SunTrust 2015 Annual Report Download - page 133

Download and view the complete annual report

Please find page 133 of the 2015 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

|

|

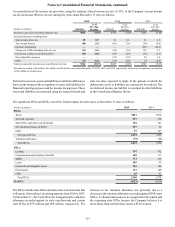

Notes to Consolidated Financial Statements, continued

105

reported in mortgage servicing related income in the

Consolidated Statements of Income.

At December 31, 2015 and 2014, the total UPB of mortgage

loans serviced was $148.2 billion and $142.1 billion,

respectively. Included in these amounts were $121.0 billion and

$115.5 billion at December 31, 2015 and 2014, respectively, of

loans serviced for third parties. The Company purchased MSRs

on residential loans with a UPB of $10.3 billion during the year

ended December 31, 2015, all of which are reflected in the UPB

amounts above. The Company purchased MSRs on residential

loans with a UPB of $10.9 billion during the year ended

December 31, 2014. During the years ended December 31, 2015

and 2014, the Company sold MSRs on residential loans, at a

price approximating their fair value, with a UPB of $803 million

and $878 million, respectively.

The Company calculates the fair value of MSRs using a

valuation model that calculates the present value of estimated

future net servicing income using prepayment projections,

spreads, and other assumptions. Senior management and the

STM Valuation Committee review all significant assumptions at

least quarterly, comparing these inputs to various sources of

market data. Changes to valuation model inputs are reflected in

the periods' results. See Note 18, “Fair Value Election and

Measurement,” for further information regarding the Company's

MSR valuation methodology.

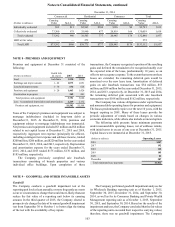

A summary of the key inputs used to estimate the fair value

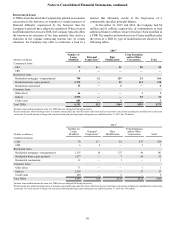

of the Company’s MSRs at December 31, 2015 and 2014, and

the sensitivity of the fair values to immediate 10% and 20%

adverse changes in those inputs, are presented in the following

table.

(Dollars in millions)

December 31,

2015

December 31,

2014

Fair value of MSRs $1,307 $1,206

Prepayment rate assumption (annual) 10% 11%

Decline in fair value from 10%

adverse change $49 $46

Decline in fair value from 20%

adverse change 94 88

Option adjusted spread (annual) 8% 10%

Decline in fair value from 10%

adverse change $64 $55

Decline in fair value from 20%

adverse change 123 105

Weighted-average life (in years) 6.6 6.4

Weighted-average coupon 4.1% 4.2%

These MSR sensitivities are hypothetical and should be used

with caution. Changes in fair value based on variations in

assumptions generally cannot be extrapolated because (i) the

relationship of the change in an assumption to the change in fair

value may not be linear and (ii) changes in one assumption may

result in changes in another, which might magnify or counteract

the sensitivities. The sensitivities do not reflect the effect of

hedging activity undertaken by the Company to offset changes

in the fair value of MSRs. See Note 17, “Derivative Financial

Instruments,” for further information regarding these hedging

activities.

Consumer Loan Servicing Rights

In June 2015, the Company completed the securitization of $1.0

billion of indirect auto loans, with servicing rights retained, and

recognized a $13 million servicing asset at the time of sale. See

Note 10, “Certain Transfers of Financial Assets and Variable

Interest Entities,” for additional information on the Company's

securitization transactions.

Income earned by the Company on its consumer loan

servicing rights is derived primarily from contractually specified

servicing fees and other ancillary fees. Such income earned for

the year ended December 31, 2015 was $5 million, and is

reported in other noninterest income in the Consolidated

Statements of Income. There was no income earned on consumer

loan servicing rights for the years ended December 31, 2014 and

2013.

At December 31, 2015, the total UPB of consumer indirect

loans serviced was $807 million, all of which were serviced for

third parties. No consumer loan servicing rights were purchased

or sold during the years ended December 31, 2015 and 2014.

Consumer loan servicing rights are accounted for at

amortized cost and are monitored for impairment on an ongoing

basis. The Company calculates the fair value of consumer

servicing rights using a valuation model that calculates the

present value of estimated future net servicing income using

prepayment projections and other assumptions. Impairment, if

any, is recognized when changes in valuation model inputs reflect

a fair value for the servicing asset that is below its respective

carrying value. At December 31, 2015, both the amortized cost

and the fair value of the Company's consumer loan servicing

rights were $9 million.

NOTE 10 - CERTAIN TRANSFERS OF FINANCIAL ASSETS AND VARIABLE INTEREST ENTITIES

The Company has transferred loans and securities in sale or

securitization transactions in which the Company retains certain

beneficial interests or retains servicing rights. Cash receipts on

beneficial interests held related to these transfers were $19

million, $21 million, and $36 million for the years ended

December 31, 2015, 2014, and 2013, respectively. The servicing

fees related to these asset transfers (excluding servicing fees for

residential mortgage loan transfers to GSEs, which are discussed

in Note 9, “Goodwill and Other Intangible Assets”) were

immaterial for each of the years ended December 31, 2015, 2014,

and 2013.

When a transfer or other transaction occurs with a VIE, the

Company first determines whether it has a VI in the VIE. A VI

is typically in the form of securities representing retained

interests in transferred assets and, at times, servicing rights and

collateral management fees. When determining whether to

consolidate the VIE, the Company evaluates whether it has both

(i) the power to direct the activities that most significantly impact

the economic performance of the VIE, and (ii) the obligation to

absorb losses, or the right to receive benefits, that could

potentially be significant to the VIE.

To determine whether a transfer should be accounted for as

a sale or a secured borrowing, the Company evaluates whether: