excluding hedge transactions initiated to

mitigate this market risk. For additional information on the

Company’s securitization activities, see Note 10, “Certain

Transfers of Financial Assets and Variable Interest Entities.”

Income Taxes

The provision for income taxes is based on income and expense

reported for financial statement purposes after adjustment for

permanent differences such as interest income from lending to

tax-exempt entities and tax credits from community

reinvestment activities. The deferral method of accounting is

used on investments that generate investment tax credits, such

that the investment tax credits are recognized as a reduction to

the related asset. Deferred income tax assets and liabilities result

from differences between the timing of the recognition of assets

and liabilities for financial reporting purposes and for income

tax purposes. These assets and liabilities are measured using the

enacted tax rates and laws that are expected to apply in the periods

in which the deferred tax assets or liabilities are expected to be

realized. Subsequent changes in the tax laws require adjustment

to these assets and liabilities with the cumulative effect included

in the provision for income taxes for the period in which the

change is enacted. A valuation allowance is recognized for a DTA

if, based on the weight of available evidence, it is more-likely-

than-not that some portion or all of the DTA will not be realized.

In computing the income tax provision, the Company evaluates