Sallie Mae 2011 Annual Report Download - page 84

Download and view the complete annual report

Please find page 84 of the 2011 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

|

|

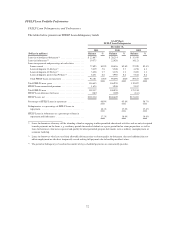

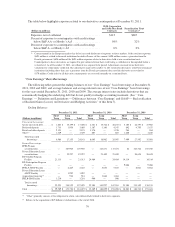

On July 1, 2011, we adopted Accounting Standards Update No. 2011-02, Receivables (Topic 310),

“A Creditor’s Determination of Whether a Restructuring Is a Troubled Debt Restructuring.” This new guidance

clarifies when a loan restructuring constitutes a troubled debt restructuring. In applying the new guidance we

have determined that certain Private Education Loans for which we have granted forbearance of greater than

three months are classified as troubled debt restructurings. If a loan meets the criteria for troubled debt

accounting then an allowance for loan loss is established which represents the present value of the losses that are

expected to occur over the remaining life of the loan. This accounting results in a higher allowance for loan

losses than our previously established allowance for these loans as our previous allowance for these loans

represented an estimate of charge-offs expected to occur over the next two years (two years being our loss

confirmation period). The new accounting guidance was effective as of July 1, 2011 but was required to be

applied retrospectively to January 1, 2011. This resulted in $124 million of additional provision for loan losses in

the third quarter of 2011 from approximately $3.8 billion of student loans being classified as troubled debt

restructurings. This new accounting guidance is only applied to certain borrowers who use their fourth or greater

month of forbearance during the time period this new guidance is effective. This new accounting guidance has

the effect of accelerating the recognition of expected losses related to our Private Education Loan portfolio. The

increase in the provision for losses as a result of this new accounting guidance does not reflect a decrease in

credit expectations of the portfolio or an increase in the expected life-of-loan losses related to this portfolio. We

believe forbearance is an accepted and effective collections and risk management tool for Private Education

Loans. We plan to continue to use forbearance and as a result, we expect to have additional loans classified as

troubled debt restructurings in the future (see “Financial Condition — Consumer Lending Portfolio Performance

— Allowance for Private Education Loan Losses” of this Item 7. for a further discussion on the use of

forbearance as a collection tool).

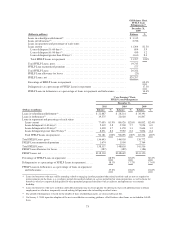

FFELP Loans are insured as to their principal and accrued interest in the event of default subject to a Risk

Sharing level based on the date of loan disbursement. These insurance obligations are supported by contractual

rights against the United States. For loans disbursed after October 1, 1993, and before July 1, 2006, we receive

98 percent reimbursement on all qualifying default claims. For loans disbursed on or after July 1, 2006, we

receive 97 percent reimbursement. For loans disbursed prior to October 1, 1993, we receive 100 percent

reimbursement.

The allowance for FFELP Loan losses uses historical experience of borrower default behavior and a two

year loss confirmation period to estimate the credit losses incurred in the loan portfolio at the reporting date. We

apply the default rate projections, net of applicable Risk Sharing, to each category for the current period to

perform our quantitative calculation. Once the quantitative calculation is performed, we review the adequacy of

the allowance for loan losses and determine if qualitative adjustments need to be considered.

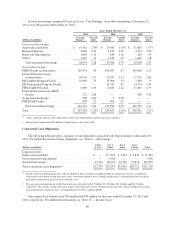

Premium and Discount Amortization

The most judgmental estimate for premium and discount amortization on student loans is the Constant

Prepayment Rate (“CPR”), which measures the rate at which loans in the portfolio pay down principal compared

to their stated terms. Loan consolidation, default, term extension and other prepayment factors affecting our CPR

estimates are affected by changes in our business strategy, changes in our competitor’s business strategies,

FFELP legislative changes, interest rates and changes to the current economic and credit environment. When we

determine the CPR we begin with historical prepayment rates due to consolidation activity, defaults, payoffs and

term extensions from the utilization of forbearance. We make judgments about which historical period to start

with and then make further judgments about whether that historical experience is representative of future

expectations and whether additional adjustment may be needed to those historical prepayment rates.

In the past the consolidation of FFELP Loans and Private Education Loans significantly affected our CPRs

and updating those assumptions often resulted in material adjustments to our amortization expense. As a result of

the passage of HCERA, there is no longer the ability to consolidate under the FFELP. In addition, due to the

current U.S. economic and credit environment, we, as well as many other industry competitors, have suspended

our Private Education Loans consolidation program. As a result, we do not expect to consolidate FFELP Loans

82