SunTrust 2015 Annual Report Download - page 149

Download and view the complete annual report

Please find page 149 of the 2015 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

|

|

Notes to Consolidated Financial Statements, continued

121

The Company monitors its credit exposure under standby

letters of credit in the same manner as it monitors other

extensions of credit in accordance with its credit policies. An

internal assessment of the PD and loss severity in the event of

default is performed, consistent with the methodologies used for

all commercial borrowers. The management of credit risk for

letters of credit leverages the risk rating process to focus greater

visibility on higher risk and/or higher dollar letters of credit. The

allowance for credit losses associated with letters of credit is a

component of the unfunded commitments reserve recorded in

other liabilities in the Consolidated Balance Sheets and is

included in the allowance for credit losses as disclosed in Note

7, “Allowance for Credit Losses.” Additionally, unearned fees

relating to letters of credit are recorded in other liabilities. The

net carrying amount of unearned fees was immaterial at

December 31, 2015 and 2014.

Loan Sales and Servicing

STM, a consolidated subsidiary of the Company, originates and

purchases residential mortgage loans, a portion of which are sold

to outside investors in the normal course of business, through a

combination of whole loan sales to GSEs, Ginnie Mae, and non-

agency investors. Prior to 2008, the Company also sold mortgage

loans through a limited number of Company-sponsored

securitizations. When mortgage loans are sold, representations

and warranties regarding certain attributes of the loans are made

to third party purchasers. Subsequent to the sale, if a material

underwriting deficiency or documentation defect is discovered,

STM may be obligated to repurchase the mortgage loan or to

reimburse an investor for losses incurred (make whole requests),

if such deficiency or defect cannot be cured by STM within the

specified period following discovery. Additionally, breaches of

underwriting and servicing representations and warranties can

result in loan repurchases, as well as adversely affect the

valuation of MSRs, servicing advances, or other mortgage loan-

related exposures, such as OREO. These representations and

warranties may extend through the life of the mortgage loan.

STM’s risk of loss under its representations and warranties is

partially driven by borrower payment performance since

investors will perform extensive reviews of delinquent loans as

a means of mitigating losses.

Non-agency loan sales include whole loan sales and loans

sold in private securitization transactions. While representations

and warranties have been made related to these sales, they differ

from those made in connection with loans sold to the GSEs in

that non-agency loans may not be required to meet the same

underwriting standards and non-agency investors may be

required to demonstrate that an alleged breach is material and

caused the investors' loss.

Loans sold to Ginnie Mae are insured by the FHA and

guaranteed by the VA. As servicer, the Company may elect to

repurchase delinquent loans in accordance with Ginnie Mae

guidelines, however, the loans continue to be insured. The

Company indemnifies the FHA and VA for losses related to loans

not originated in accordance with their guidelines.

See Note 19, "Contingencies," for additional information on

current legal matters related to loan sales.

The Company previously reached agreements in principle

with Freddie Mac and Fannie Mae that relieve the Company of

certain existing and future repurchase obligations related to loans

sold from 2000-2008 to Freddie Mac and loans sold from

2000-2012 to Fannie Mae. Repurchase requests have declined

significantly as a result of the settlements. Repurchase requests

from GSEs, Ginnie Mae, and non-agency investors, for all

vintages, are illustrated in the following table that summarizes

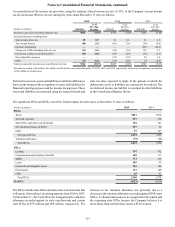

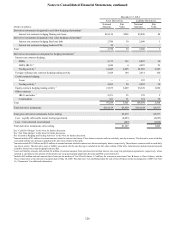

demand activity for the years ended December 31.

(Dollars in millions) 2015 2014 2013

Beginning pending repurchase

requests $47 $126 $655

Repurchase requests received 73 158 1,511

Repurchase requests resolved:

Repurchased (22) (28) (1,134)

Cured (81) (209) (906)

Total resolved (103) (237) (2,040)

Ending pending repurchase requests1$17 $47 $126

Percent from non-agency investors:

Pending repurchase requests 32.9% 6.7% 2.8%

Repurchase requests received 7.2% 0.9% 1.2%

1 Comprised of $11 million, $44 million, and $122 million from the GSEs, and $6

million, $3 million, and $4 million from non-agency investors at December 31, 2015,

2014, and 2013, respectively.

The repurchase and make whole requests received have been

primarily due to alleged material breaches of representations

related to compliance with the applicable underwriting

standards, including borrower misrepresentation and appraisal

issues. STM performs a loan-by-loan review of all requests and

contests demands to the extent they are not considered valid. The

following table summarizes the changes in the Company’s

reserve for mortgage loan repurchases for the years ended

December 31:

(Dollars in millions) 2015 2014 2013

Balance, at beginning of period $85 $78 $632

Repurchase (benefit)/provision (12) 12 114

Charge-offs, net of recoveries (16) (5) (668)

Balance, at end of period $57 $85 $78

A significant degree of judgment is used to estimate the mortgage

repurchase liability as the estimation process is inherently

uncertain and subject to imprecision. The Company believes that

its reserve appropriately estimates incurred losses based on its

current analysis and assumptions, inclusive of the Freddie Mac

and Fannie Mae settlement agreements, GSE owned loans

serviced by third party servicers, loans sold to private investors,

and other indemnifications.

Notwithstanding the aforementioned agreements with

Freddie Mac and Fannie Mae settling certain aspects of the

Company's repurchase obligations, those institutions preserve

their right to require repurchases arising from certain types of

events, and that preservation of rights can impact future losses

of the Company. While the repurchase reserve includes the

estimated cost of settling claims related to required repurchases,

the Company's estimate of losses depends on its assumptions

regarding GSE and other counterparty behavior, loan

performance, home prices, and other factors. The related liability

is recorded in other liabilities in the Consolidated Balance