Sallie Mae 2011 Annual Report Download - page 134

Download and view the complete annual report

Please find page 134 of the 2011 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

|

|

SLM CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

2. Significant Accounting Policies (Continued)

Recently Issued Accounting Standards

Presentation of Comprehensive Income

In June 2011, the FASB issued ASU No. 2011-05, Comprehensive Income (Topic 220), “Presentation of

Comprehensive Income.” The objective of this new guidance is to improve the comparability, consistency, and

transparency of financial reporting and to increase the prominence of items reported in other comprehensive

income. The new guidance requires all non-owner changes in stockholders’ equity be presented either in a single

continuous statement of comprehensive income or in two separate but consecutive statements. The new guidance

will be applied retrospectively for fiscal years, and interim periods within those years, beginning after

December 15, 2011. As such, this new guidance will be effective for us in the first quarter 2012. The new

guidance will not have an impact on our results of operations.

Fair Value Measurement and Disclosure Requirements

In May 2011, the FASB issued ASU No. 2011-04, Fair Value Measurement (Topic 820), “Amendments to

Achieve Common Fair Value Measurement and Disclosure Requirements in U.S. GAAP and IFRSs.” These

amendments (1) clarify the FASB’s intent about the application of existing fair value measurement and

disclosure requirements; and (2) change particular principles or requirements for measuring fair value or for

disclosing information about fair value measurements. This new guidance is effective prospectively for interim

and annual periods beginning after December 15, 2011 and is not expected to have a material impact on our fair

value measurements.

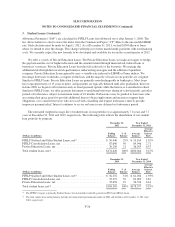

3. Student Loans

There are three principal categories of FFELP Loans: Stafford, PLUS, and FFELP Consolidation Loans.

Generally, Stafford and PLUS Loans have repayment periods of between five and ten years. FFELP

Consolidation Loans have repayment periods of twelve to thirty years. FFELP Loans do not require repayment,

or have modified repayment plans, while the borrower is in-school and during the grace period immediately upon

leaving school. The borrower may also be granted a deferment or forbearance for a period of time based on need,

during which time the borrower is not considered to be in repayment. Interest continues to accrue on loans in the

in-school, deferment and forbearance period. FFELP Loans obligate the borrower to pay interest at a stated fixed

rate or a variable rate reset annually (subject to a cap) on July 1 of each year depending on when the loan was

originated and the loan type. FFELP Loans disbursed before April 1, 2006 earn interest at the greater of the

borrower’s rate or a floating rate based on the SAP formula, with the interest earned on the floating rate that

exceeds the interest earned from the borrower being paid directly by ED. In low or certain declining interest rate

environments when student loans are earning at the fixed borrower rate, and the interest on the funding for the

loans is variable and declining, we can earn additional spread income that we refer to as Floor Income. For loans

disbursed after April 1, 2006, FFELP Loans effectively only earn at the SAP rate, as the excess interest earned

when the borrower rate exceeds the SAP rate (Floor Income) is required to be rebated to ED.

FFELP Loans are insured as to their principal and accrued interest in the event of default subject to a Risk

Sharing level based on the date of loan disbursement. These insurance obligations are supported by contractual

rights against the United States. For loans disbursed after October 1, 1993 and before July 1, 2006, we receive 98

percent reimbursement on all qualifying default claims. For loans disbursed on or after July 1, 2006, we receive

97 percent reimbursement.

On December 23, 2011, the President signed the Consolidated Appropriations Act of 2012 into law. This

law includes changes that permit FFELP lenders or beneficial holders to change the index on which the Special

F-25