SunTrust 2015 Annual Report Download - page 89

Download and view the complete annual report

Please find page 89 of the 2015 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

|

|

61

sheets through the financial instruments' respective maturities

and is considered a longer term measure.

A positive net interest income sensitivity in a rising rate

environment indicates that over the forecast horizon of one year,

asset based interest income will increase more quickly than

liability based interest expense due to balance sheet

composition. A negative MVE sensitivity in a rising rate

environment indicates that the value of financial assets will

decrease more than the value of financial liabilities.

One of the primary methods that we use to quantify and

manage interest rate risk is simulation analysis, which we use to

model net interest income from assets, liabilities, and derivative

positions under various interest rate scenarios and balance sheet

structures. This analysis measures the sensitivity of net interest

income over a two-year time horizon, which differs from the

interest rate sensitivities in Table 22, which reflect a one-year

time horizon. Key assumptions in the simulation analysis (and

in the valuation analysis discussed below) relate to the behavior

of interest rates and spreads, the changes in product balances,

and the behavior of loan and deposit clients in different rate

environments. This analysis incorporates several assumptions,

the most material of which relate to the repricing and behavioral

fluctuations of deposits with indeterminate or non-contractual

maturities.

As the future path of interest rates is not known, we use

simulation analysis to project net interest income under various

scenarios including implied forward and deliberately extreme

and perhaps unlikely scenarios. The analyses may include rapid

and gradual ramping of interest rates, rate shocks, basis risk

analysis, and yield curve twists. Specific strategies are also

analyzed to determine their impact on net interest income levels

and sensitivities.

The sensitivity analysis presented in Table 22 is measured

as a percentage change in net interest income due to

instantaneous moves in benchmark interest rates. Estimated

changes set forth below are dependent upon material

assumptions such as those previously discussed.

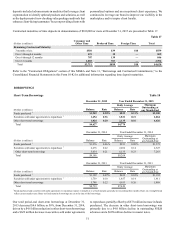

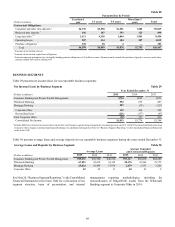

Net Interest Income Asset Sensitivity Table 22

Estimated % Change in

Net Interest Income Over 12 Months 1

December 31, 2015 December 31, 2014

Rate Change

+200 bps 5.7% 6.7%

+100 bps 3.0% 3.5%

-25 bps (1.2)% (1.0)%

1 Estimated % change of net interest income is reflected on a non-FTE basis.

The decrease in net interest income asset sensitivity at

December 31, 2015 compared to December 31, 2014 is due to

growth in interest-bearing indeterminate maturity deposits, an

increase in the securities AFS portfolio related to LCR

compliance, and slower assumed prepayments. See additional

discussion related to net interest income in the "Net Interest

Income/Margin" section of this MD&A.

We also perform valuation analyses, which we use for

discerning levels of risk present in the balance sheet and

derivative positions that might not be taken into account in the

net interest income simulation horizon. Whereas a net interest

income simulation highlights exposures over a relatively short

time horizon, our valuation analysis incorporates all cash flows

over the estimated remaining life of all balance sheet and

derivative positions. The valuation of the balance sheet, at a point

in time, is defined as the discounted present value of asset cash

flows and derivative cash flows minus the discounted present

value of liability cash flows, the net of which is referred to as

MVE. The sensitivity of MVE to changes in the level of interest

rates is a measure of the longer-term repricing risk and options

risk embedded in the balance sheet. Similar to the net interest

income simulation, MVE uses instantaneous changes in rates.

However, MVE values only the current balance sheet and does

not incorporate originations of new/replacement business or

balance sheet growth that are used in the net interest income

simulation model. As with the net interest income simulation

model, assumptions about the timing and variability of balance

sheet cash flows are critical in the MVE analysis. Particularly

important are the assumptions driving prepayments and the

expected changes in balances and pricing of the indeterminate

deposit portfolios. At December 31, 2015, the MVE profile in

Table 23 indicated a decline in net balance sheet value due to

instantaneous upward changes in rates. MVE sensitivity is

reported in both upward and downward rate shocks.

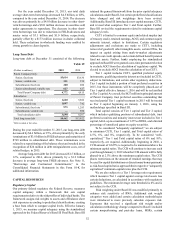

Market Value of Equity Sensitivity Table 23

Estimated % Change in MVE

December 31, 2015 December 31, 2014

Rate Change

+200 bps (8.2)% (4.2)%

+100 bps (3.7)% (1.5)%

-25 bps 0.7% 0.1%

The increase in MVE sensitivity compared to December 31,

2014 is primarily due to increased balance sheet duration arising

from a combination of factors including, but not limited to,

extending receive-fixed interest rate swaps, an increase in the

securities AFS portfolio related to LCR compliance, slightly

shorter deposit lives, and reduced prepayment speeds on

mortgage loans and securities. While an instantaneous and severe

shift in interest rates was used in this analysis to provide an

estimate of exposure under these rate scenarios, we believe that

a gradual shift in interest rates would have a much more modest

impact. Since MVE measures the discounted present value of

cash flows over the estimated lives of instruments, the change

in MVE does not directly correlate to the degree that earnings

would be impacted over a shorter time horizon (i.e., the current

year). Further, MVE does not take into account factors such as

future balance sheet growth, changes in product mix, changes in

yield curve relationships, and changing product spreads that

could mitigate the impact of changes in interest rates. The net

interest income simulation and valuation analyses do not include

actions that management may undertake to manage this risk in

response to anticipated changes in interest rates.

Market Risk from Trading Activities

We manage market risk associated with trading activities using

a comprehensive risk management approach, which includes

VAR metrics, as well as stress testing and sensitivity analysis.

All risk metrics are measured and monitored at the trading desk