SunTrust 2015 Annual Report Download - page 159

Download and view the complete annual report

Please find page 159 of the 2015 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

|

|

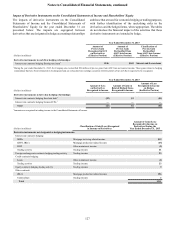

Notes to Consolidated Financial Statements, continued

131

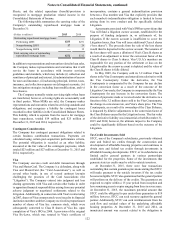

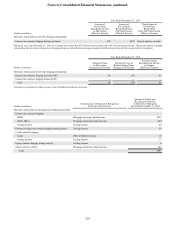

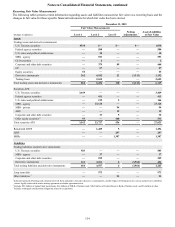

Credit Derivative Instruments

As part of SunTrust's trading businesses, the Company enters

into contracts that are, in form or substance, written guarantees:

specifically, CDS, risk participations, and TRS. The Company

accounts for these contracts as derivatives and, accordingly,

records these contracts at fair value, with changes in fair value

recognized in trading income in the Consolidated Statements of

Income.

The Company writes CDS, which are agreements under

which the Company receives premium payments from its

counterparty for protection against an event of default of a

reference asset. In the event of default under the CDS, the

Company would either settle its obligation net in cash or make

a cash payment to its counterparty and take delivery of the

defaulted reference asset, from which the Company may recover

all, a portion, or none of the credit loss, depending on the

performance of the reference asset. Events of default, as defined

in the CDS agreements, are generally triggered upon the failure

to pay and similar events related to the issuer(s) of the reference

asset. When the Company has written CDS, all written CDS

contracts reference single name corporate credits or corporate

credit indices. The Company generally enters into offsetting

CDS for the underlying reference asset, under which the

Company pays a premium to its counterparty for protection

against an event of default on the reference asset. The

counterparties to these purchased CDS are generally of high

creditworthiness and typically have ISDA master netting

agreements in place that subject the CDS to master netting

provisions, thereby mitigating the risk of non-payment to the

Company. As such, at December 31, 2015, the Company did not

have any material risk of making a non-recoverable payment on

any written CDS. During 2015 and 2014, the only instances of

default on written CDS were driven by credit indices with

constituent credit default. In all cases where the Company made

resulting cash payments to settle, the Company collected like

amounts from the counterparties to the offsetting purchased

CDS.

There were no written CDS at December 31, 2015. At

December 31, 2014, written CDS had remaining terms of four

years. The fair value of written CDS was $1 million at

December 31, 2014. The maximum guarantees outstanding at

December 31, 2014, as measured by the gross notional amount

of written CDS, was $20 million. At December 31, 2015 and

2014, the gross notional amounts of purchased CDS contracts,

which protect the Company against default of a reference asset,

were $150 million and $190 million, respectively. The fair values

of purchased CDS were $1 million and $5 million at December

31, 2015 and 2014, respectively.

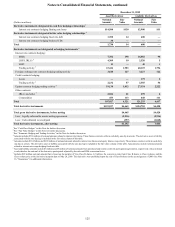

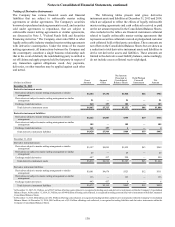

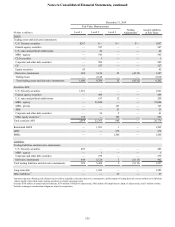

The Company has also entered into TRS contracts on loans.

The Company’s TRS business consists of matched trades, such

that when the Company pays depreciation on one TRS, it receives

the same amount on the matched TRS. To mitigate its credit risk,

the Company typically receives initial cash collateral from the

counterparty upon entering into the TRS and is entitled to

additional collateral if the fair value of the underlying reference

assets deteriorates. There were $2.2 billion and $2.3 billion of

outstanding TRS notional balances at December 31, 2015 and

2014, respectively. The fair values of these TRS assets and

liabilities at December 31, 2015 were $57 million and $52

million, respectively, and related collateral held at December 31,

2015 was $492 million. The fair values of the TRS assets and

liabilities at December 31, 2014 were $19 million and $14

million, respectively, and related collateral held at December 31,

2014 was $373 million. For additional information on the

Company's TRS contracts, see Note 10, "Certain Transfers of

Financial Assets and Variable Interest Entities," as well as Note

18, "Fair Value Election and Measurement."

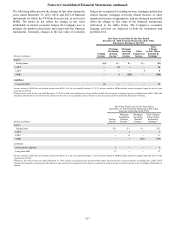

The Company writes risk participations, which are credit

derivatives, whereby the Company has guaranteed payment to

a dealer counterparty in the event the counterparty experiences

a loss on a derivative, such as an interest rate swap, due to a

failure to pay by the counterparty’s customer (the “obligor”) on

that derivative. The Company monitors its payment risk on its

risk participations by monitoring the creditworthiness of the

obligors, which is based on the normal credit review process the

Company would have performed had it entered into a derivative

directly with the obligors. The obligors are all corporations or

partnerships. The Company continues to monitor the

creditworthiness of the obligors and the likelihood of payment

could change at any time due to unforeseen circumstances. To

date, no material losses have been incurred related to the

Company’s written risk participations. At December 31, 2015

and 2014, the remaining terms on these risk participations

generally ranged from less than one year to eight years and from

one to nine years, respectively, with a weighted average on the

maximum estimated exposure of 5.6 and 5.2 years, respectively.

The Company’s maximum estimated exposure to written risk

participations, as measured by projecting a maximum value of

the guaranteed derivative instruments based on interest rate

curve simulations and assuming 100% default by all obligors on

the maximum values, was approximately $55 million and $31

million at December 31, 2015 and 2014, respectively. The fair

values of the written risk participations were immaterial at both

December 31, 2015 and 2014. As part of its trading activities,

the Company may enter into purchased risk participations to

mitigate credit exposure to a derivative counterparty.

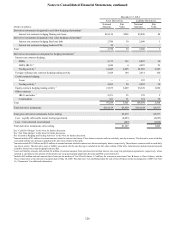

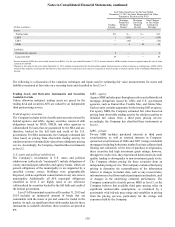

Cash Flow Hedging Instruments

The Company utilizes a comprehensive risk management

strategy to monitor sensitivity of earnings to movements in

interest rates. Specific types of funding and principal amounts

hedged are determined based on prevailing market conditions

and the shape of the yield curve. In conjunction with this strategy,

the Company may employ various interest rate derivatives as

risk management tools to hedge interest rate risk from recognized

assets and liabilities or from forecasted transactions. The terms

and notional amounts of derivatives are determined based on

management’s assessment of future interest rates, as well as other

factors.

Interest rate swaps have been designated as hedging the

exposure to the benchmark interest rate risk associated with

floating rate loans. At December 31, 2015 and 2014, the

maturities for hedges of floating rate loans ranged from less than

one year to seven years and from less than one year to four years,

respectively, with the weighted average being 3.3 and 1.9 years,

respectively. These hedges have been highly effective in

offsetting the designated risks, yielding an immaterial amount

of ineffectiveness for the year ended December 31, 2015 and

2014. At December 31, 2015, $229 million of deferred net pre-

tax gains on derivative instruments designated as cash flow