SunTrust 2015 Annual Report Download - page 88

Download and view the complete annual report

Please find page 88 of the 2015 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

|

|

60

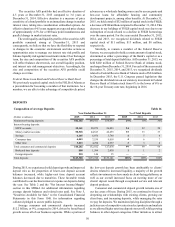

established policies, procedures, and standards. Risk Review,

one of our independent assurance functions, regularly assesses

and reports on business unit and enterprise asset quality, and the

integrity of our credit processes. Additionally, total borrower

exposure limits and concentration risk are established and

monitored. Credit risk may be mitigated through purchase of

credit loss protection via third party insurance and/or use of credit

derivatives such as CDS.

Borrower/counterparty (obligor) risk and facility risk is

evaluated using our risk rating methodology, which is utilized

in all lines of business. We use various risk models to estimate

both expected and unexpected loss, which incorporates both

internal and external default and loss experience. To the extent

possible, we collect and use internal data to ensure the validity,

reliability, and accuracy of our risk models used in default,

severity, and loss estimation.

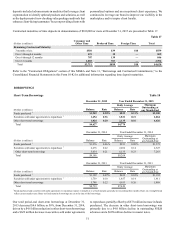

Operational Risk Management

We face ongoing and emerging risks and regulations related to

the activities that surround the delivery of banking and financial

products. Coupled with external influences such as market

conditions, fraudulent activities, disasters, cyber-attacks and

other security risks, country risk, vendor risk, and legal risk, the

potential for operational and reputational loss remains elevated.

Our operations rely on computer systems, networks, the

internet, digital applications, and the telecommunications and

computer systems of third parties to perform business activities.

The use of digital technologies introduces cyber-security risk

that can manifest in the form of information theft, physical

disruptions, criminal acts by individuals, groups, or nation states,

and a client’s inability to access online services. We use a wide

array of techniques to secure our operations and proprietary

information such as Board approved policies and programs,

network monitoring, access controls, dedicated security

personnel, and defined insurance instruments, as well as consult

with third-party data security experts.

To control cyber-security risk, we maintain an active

information security program that conforms to FFIEC guidance.

This information security program is aligned with our

operational risks and is overseen by executive management, the

Board, and our independent audit function. It continually

monitors and evaluates threats, events, and the performance of

its business operations and continually adapts and modifies its

risk reduction activities accordingly. We also have a cyber

liability insurance policy that provides us with coverage against

certain losses. expenses, and damages associated with cyber risk.

Further, we recognize our role in the overall national

payments system and we have adopted the National Institute of

Standards and Technology Cyber Security Framework ("NIST

CSF"). We also fully participate in the federally recognized

financial sector information sharing organization structure,

known as the Financial Services Information Sharing and

Analysis Center ("FS-ISAC"). Digital technology is constantly

evolving, and new and unforeseen threats and actions by others

may disrupt operations or result in losses beyond our risk control

thresholds. Although we invest substantial time and resources to

manage and reduce cyber risk, it is not possible to completely

eliminate this risk.

We believe that effective management of operational risk,

defined as the risk of loss resulting from inadequate or failed

internal processes, people and systems, or from external events,

plays a major role in both the level and the stability of our

profitability. Our Operational Risk Management function

oversees an enterprise-wide framework intended to identify,

assess, control, monitor, and report on operational risks

Company-wide. These processes support our goals to minimize

future operational losses and strengthen our performance by

maintaining sufficient capital to absorb operational losses that

are incurred.

Operational Risk Management is overseen by our CORO,

who reports directly to the CRO. The operational risk governance

structure includes an operational risk manager and support staff

within each business segment and corporate function. These risk

managers are responsible for execution of risk management

within their areas in compliance with CRM's policies and

procedures.

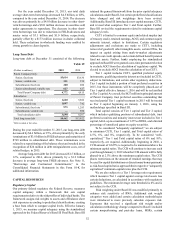

Market Risk Management

Market risk refers to potential losses arising from changes in

interest rates, foreign exchange rates, equity prices, commodity

prices, and other relevant market rates or prices. Interest rate risk,

defined as the exposure of net interest income and MVE to

changes in interest rates, is our primary market risk and mainly

arises from the structure of our balance sheet. Variable rate loans,

prior to any hedging related actions, were approximately 60%

of total loans at December 31, 2015, and after giving

consideration to hedging related actions, were approximately

48% of total loans. Approximately 4-5% of our variable rate

loans at December 31, 2015 had coupon rates that were equal to

a contractually specified interest rate floor. In addition to interest

rate risk, we are also exposed to market risk in our trading

instruments measured at fair value. Our ALCO meets regularly

and is responsible for reviewing our open market positions and

establishing policies to monitor and limit exposure to market

risk.

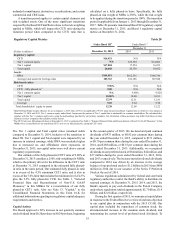

Market Risk from Non-Trading Activities

The primary goal of interest rate risk management is to control

exposure to interest rate risk, within policy limits approved by

the Board. These limits and guidelines reflect our appetite for

interest rate risk over both short-term and long-term horizons.

No limit breaches occurred during the year ended December 31,

2015.

The major sources of our non-trading interest rate risk are

timing differences in the maturity and repricing characteristics

of assets and liabilities, changes in the shape of the yield curve,

and the potential exercise of freestanding or embedded options.

We measure these risks and their impact by identifying and

quantifying exposures through the use of sophisticated

simulation and valuation models, which, as described in

additional detail below, are employed by management to

understand net interest income sensitivity and MVE sensitivity.

These measures show that our interest rate risk profile is

moderately asset sensitive at December 31, 2015.

MVE and net interest income sensitivity are complementary

interest rate risk metrics and should be viewed together. Net

interest income sensitivity captures asset and liability repricing

mismatches for one year, inclusive of forecast balance sheet

changes, and is considered a shorter term measure, while MVE

sensitivity captures mismatches within the period end balance