Sallie Mae 2011 Annual Report Download - page 161

Download and view the complete annual report

Please find page 161 of the 2011 Sallie Mae annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

|

|

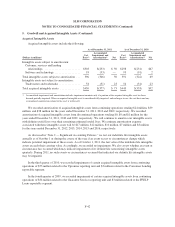

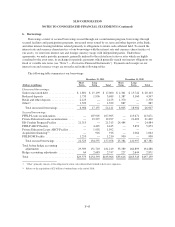

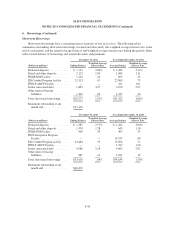

SLM CORPORATION

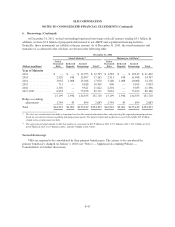

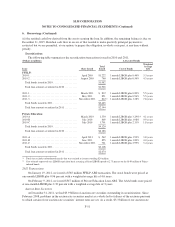

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

6. Borrowings (Continued)

securities as of December 31, 2011 bore interest at the maximum rate allowable under their terms. The maximum

allowable interest rate on our taxable auction rate securities is generally LIBOR plus 1.50 percent to 3.50 percent,

dependant on the security’s credit rating. The maximum allowable interest rate on many of our tax-exempt

auction rate securities is a formula driven rate, which produced various maximum rates up to 0.53 percent during

the fourth quarter of 2011. As of December 31, 2011, $0.6 billion of auction rate securities with shorter weighted

average terms to maturity have had successful auctions, resulting in an average rate of 1.70 percent.

Reset Rate Notes

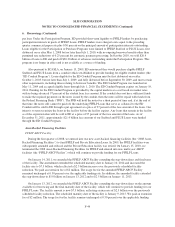

Certain tranches of our term ABS are reset rate notes. Reset rate notes are subject to periodic remarketing, at

which time the interest rates on the notes are reset. We also have the option to repurchase a reset rate note upon a

failed remarketing and hold it as an investment until such time it can be remarketed. In the event a reset rate note

cannot be remarketed on the remarketing date, and is not repurchased, the interest rate generally steps up to and

remains at LIBOR plus 0.75 percent until such time as the bonds are successfully remarketed or repurchased. Our

repurchase of a reset rate note requires additional funding, the availability and pricing of which may be less

favorable to us than it was at the time the reset rate note was originally issued. Unlike the repurchase of a reset

rate note, the occurrence of a failed remarketing does not require additional funding. As a result of the ongoing

dislocation in the capital markets, at December 31, 2011, $6.2 billion of our reset rate notes bore interest at, or

were swapped to LIBOR plus 0.75 percent due to a failed remarketing. Until capital markets conditions improve,

it is possible these and additional reset rate notes will experience failed remarketings. As of December 31, 2011,

we had $7.0 billion and $1.5 billion of reset rate notes due to be newly remarketed in 2012 and 2013,

respectively, and an additional $4.2 billion to be newly remarked thereafter.

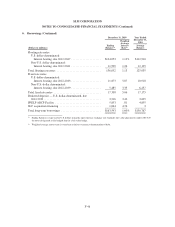

Federal Home Loan Bank of Des Moines (“FHLB-DM”)

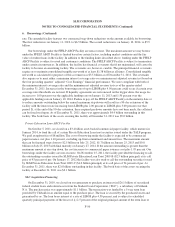

On January 15, 2010, HICA Education Loan Corporation (“HICA”), our subsidiary, entered into a

borrowing agreement with the FHLB-DM. Under the agreement, the FHLB-DM will provide advances backed by

Federal Housing Finance Agency approved collateral which includes FFELP Loans (but does not include Private

Education Loans). The facility is available as long as we maintain membership with FHLB-DM. The amount,

price and tenor of future advances will vary and be subject to the agreement’s borrowing conditions as then in

effect determined at the time of each borrowing. The maximum amount that can be borrowed, as of

December 31, 2011, subject to available collateral, is approximately $8.4 billion. As of December 31, 2011,

borrowing under the facility totaled $1.2 billion, and matures by February 15, 2012, and was secured by

$1.4 billion of FFELP Loans. We have provided a guarantee to the FHLB-DM for the performance and payment

of HICA’s obligations.

Other Funding Sources

Sallie Mae Bank

During the fourth quarter of 2008, the Bank, our Utah industrial bank subsidiary, began expanding its

deposit base to fund new Private Education Loan originations. The Bank raises deposits through intermediaries in

the brokered Certificate of Deposit (“CD”) market and through direct retail deposit channels. As of December 31,

2011, bank deposits totaled $6.3 billion of which $3.7 billion were brokered term deposits, $2.1 billion were

retail and other deposits and $453 million were deposits from affiliates that eliminate in our consolidated balance

sheet. Cash and liquid investments totaled $1.5 billion as of December 31, 2011.

In addition to its deposit base, the Bank has borrowing capacity with the Federal Reserve Bank (“FRB”)

through a collateralized lending facility. FRB is not obligated to lend; however, in general we can borrow as long

F-52