SunTrust 2015 Annual Report Download - page 151

Download and view the complete annual report

Please find page 151 of the 2015 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

|

|

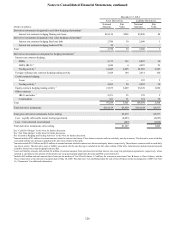

Notes to Consolidated Financial Statements, continued

123

deliver tax credits, and was recorded in other liabilities in the

Consolidated Balance Sheets.

Public Deposits

The Company holds public deposits from various states in which

it does business. Individual state laws require banks to

collateralize public deposits, typically as a percentage of their

public deposit balance in excess of FDIC insurance and may also

require a cross-guarantee among all banks holding public

deposits of the individual state. The amount of collateral required

varies by state and may also vary by institution within each state,

depending on the individual state's risk assessment of depository

institutions. Certain of the states in which the Company holds

public deposits use a pooled collateral method, whereby in the

event of default of a bank holding public deposits, the collateral

of the defaulting bank is liquidated to the extent necessary to

recover the loss of public deposits of the defaulting bank. To the

extent the collateral is insufficient, the remaining public deposit

balances of the defaulting bank are recovered through an

assessment of the other banks holding public deposits in that

state. The maximum potential amount of future payments the

Company could be required to make is dependent on a variety

of factors, including the amount of public funds held by banks

in the states in which the Company also holds public deposits

and the amount of collateral coverage associated with any

defaulting bank. Individual states appear to be monitoring this

risk and evaluating collateral requirements; therefore, the

likelihood that the Company would have to perform under this

guarantee is dependent on whether any banks holding public

funds default as well as the adequacy of collateral coverage.

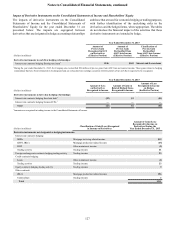

Other

In the normal course of business, the Company enters into

indemnification agreements and provides standard

representations and warranties in connection with numerous

transactions. These transactions include those arising from

securitization activities, underwriting agreements, merger and

acquisition agreements, swap clearing agreements, loan sales,

contractual commitments, payment processing, sponsorship

agreements, and various other business transactions or

arrangements. The extent of the Company's obligations under

these indemnification agreements depends upon the occurrence

of future events; therefore, the Company's potential future

liability under these arrangements is not determinable. STIS and

STRH, broker-dealer affiliates of the Company, use a common

third party clearing broker to clear and execute their customers'

securities transactions and to hold customer accounts. Under

their respective agreements, STIS and STRH agree to indemnify

the clearing broker for losses that result from a customer's failure

to fulfill its contractual obligations. As the clearing broker's

rights to charge STIS and STRH have no maximum amount, the

Company believes that the maximum potential obligation cannot

be estimated. However, to mitigate exposure, the affiliate may

seek recourse from the customer through cash or securities held

in the defaulting customers' account. For the years ended

December 31, 2015, 2014, and 2013, STIS and STRH

experienced minimal net losses as a result of the indemnity. The

clearing agreements expire in May 2020 for both STIS and

STRH.

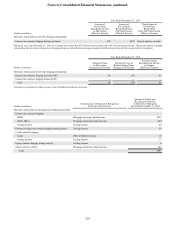

NOTE 17 - DERIVATIVE FINANCIAL INSTRUMENTS

The Company enters into various derivative financial

instruments, both in a dealer capacity to facilitate client

transactions and as an end user as a risk management tool. The

ALCO monitors all derivative activities. When derivatives have

been entered into with clients, the Company generally manages

the risk associated with these derivatives within the framework

of its VAR methodology that monitors total daily exposure and

seeks to manage the exposure on an overall basis. Derivatives

are also used as a risk management tool to hedge the Company’s

balance sheet exposure to changes in identified cash flow and

fair value risks, either economically or in accordance with hedge

accounting provisions. The Company’s Corporate Treasury

function is responsible for employing the various hedge

accounting strategies to manage these objectives. Additionally,

as a normal part of its operations, the Company enters into IRLCs

on mortgage loans that are accounted for as freestanding

derivatives and has certain contracts containing embedded

derivatives that are measured, in their entirety, at fair value. All

freestanding derivatives and any embedded derivatives that the

Company bifurcates from the host contracts are measured at fair

value in the Consolidated Balance Sheets in trading assets and

derivative instruments and trading liabilities and derivative

instruments. The associated gains and losses are either

recognized in AOCI, net of tax, or within the Consolidated

Statements of Income, depending upon the use and designation

of the derivatives.

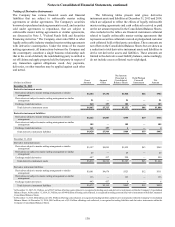

Credit and Market Risk Associated with Derivative Instruments

Derivatives expose the Company to counterparty credit risk if

the counterparty to the derivative contract does not perform as

expected. The Company minimizes the credit risk of derivatives

by entering into transactions with counterparties with defined

exposure limits based on their credit quality and in accordance

with established policies and procedures. All counterparties are

regularly reviewed by the Company’s Credit Risk Management

division and appropriate action is taken to adjust the exposure

to certain counterparties as necessary. The Company’s derivative

transactions may also be governed by ISDA documentation or

other legally enforceable industry standard master netting

agreements. In certain cases and depending on the nature of the

underlying derivative transactions, bilateral collateral

agreements are also utilized. Furthermore, the Company and its

subsidiaries are subject to OTC derivative clearing requirements,

which require certain derivatives to be cleared through central

clearinghouses with which the Company and other

counterparties are required to post initial margin. To mitigate the

risk of non-payment, variation margin is received or paid daily

based on the net asset or liability position of the contracts.

When the Company has more than one outstanding

derivative transaction with a single counterparty, and there exists

a legal right of offset with that counterparty, the Company

considers its exposure to the counterparty to be the net fair value

of its derivative positions with that counterparty. If the net fair