Sallie Mae 2011 Annual Report Download - page 142

Download and view the complete annual report

Please find page 142 of the 2011 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

|

|

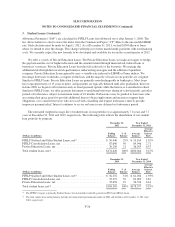

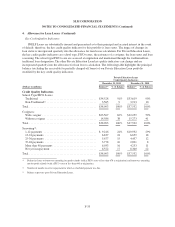

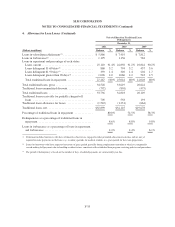

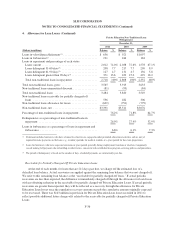

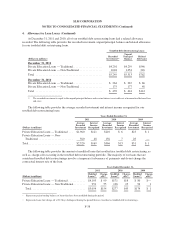

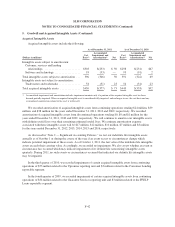

SLM CORPORATION

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

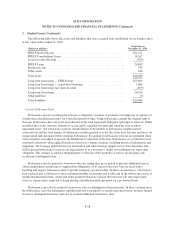

4. Allowance for Loan Losses (Continued)

Key Credit Quality Indicators

FFELP Loans are substantially insured and guaranteed as to their principal and accrued interest in the event

of default; therefore, the key credit quality indicator for this portfolio is loan status. The impact of changes in

loan status is incorporated quarterly into the allowance for loan losses calculation. For Private Education Loans,

the key credit quality indicators are school type, FICO scores, the existence of a cosigner, the loan status and loan

seasoning. The school type/FICO score are assessed at origination and maintained through the traditional/non-

traditional loan designation. The other Private Education Loan key quality indicators can change and are

incorporated quarterly into the allowance for loan losses calculation. The following table highlights the principal

balance (excluding the receivable for partially charged-off loans) of our Private Education Loan portfolio

stratified by the key credit quality indicators.

Private Education Loans

Credit Quality Indicators

December 31, 2011 December 31, 2010

(Dollars in millions) Balance(3) % of Balance Balance(3) % of Balance

Credit Quality Indicators

School Type/FICO Scores:

Traditional ........................................ $34,528 91% $33,619 90%

Non-Traditional(1) ................................... 3,565 9 3,913 10

Total ............................................... $38,093 100% $37,532 100%

Cosigners:

With cosigner ...................................... $23,507 62% $22,259 59%

Without cosigner ................................... 14,586 38 15,273 41

Total ............................................... $38,093 100% $37,532 100%

Seasoning(2):

1-12 payments ..................................... $ 9,246 24% $10,932 29%

13-24 payments .................................... 6,837 18 6,659 18

25-36 payments .................................... 5,677 15 4,457 12

37-48 payments .................................... 3,778 10 2,891 8

More than 48 payments .............................. 6,033 16 4,253 11

Not yet in repayment ................................ 6,522 17 8,340 22

Total ............................................... $38,093 100% $37,532 100%

(1) Defined as loans to borrowers attending for-profit schools (with a FICO score of less than 670 at origination) and borrowers attending

not-for-profit schools (with a FICO score of less than 640 at origination).

(2) Number of months in active repayment for which a scheduled payment was due.

(3) Balance represents gross Private Education Loans.

F-33